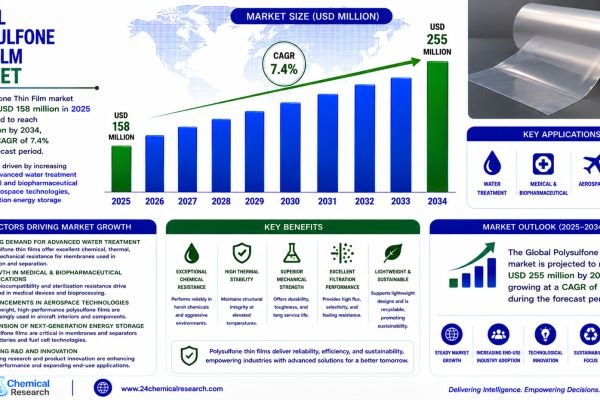

Global Polysulfone Thin Film market size was valued at USD 158 million in 2025. The market is projected to grow from an estimated USD 169 million in 2026 to USD 255 million by 2034, exhibiting a compound annual growth rate (CAGR) of 7.4% during the forecast period.

Polysulfone Thin Film is a high-performance thermoplastic film manufactured from polysulfone (PSU) resin, renowned for its exceptional thermal stability, mechanical strength, and chemical resistance. These films are naturally transparent, dimensionally stable, and possess high dielectric properties, making them ideal for critical applications in medical devices, electrical insulation, membrane supports, and the aerospace sector. Furthermore, their excellent hydrolytic stability makes them particularly well-suited for repeated steam sterilization and use in harsh fluid environments—a combination of attributes that very few engineering materials can consistently deliver at scale.

Get Full Report Here: https://www.24chemicalresearch.com/reports/303863/polysulfone-thin-film-market

Market Dynamics:

The market's trajectory is shaped by a complex interplay of powerful growth drivers, significant restraints that are being actively addressed, and vast, untapped opportunities. While the material itself is far from new, its applications are evolving rapidly, and that is precisely what is keeping the demand curve pointed firmly upward.

Powerful Market Drivers Propelling Expansion

- Surging Demand from Advanced Filtration and Water Treatment: The single largest driver for polysulfone thin film is the escalating global demand from the water and wastewater treatment sector. Polysulfone's exceptional chemical resistance, thermal stability, and mechanical strength make it an ideal substrate material for manufacturing high-performance ultrafiltration and microfiltration membranes. These membranes are absolutely critical for producing high-purity water in pharmaceutical manufacturing, desalination plants, and large-scale industrial processes where performance reliability is non-negotiable. Beyond this, the increasing global focus on freshwater scarcity and the tightening of environmental discharge regulations are further accelerating the adoption of advanced membrane filtration technologies, creating a sustained and growing demand pipeline that shows no sign of slowing down.

- Expansion Across the Medical and Life Sciences Industry: Another powerful and well-established driver is the expanding application of polysulfone thin films within the medical and life sciences industry. The material's proven biocompatibility and its ability to withstand sterilization using multiple methods—including steam autoclaving, ethylene oxide gas, and gamma radiation—make it a preferred choice for critical medical devices and diagnostic systems. It is widely used in hemodialysis membranes, pharmaceutical filtration cartridges, and single-use bioprocess components. The aging global population and the rising worldwide prevalence of chronic conditions such as end-stage renal disease are creating a sustained and structurally growing demand for these life-critical applications. Because this demand is tied to long-term demographic trends rather than economic cycles, it provides a particularly stable and predictable growth foundation for the market.

- Adoption in Aerospace, Automotive, and Electronics: The push for lightweight, thermally stable, and electrically insulating materials across the aerospace, automotive, and electronics sectors is adding another meaningful growth layer. Polysulfone thin films are used as dielectric layers, protective coatings, and structural components in assemblies that require high heat deflection temperatures combined with excellent dimensional stability. In electronics, as manufacturers continue to miniaturize components, the need for thin, high-performance dielectric films becomes increasingly important. Similarly, the aerospace and automotive industries' unrelenting push for fuel efficiency and stringent flame retardancy requirements aligns closely with polysulfone's inherent material properties, making it a natural fit for next-generation lightweight design strategies.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/303863/polysulfone-thin-film-market

Significant Market Restraints Challenging Adoption

Despite its considerable promise, the polysulfone thin film market faces real hurdles that manufacturers and end-users alike must actively work to overcome before universal adoption can be achieved.

- High Raw Material and Complex Production Costs: A primary restraint facing the polysulfone thin film market is the high cost associated with both its feedstocks and its manufacturing process. The raw materials required—particularly specialty monomers such as bisphenol-A and diphenyl sulfone—are considerably more expensive than commodity plastics. Furthermore, the manufacturing process for producing high-quality, defect-free thin films is both complex and energy-intensive, typically involving sophisticated techniques such as solution casting or phase inversion under carefully controlled conditions. This elevated cost structure can limit the material's penetration in price-sensitive market segments, making it less immediately competitive against lower-cost alternatives like polyvinylidene fluoride (PVDF) in applications where the full performance profile of polysulfone is not strictly necessary.

- Regulatory Hurdles in High-Value End-Use Sectors: In the medical device, pharmaceutical, and food contact sectors, polysulfone films must undergo rigorous and time-consuming regulatory certification processes from bodies such as the U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA). Meeting standards such as USP Class VI biocompatibility testing and ISO 10993 biological evaluation adds significant time and cost to product development cycles. For new entrants especially, navigating these compliance pathways is a formidable barrier that can delay commercial product launches by years and consume a disproportionate share of development budgets.

Critical Market Challenges Requiring Innovation

The polysulfone thin film market also contends with several structural challenges that require ongoing innovation to resolve. The price volatility of key petrochemical feedstocks—particularly bisphenol-A, which is also in demand for epoxy resins and polycarbonate—creates uncertainty in raw material procurement and makes consistent product pricing difficult for manufacturers. This unpredictability can erode profit margins and deter long-term capacity investment, particularly when crude oil prices are subject to geopolitical disruptions.

Furthermore, competition from other high-performance thermoplastic films is intensifying. While polysulfone offers a balanced and well-established property profile, materials like Polyether Ether Ketone (PEEK) offer superior mechanical performance at continuous elevated temperatures, and Polyimide (PI) films provide better thermal stability in the most extreme thermal environments. This means that in applications at the very top of the performance spectrum, polysulfone must justify its position on merit, requiring manufacturers to invest continuously in material refinement and application-specific grades. The knowledge gap in many emerging economies, where awareness of advanced engineering polymers remains limited, also slows market penetration in regions that otherwise offer significant volume growth potential.

Vast Market Opportunities on the Horizon

- The Rapidly Expanding Electric Vehicle and Battery Sector: One of the most compelling emerging opportunities for polysulfone thin films lies in the electric vehicle and renewable energy storage markets. Polysulfone films are being actively investigated as advanced separators in lithium-ion batteries due to their excellent thermal stability and strong electrolyte resistance, properties that can meaningfully enhance battery safety and overall service longevity. As the global push for electrification intensifies and demand for high-performance, thermally stable energy storage solutions accelerates, this application segment could transition from a promising research avenue into a significant commercial growth driver within the forecast period.

- Sustainable and Bio-Based Material Innovation: A significant strategic opportunity lies in the development of more sustainable variants of polysulfone. Research into bio-based feedstocks and more environmentally responsible production processes can open access to new customer segments, particularly in Europe and North America, where environmental, social, and governance (ESG) criteria are becoming increasingly embedded in procurement decisions. Companies that invest in and successfully commercialize greener polysulfone thin film products stand to capture a premium market segment while simultaneously strengthening their regulatory and reputational positioning for the long term.

- Expansion Into High-Growth Emerging Markets: There is immense and largely untapped potential for market expansion in the Asia-Pacific region, particularly across China, India, and Southeast Asia. Rapid industrialization, growing government investments in water infrastructure upgrades, and an expanding and increasingly sophisticated healthcare sector in these countries are together creating fertile conditions for the wider adoption of polysulfone thin films. Strategic manufacturing partnerships, localized production facilities, and targeted technical education initiatives for end-users in these regions can help leading suppliers effectively capitalize on this high-growth opportunity without sacrificing the quality and compliance standards that define their value proposition in more mature markets.

In-Depth Segment Analysis: Where is the Growth Concentrated?

By Type:

The market is segmented into PSU (Polysulfone), PES (Polyethersulfone), and others. PSU films represent the foundational product category, valued for their outstanding thermal endurance and mechanical robustness that are critical in high-stress operating environments. However, PES films are gaining notable market traction due to their superior chemical resistance and enhanced hydrolytic stability, making them increasingly preferred for applications that involve repeated sterilization cycles and exposure to aggressive process chemicals, particularly within the medical and biopharmaceutical sectors. These differing but complementary material profiles create distinct and durable application niches for each type.

By Application:

Application segments include Water Treatment and Environmental Engineering, Medical and Biopharmaceutical, Food and Beverage, and others. The Medical and Biopharmaceutical segment is a primary driver for advanced polysulfone thin films, leveraging the material's unique and proven ability to withstand repeated autoclaving while maintaining full structural and functional integrity in contact with biological fluids. Concurrently, Water Treatment and Environmental Engineering represents a high-volume, high-growth application segment where the films serve as critical membrane supports prized for their durability and resistance to fouling. Both segments are shaped by stringent regulatory requirements that continuously push the boundaries of film performance and manufacturing precision.

By End-User Industry:

The end-user landscape includes Medical Device Manufacturers, Water Treatment Plant Operators, and Electronics and Aerospace Companies. Medical Device Manufacturers constitute a sophisticated and demanding end-user segment with extremely rigorous specifications for material purity, biocompatibility, and sterilization performance. Water Treatment Plant Operators, on the other hand, require large-volume, cost-effective, and highly durable membrane solutions that can deliver consistent filtration performance over extended operational lifecycles. The specific and often non-negotiable technical requirements of these two primary end-user groups drive the development of customized film grades and foster deep, long-term collaborative relationships between material suppliers and their industrial customers.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/303863/polysulfone-thin-film-market

Competitive Landscape:

The global Polysulfone Thin Film market is characterized by a high degree of specialization and is dominated by a concentrated group of established multinational chemical and advanced polymer companies. The market's competitive environment is defined by significant barriers to entry—including stringent technical requirements for product purity, consistency, and performance; complex and capital-intensive manufacturing processes; and deep intellectual property portfolios held by incumbents. These leading players compete primarily on the basis of technological innovation, product reliability for critical applications in medical devices and industrial filtration, and the strength and reach of their global supply chain capabilities. Solvay S.A. (Belgium), Victrex plc (United Kingdom), and Ensinger GmbH (Germany) collectively represent the upper tier of the competitive landscape, with their market positions underpinned by decades of application expertise and deep customer relationships in regulated industries.

Beyond the top-tier leaders, the competitive landscape includes several significant niche players and specialized manufacturers serving specific regional markets or application segments. Companies such as RTP Company (United States) and Westlake Plastics Company (United States) are important compounders and processors of engineering plastics offering polysulfone films among their broader portfolios. Specialized distributors and material converters like CS Hyde Company (USA) and Goodfellow Corporation (UK) play a crucial role in the supply chain by providing tailored film products and small-quantity services to a diverse base of R&D and industrial customers. Meanwhile, emerging manufacturers in the Asia-Pacific region, most notably Foshan Dafu New Material Co., Ltd. (China), are growing by offering competitive pricing alongside expanding regional production capacity, particularly to serve the strong domestic demand in water treatment and consumer electronics manufacturing. The competitive strategy across the board is increasingly focused on developing application-specific film grades and forging long-term supply agreements with key end-users, thereby building switching cost advantages and securing predictable revenue streams.

List of Key Polysulfone Thin Film Companies Profiled:

- Solvay S.A. (Belgium)

- Victrex plc (United Kingdom)

- Ensinger GmbH (Germany)

- RTP Company (United States)

- Syensqo (Belgium)

- Mitsubishi Chemical Group (Japan)

- CS Hyde Company (United States)

- Westlake Plastics Company (United States)

- Goodfellow Corporation (United Kingdom)

- dr Dietrich Müller GmbH (Germany)

- Foshan Dafu New Material Co., Ltd. (China)

The competitive strategy across the market is overwhelmingly focused on continuous R&D investment to enhance product quality, improve membrane morphology control, and reduce overall production costs, alongside forming strategic vertical partnerships with end-user companies to co-develop and validate application-specific solutions, thereby securing long-term and defensible demand.

Regional Analysis: A Global Footprint with Distinct Leaders

- North America: North America, led by the United States, holds a commanding position in the global Polysulfone Thin Film market. The region's leadership is anchored by the presence of major market participants including Solvay and Westlake Plastics, which drive advanced material innovation domestically. Stringent regulatory standards from the FDA governing medical and food contact materials create a consistent and high-value demand environment for compliant polysulfone films. Advanced water treatment infrastructure projects further utilize these films extensively in membrane filtration systems. The high concentration of aerospace, semiconductor, and specialized electronics manufacturing also provides a technologically demanding customer base that values the material's thermal stability and dielectric performance.

- Europe: Europe represents a significant and technologically mature market for Polysulfone Thin Film, supported by a strong regional presence of key manufacturers including Ensinger, Victrex, and Syensqo. The region's demand is driven by a well-established medical and pharmaceutical industry that places a premium on high-purity materials capable of withstanding repeated sterilization cycles. European environmental regulations promoting advanced water treatment and membrane filtration technologies also contribute meaningfully to demand. The region's focus on sustainability and circular economy principles is furthermore shaping innovation pathways, potentially driving research into more recyclable or bio-derived polysulfone variants over the medium to long term.

- Asia-Pacific: The Asia-Pacific market for Polysulfone Thin Film is experiencing rapid and broad-based growth, with China and Japan serving as key regional contributors. The region benefits from a massive manufacturing base for electronics and a rapidly expanding and professionalizing healthcare sector. Local manufacturers, including Mitsubishi Chemical Group and Foshan Dafu New Material Co., Ltd., are increasing production capacities to serve both domestic and international demand. Market growth is propelled by urbanization, industrialization, and large-scale government investments in water and wastewater treatment infrastructure. The competitive landscape in this region is notably intense, with cost-effectiveness being a primary differentiator that shapes pricing strategies alongside ongoing investment in technological capability.

- South America, Middle East & Africa: These regions represent the emerging frontier of the Polysulfone Thin Film market. South America, particularly Brazil and Argentina, is seeing gradual development driven by growing healthcare expenditure and industrialization, though import dependency for advanced materials remains a characteristic constraint. The Middle East and Africa, especially GCC countries such as Saudi Arabia and the UAE, present growth opportunities centered on large-scale water desalination and energy infrastructure projects where advanced membrane technologies are increasingly specified. While overall penetration remains limited relative to more developed regions, the long-term structural drivers in both areas—water scarcity, healthcare sector growth, and government-led economic diversification—underpin a positive and sustained outlook.

Get Full Report Here: https://www.24chemicalresearch.com/reports/303863/polysulfone-thin-film-market

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/303863/polysulfone-thin-film-market

About 24chemicalresearch

Founded in 2015, 24chemicalresearch has rapidly established itself as a leader in chemical market intelligence, serving clients including over 30 Fortune 500 companies. We provide data-driven insights through rigorous research methodologies, addressing key industry factors such as government policy, emerging technologies, and competitive landscapes.

- Plant-level capacity tracking

- Real-time price monitoring

- Techno-economic feasibility studies

International: +1(332) 2424 294 | Asia: +91 9169162030

Website: https://www.24chemicalresearch.com/