CFRTP UD (Unidirectional) Tape is an advanced composite material consisting of continuous reinforcing fibers—primarily carbon, glass, or aramid—fully impregnated within a thermoplastic polymer matrix such as PEEK, PA, PPS, or LM-PAEK. Designed specifically for use in high-speed Automated Fiber Placement (AFP) and Automated Tape Laying (ATL) processes, these tapes enable precise, repeatable, and rapid deposition of composite plies, making them indispensable in the manufacture of structurally demanding components across aerospace, automotive, and defense sectors. Unlike conventional thermoset prepregs, thermoplastic-based UD tapes can be consolidated in-situ during the layup process, eliminating the need for autoclave post-curing and fundamentally reshaping the economics of high-performance composite manufacturing.

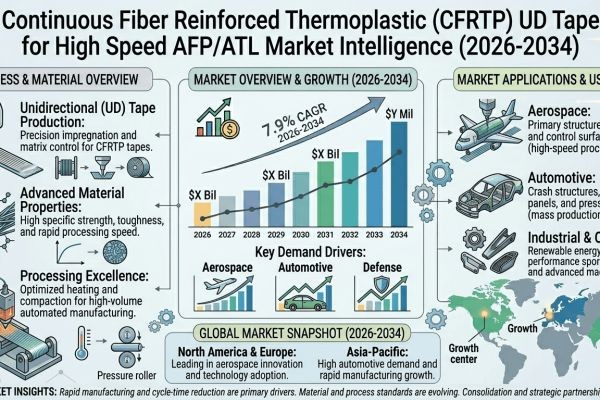

The market is witnessing robust expansion driven by the accelerating shift from thermoset to thermoplastic composites in primary and secondary aerospace structures, increasing demand for lightweighting solutions in next-generation aircraft programs, and significant advancements in in-situ consolidation technology that compress processing cycle times. Furthermore, leading OEMs and Tier-1 suppliers are actively investing in high-rate AFP/ATL manufacturing lines to meet rising aircraft production targets. Toray Industries, Syensqo (formerly Solvay), Teijin Limited, and Celanese Corporation are among the key players actively advancing their CFRTP UD tape portfolios to address the evolving requirements of high-speed automated composite manufacturing.

Get Full Report Here: https://www.24chemicalresearch.com/reports/308896/continuous-fiber-reinforced-thermoplastic-ud-tape-for-high-speed-afpatl-market

Market Dynamics:

The market's trajectory is shaped by a complex interplay of powerful growth drivers, significant restraints that are being actively addressed, and vast, untapped opportunities across multiple high-value industrial sectors.

Powerful Market Drivers Propelling Expansion

-

Rising Demand from Aerospace and Defense Sector Accelerating CFRTP UD Tape Adoption: The aerospace and defense industry remains the most significant demand driver for CFRTP UD Tape used in high-speed AFP and ATL processes. Aircraft manufacturers and their Tier-1 suppliers are under sustained pressure to reduce structural weight while maintaining or improving mechanical performance—and thermoplastic composites offer a compelling answer. Thermoplastic UD tapes enable faster processing cycles compared to thermoset alternatives, eliminating autoclave curing requirements in many applications and significantly reducing out-of-autoclave processing times. Leading commercial aerospace programs have increasingly incorporated thermoplastic composite structures, particularly in secondary and primary structural components, as confidence in the material's performance envelope grows within engineering and certification communities worldwide.

-

Advances in High-Speed AFP and ATL Equipment Unlocking Process Efficiency Gains: The rapid maturation of high-speed AFP and ATL machinery has been a decisive enabler for CFRTP UD tape adoption across multiple end-use industries. Modern AFP systems can achieve laydown rates that were technically unachievable less than a decade ago, with some platforms capable of deposition rates exceeding 100 kg/hour under optimized conditions. These machines are increasingly equipped with in-situ consolidation technology—laser, flame, or hot gas torch heating—that allows thermoplastic tapes to be consolidated immediately upon placement, removing entire downstream process steps. Furthermore, digital process control, machine learning-assisted defect detection, and adaptive laydown path optimization are making high-speed AFP and ATL systems more reliable and repeatable, which is critical for regulated industries such as aerospace.

-

Sustainability Mandates and Circular Economy Pressures Strengthening the Thermoplastic Value Proposition: Environmental regulation and voluntary sustainability commitments are increasingly influencing material selection decisions in aerospace, automotive, and wind energy sectors—and CFRTP UD tapes are well positioned to benefit. Unlike epoxy-based thermoset composites, thermoplastic matrix systems such as PEEK, PEKK, PPS, and PA12 can be remelted, reformed, and in principle reintegrated into the supply chain at end of product life. The combination of reduced scrap rates during AFP/ATL manufacturing—enabled by precise digital deposition and near-net-shape layup—and end-of-life recyclability is making CFRTP UD tapes an increasingly preferred choice among sustainability-conscious procurement teams operating under tightening regulatory frameworks in Europe and North America.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/308896/continuous-fiber-reinforced-thermoplastic-ud-tape-for-high-speed-afpatl-market

Significant Market Restraints Challenging Adoption

Despite its strong technical performance profile, the market faces meaningful hurdles that must be addressed to enable broader commercial adoption beyond the established aerospace prime contractor ecosystem.

-

Elevated Capital Investment Requirements Limiting Accessibility for Mid-Tier Manufacturers: High-speed AFP and ATL systems capable of processing CFRTP UD tape with integrated in-situ consolidation represent a substantial capital commitment that remains out of reach for many mid-tier composite manufacturers. The acquisition cost of advanced multi-axis AFP platforms from leading machine builders, combined with the associated infrastructure—including controlled-environment layup cells, specialized tooling, and process monitoring systems—can represent investments of several million dollars per machine installation. When this capital expenditure is considered alongside the additional costs of operator training, process development, and material qualification, the total cost of entry is high enough to constrain adoption among companies without either deep internal capital resources or firm long-term program commitments from major OEM customers.

-

Competition from Thermoset Prepreg and Emerging Alternative Technologies: CFRTP UD tape for AFP/ATL competes not only with incumbent thermoset prepreg systems—which benefit from mature qualification databases, established supply chains, and deeply embedded process knowledge within the aerospace industry—but also with a range of emerging alternative composite manufacturing technologies. Dry fiber AFP combined with resin transfer infusion, for example, offers competitive cost and process flexibility for certain large-area structural applications and is attracting growing investment from aerospace structures manufacturers. Additionally, advances in rapid-cure thermoset chemistries and out-of-autoclave thermoset prepreg systems are narrowing the cycle time gap that has historically been one of CFRTP's most compelling arguments, requiring the thermoplastic AFP/ATL ecosystem to continue demonstrating differentiated value beyond processing speed alone.

Critical Market Challenges Requiring Innovation

The transition from laboratory-scale success to industrial-scale AFP and ATL manufacturing presents its own distinct set of challenges. Achieving high-quality in-situ consolidated CFRTP laminates during high-speed AFP deposition requires precise and simultaneous control of a large number of interdependent process variables, including heating source power, standoff distance, laydown speed, compaction force, and ambient temperature. The thermal window within which thermoplastic matrices must be maintained to achieve adequate bonding without degradation is narrow—and this window narrows further as laydown speed increases. Establishing robust and validated process parameter sets for new tape-machine-application combinations requires significant experimental effort and specialized expertise that many potential adopters, particularly smaller Tier-2 and Tier-3 manufacturers, do not have readily available internally.

Additionally, the absence of widely adopted industry standards specifically addressing CFRTP UD tape characterization, quality assurance, and process qualification for AFP/ATL manufacturing creates uncertainty for both material producers and end-users seeking regulatory certification. While established thermoset composite materials benefit from decades of accumulated test data and well-understood certification pathways, thermoplastic composites manufactured via high-speed AFP/ATL remain in a comparatively early stage of regulatory documentation. This creates a situation where technically capable materials face extended and costly certification timelines before they can be deployed in safety-critical structures, introducing procurement risk that slows the pace of technology adoption.

Vast Market Opportunities on the Horizon

-

Next-Generation Commercial Aircraft Programs Creating Sustained Long-Term Demand: The anticipated development and eventual production ramp of next-generation narrowbody and widebody commercial aircraft platforms over the coming decade represents a substantial demand opportunity for CFRTP UD tape processed via high-speed AFP and ATL. Aircraft OEMs and their structural design teams are increasingly evaluating thermoplastic composites for fuselage panels, floor beams, frames, ribs, and control surfaces, driven by the lifecycle cost and throughput advantages that thermoplastic processing can offer at high production rates. The design community for future programs is approaching material selection with a more open and technology-agnostic methodology than previous generations, creating a genuine opportunity for CFRTP UD tape to capture significant structural content if technical maturity and supply chain readiness can be convincingly demonstrated through ongoing qualification programs.

-

Urban Air Mobility and Advanced Air Mobility Sector Emerging as a Novel Growth Frontier: The rapidly expanding urban air mobility (UAM) and advanced air mobility (AAM) sector—encompassing electric vertical takeoff and landing (eVTOL) aircraft, unmanned aerial systems, and regional electric aircraft—is emerging as a genuinely high-growth application domain for CFRTP UD tape and AFP/ATL manufacturing. These vehicle architectures place extreme emphasis on structural mass minimization to maximize battery-to-payload efficiency, and continuous fiber thermoplastic composites offer an attractive combination of specific stiffness, specific strength, and design flexibility. Furthermore, the production volume ambitions of many UAM developers—targeting hundreds to thousands of vehicles per year—align well with the high-throughput, low-touch manufacturing vision enabled by high-speed AFP/ATL with in-situ consolidation.

-

Digital Manufacturing Integration and Industry 4.0 Enablement Expanding Process Capability: The convergence of CFRTP AFP/ATL manufacturing with digital manufacturing technologies—including real-time process monitoring, closed-loop adaptive control, digital twin simulation, and AI-driven quality inspection—represents a significant opportunity to improve process reliability, reduce qualification costs, and accelerate the pathway to certification for new applications. Machine builders and research institutions are actively developing sensor suites capable of monitoring thermal profiles, compaction pressure, and laminate quality in real time during high-speed AFP deposition, with feedback systems capable of adjusting process parameters dynamically to maintain quality within specification. As these digital capabilities mature and become integrated into commercial AFP and ATL platforms, they will lower the process development burden for new material-application combinations and generate the structured datasets that regulatory authorities increasingly expect as part of certification evidence packages.

In-Depth Segment Analysis: Where is the Growth Concentrated?

By Type:

The market is segmented into Carbon Fiber Reinforced Thermoplastic (CF/TP) UD Tape, Glass Fiber Reinforced Thermoplastic (GF/TP) UD Tape, Aramid Fiber Reinforced Thermoplastic (AF/TP) UD Tape, and Hybrid Fiber Reinforced Thermoplastic UD Tape. Carbon Fiber Reinforced Thermoplastic (CF/TP) UD Tape currently dominates the CFRTP UD tape landscape for high-speed AFP/ATL applications, owing to its exceptional strength-to-weight ratio, superior stiffness, and outstanding fatigue resistance. Carbon fiber-based tapes are particularly sought after in demanding structural aerospace applications where weight reduction is critical without compromising mechanical integrity. Glass fiber reinforced variants are gaining traction as a cost-conscious alternative in semi-structural applications, while hybrid fiber configurations are increasingly explored to engineer tailored mechanical and thermal properties across diverse high-speed AFP/ATL processing requirements.

By Application:

Application segments include Structural Panels and Fuselage Skins, Wing Components and Spars, Pressure Vessels and Piping, Automotive Body and Chassis Components, and others. The Structural Panels and Fuselage Skins segment currently leads the application landscape, driven by the aerospace industry's relentless pursuit of lightweight, high-strength structures. The thermoplastic matrix enables in-situ consolidation during AFP/ATL layup, dramatically reducing cycle times and eliminating the need for autoclave curing. Wing components and spars are emerging as a strategically important application as manufacturers seek to leverage AFP automation for complex curvature geometries, while automotive chassis and body panel applications are expanding rapidly as vehicle lightweighting initiatives drive adoption of AFP-processed CFRTP components.

By End-User Industry:

The end-user landscape includes Aerospace and Defense Manufacturers, Automotive OEMs and Tier-1 Suppliers, Wind Energy Equipment Manufacturers, Oil and Gas Industry, and Sporting Goods and Consumer Products. Aerospace and Defense Manufacturers constitute the foremost end-user segment for CFRTP UD tape processed via high-speed AFP/ATL systems. Commercial airframe OEMs and their Tier-1 suppliers are at the forefront of integrating thermoplastic composite tapes into next-generation aircraft structures, driven by stringent regulatory requirements for fuel efficiency, reduced emissions, and improved recyclability at end-of-life. Automotive OEMs represent a rapidly maturing secondary segment, particularly as electric vehicle architectures create new structural requirements that CFRTP laminates are uniquely positioned to fulfill. Wind energy manufacturers are evaluating CFRTP UD tape for blade spar caps and structural reinforcements, drawn by the material's recyclability advantage and fatigue resistance.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/308896/continuous-fiber-reinforced-thermoplastic-ud-tape-for-high-speed-afpatl-market

Competitive Landscape:

The global CFRTP UD Tape for High Speed AFP/ATL market is characterized by a concentrated group of vertically integrated specialty manufacturers with deep roots in composite materials science and aerospace-grade thermoplastic processing. The market structure reflects relatively tight consolidation at the high-performance end, where tape quality consistency, fiber volume fraction control, and slit-tape dimensional tolerances are non-negotiable for automated layup at speeds exceeding 1,000 mm/s. The top companies—Toray Industries (Japan), Syensqo SA (Belgium), and Toray Advanced Composites (USA/Netherlands)—are among the most prominent players, leveraging proprietary polymer resin systems and fiber sizing technologies optimized for PEEK, PEKK, and PA12-based thermoplastic matrices. These companies benefit from decades of qualification data with major airframers such as Airbus and Boeing, creating substantial barriers to entry for newer competitors.

Beyond the established tier-one suppliers, a number of specialized and emerging manufacturers have carved out competitive niches. The competitive strategy across the industry is overwhelmingly focused on R&D to enhance product quality and reduce processing costs, alongside forming strategic vertical partnerships with end-user companies to co-develop and validate new applications—thereby securing future demand and shortening qualification timelines in regulated end-use sectors.

List of Key Continuous Fiber Reinforced Thermoplastic (CFRTP) UD Tape Companies Profiled:

-

Toray Industries, Inc. (Japan)

-

Toray Advanced Composites (formerly TenCate Advanced Composites) (USA / Netherlands)

-

Teijin Limited (Teijin Carbon) (Japan)

-

Victrex plc (United Kingdom)

-

Celanese Corporation (USA)

-

Suprem SA (Switzerland)

-

Porcher Industries (France)

-

SGL Carbon SE (Germany)

-

Hexcel Corporation (USA)

Regional Analysis: A Global Footprint with Distinct Leaders

-

North America: Is the leading region in the CFRTP UD Tape for High Speed AFP/ATL market, driven by a deeply entrenched aerospace and defense manufacturing base that continues to prioritize advanced composite processing technologies. The United States hosts a concentration of major aircraft manufacturers, Tier-1 suppliers, and material innovators actively integrating high-speed AFP and ATL systems into their production workflows. Sustained government and defense procurement programs demand lightweight, high-performance structural components, creating a consistent pull for CFRTP UD tape solutions. Research institutions and national laboratories in North America have been at the forefront of developing thermoplastic composite processing methods, accelerating the transition from thermoset-dominated systems toward thermoplastic alternatives.

-

Europe & Asia-Pacific: Together, they form a powerful and rapidly growing secondary bloc. Europe's strength is anchored in its aerospace manufacturing corridor stretching across France, Germany, the United Kingdom, and Spain, where aerospace primes and their extensive supplier networks have been early adopters of thermoplastic composites driven by the dual imperatives of structural performance and end-of-life recyclability. Publicly funded research programs and collaborative EU industrial initiatives have accelerated material qualification and process development. Asia-Pacific, meanwhile, is emerging as a rapidly growing market underpinned by expanding aerospace manufacturing capacity in Japan, South Korea, and China, with national programs supporting the adoption of AFP and ATL technologies and Japan's established carbon fiber industry providing a strong material supply foundation.

-

South America and Middle East & Africa: These regions represent the emerging frontier of the CFRTP UD Tape AFP/ATL market. While currently smaller in scale, they present meaningful long-term growth opportunities. Brazil serves as the primary focal point in South America, given its regionally significant aerospace manufacturing sector. The Middle East, particularly Gulf Cooperation Council countries, is demonstrating interest in building diversified advanced manufacturing capabilities, with selective government-backed programs in countries such as the United Arab Emirates supporting the development of composites processing competencies. Increasing aviation infrastructure investments and defense procurement programs signal gradual future demand potential across both regions.

Get Full Report Here: https://www.24chemicalresearch.com/reports/308896/continuous-fiber-reinforced-thermoplastic-ud-tape-for-high-speed-afpatl-market

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/308896/continuous-fiber-reinforced-thermoplastic-ud-tape-for-high-speed-afpatl-market

About 24chemicalresearch

Founded in 2015, 24chemicalresearch has rapidly established itself as a leader in chemical market intelligence, serving clients including over 30 Fortune 500 companies. We provide data-driven insights through rigorous research methodologies, addressing key industry factors such as government policy, emerging technologies, and competitive landscapes.

-

Plant-level capacity tracking

-

Real-time price monitoring

-

Techno-economic feasibility studies

International: +1(332) 2424 294 | Asia: +91 9169162030

Website: https://www.24chemicalresearch.com/