A consistent operational scale-up is redefining high-volume stamping, automated welding, and modular platform assembly pipelines, fueled by the commercial necessity to deliver highly rigid, resilient structural platforms that comply with rigorous crash-safety criteria worldwide.

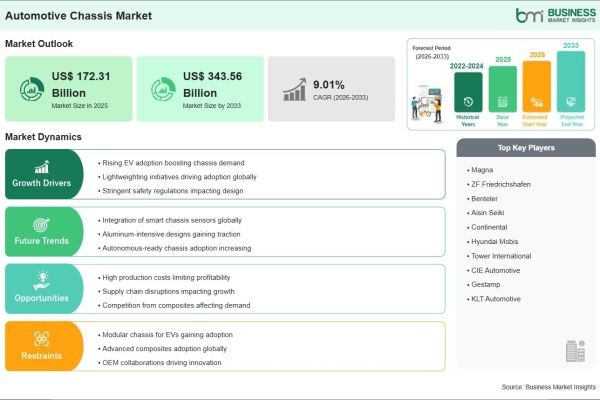

Based on market intelligence from Business Market Insights, the global Automotive Chassis Market is anticipated to reach US$ 343.56 billion by 2033, mounting from its 2025 value of US$ 172.31 billion at a projected CAGR of 9.01% from 2026 to 2033.

Download Sample Report : https://www.businessmarketinsights.com/sample/BMIPUB00035562

What Are Automotive Chassis?

Automotive chassis serve as the foundational internal framework of a vehicle, essentially acting as the structural skeleton that supports the powertrain, suspension, and vehicle body. They are engineered to bear mechanical loads and dynamic stresses during operation, ensuring stability, optimal handling, and safety. A robust chassis accommodates critical components like the engine, transmission, steering system, and axles, serving as the base upon which the entire automobile is assembled and integrated.

Technological advancements in advanced metallurgy and structural engineering, such as the development of modular "skateboard" platforms, multi-material constructions, and the use of ultra-high-strength steel (UHSS), are profoundly reshaping the automotive chassis industry. Manufacturers are increasingly focusing on delivering lightweight, highly rigid frames capable of superior crash energy absorption and seamless integration with complex electronic suspension systems. This strategic shift allows global automotive OEMs to achieve highly optimized vehicle dynamics, significantly improve power-to-weight ratios, and confidently transition toward zero-emission fleet production.

Common chassis designs include the traditional ladder frame, monocoque (unitary), backbone, and modern modular architectures. Modern automotive chassis manufacturing incorporates precision hydroforming, robotic spot welding, and advanced laser-cutting processes to ensure the reliability of these critical load-bearing structures under intense road stress. The adoption and evolution of these frameworks are currently heavily influenced by the electric vehicle (EV) sector, where achieving structural rigidity while offsetting heavy battery weight is paramount.

Industry Drivers

A major driver of the Automotive Chassis Industry is the accelerating shift toward electric mobility and the subsequent demand for specialized EV platforms. Unlike conventional internal combustion engine (ICE) vehicles, EVs require specialized, modular chassis designs capable of safely housing heavy, large-scale battery packs within the vehicle floor. This fundamental structural requirement is generating immense, recurring demand for upgraded chassis architectures that provide enhanced torsional rigidity and an optimized low center of gravity.

The pressing need for vehicle light-weighting to meet stringent global emission and fuel-efficiency regulations serves as another critical growth factor. Automakers are aggressively replacing traditional heavy steel components with advanced aluminum alloys, high-strength steels, and carbon fiber composites. This evolution allows vehicles to achieve extended driving ranges and better fuel economy without compromising passenger safety, driving continuous innovation cycles and higher-value procurement within the chassis market.

Furthermore, the expansion of global vehicle production—particularly the rising popularity of SUVs and light commercial vehicles in emerging economies—creates a sustained demand for highly durable, robust conventional and monocoque chassis systems. As consumer preferences demand vehicles that offer a premium blend of comfort, durability, and safety, manufacturers are heavily investing in localized chassis production lines to support surging automotive output.

Industry Segmentation

By Chassis Type

- Monocoque Chassis: The dominant segment, widely used in modern passenger cars and SUVs due to its excellent structural integrity, lightweight properties, and superior crash safety performance.

- Modular/Skateboard Chassis: The fastest-growing segment, purpose-built for electric vehicles to offer flexible manufacturing and lower the center of gravity by integrating battery enclosures directly into the base frame.

- Ladder Frame Chassis: Remains essential for heavy commercial vehicles, pickup trucks, and rugged off-road vehicles requiring maximum load-bearing capacity and durability.

By Material Type

- High-Strength Steel: Continues to hold the largest market share due to its superior cost-effectiveness, high durability, and ease of high-volume manufacturing.

- Aluminum Alloys: Experiencing rapid adoption for light-weighting purposes, significantly improving the power-to-weight ratio in premium, luxury, and electric vehicles.

- Carbon Fiber Composites: A niche but rapidly emerging material segment offering unmatched stiffness and weight reduction for high-performance applications.

By Vehicle Type

- Passenger Cars: The leading end-user segment, driven by vast global production volumes, continuous design iterations, and the rapid rollout of light-duty electric vehicles.

- Commercial Vehicles: Growing steadily, reliant on highly durable chassis structures to manage extreme payloads and heavy-duty logistics operations over long distances.

Regional Insights

- Asia-Pacific: The dominant and fastest-growing region, fueled by its position as the world's largest automotive manufacturing hub (led by China, India, and Japan) and backed by massive government incentives for EV adoption.

- North America: Maintains a highly lucrative market, driven by heavy consumer demand for large SUVs and pickup trucks requiring durable ladder frames, alongside rapid investments in localized electric vehicle supply chains.

- Europe: Shows steady, premium-driven growth, supported by the strictest global carbon emission mandates, the presence of leading luxury automakers, and early adoption of lightweight modular architectures.

- Middle East & Africa: Experiencing gradual growth driven by expanding road infrastructure, rising commercial vehicle sales, and the localization of automotive assembly plants.

- South & Central America: Remains a highly active market, focusing on optimizing local production efficiency and catering to growing domestic demands for passenger and light commercial transport.

Top Players in the Automotive Chassis Industry

The market is highly competitive and capital-intensive, characterized by leading global tier-1 suppliers focusing on multi-material integration, advanced robotics, and strategic OEM partnerships:

- Continental AG

- ZF Friedrichshafen AG

- Magna International Inc.

- Schaeffler AG

- Aisin Corporation

- Benteler International AG

- CIE Automotive

- Hyundai Mobis

- Gestamp Automocion S.L.

- Tower International

Technological Innovations

Technological innovation is rapidly transforming the Automotive Chassis Industry. The widespread adoption of "skateboard" chassis platforms has revolutionized EV manufacturing. This innovation allows automakers to use a single, highly scalable base architecture across multiple distinct vehicle models. This extreme modularity drastically reduces research and development time, lowers per-unit production costs, and accelerates time-to-market for new electric fleets.

Furthermore, the integration of smart, mechatronic chassis technologies is gaining immense traction. Manufacturers are developing active chassis systems featuring electronic roll stabilization, steer-by-wire mechanics, and adaptive suspension kinematics. These software-defined chassis components communicate in real-time with Advanced Driver Assistance Systems (ADAS), enabling dynamic mechanical adjustments that significantly enhance vehicle stability, automated safety, and overall ride comfort.

Future Industry Outlook

The future outlook for the Automotive Chassis Market is highly promising, shaped directly by the industry's irreversible pivot toward electrification and autonomous driving. As self-driving technologies mature, chassis systems will increasingly rely on "by-wire" technologies—where heavy mechanical linkages for steering and braking are replaced by lightweight electronic sensors and actuators. This shift will require chassis frames to become fundamentally smarter, lighter, and structurally adaptable.

Companies that prioritize the development of multi-material platforms, sustainable manufacturing practices, and highly integrated mechatronic solutions will be best positioned to capture substantial market share. As automakers push aggressively for net-zero carbon footprints, the integration of recycled "green" steel and low-carbon secondary aluminum into chassis production will become a major competitive differentiator through 2033.

Frequently Asked Questions (FAQs)

What is the projected size of the Automotive Chassis Market by 2033?

The market is projected to reach US$ 147.2 billion by 2033, expanding from an estimated US$ 94.2 billion in 2025.

What factors are driving industry growth?

Key drivers include the massive global shift toward specialized electric vehicle platforms, urgent demands for vehicle lightweighting to improve battery range and fuel efficiency, and rising global vehicle production volumes.

Which chassis type dominates the market?

The monocoque chassis segment holds the largest market share, as it is the standard, highly efficient structural foundation for the vast majority of modern passenger cars and SUVs.

Which region leads the automotive chassis industry?

Asia-Pacific is the dominant and fastest-growing region, driven by unparalleled automotive manufacturing capacities, massive domestic consumption, and an aggressive transition to electric mobility.

Browse More Reports:

https://www.businessmarketinsights.com/reports/brics-veterinary-x-ray-market

https://www.businessmarketinsights.com/reports/north-america-veterinary-x-ray-market

https://www.businessmarketinsights.com/reports/europe-laser-ablation-market

About Us

Business Market Insights is a market research platform that provides subscription service for industry and company reports. Our research team has extensive professional expertise in domains such as Electronics & Semiconductor; Aerospace & Defense; Automotive & Transportation; Energy & Power; Healthcare; Manufacturing & Construction; Food & Beverages; Chemicals & Materials; and Technology, Media, & Telecommunications.

Contact Us

If you have any questions about this report or would like further information, please contact us:

Contact person: Ankit Mathur

Email: sales@businessmarketinsights.com

Phone: +16467917070