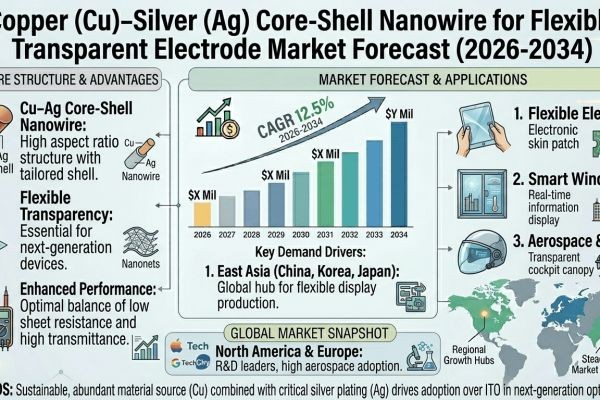

Copper–Silver core-shell nanowires are advanced one-dimensional nanostructures engineered with a copper core encapsulated by a thin silver shell, designed to deliver high electrical conductivity and exceptional optical transparency simultaneously. These hybrid nanomaterials effectively combine the cost advantage of copper with the superior oxidation resistance and surface conductivity of silver, making them a compelling alternative to indium tin oxide (ITO) in flexible and stretchable electronics. Key application areas include organic solar cells, organic light-emitting diodes (OLEDs), touchscreens, wearable sensors, and next-generation flexible displays. The technology has moved steadily from academic demonstration to early commercial deployment, driven by the electronics industry's sustained demand for electrode materials that perform where ITO simply cannot.

Get Full Report Here: https://www.24chemicalresearch.com/reports/308916/-market

Market Dynamics:

The market's trajectory is shaped by a complex interplay of powerful growth drivers, significant restraints that are being actively addressed, and vast, untapped opportunities.

Powerful Market Drivers Propelling Expansion

- Surging Demand for Flexible and Wearable Electronics: The global flexible electronics industry has witnessed accelerated growth over the past decade, creating substantial demand for transparent conductive electrodes that can replace brittle indium tin oxide (ITO). Cu–Ag core-shell nanowires have emerged as a highly promising alternative, offering a combination of high electrical conductivity, optical transparency, and mechanical flexibility that ITO fundamentally cannot deliver. Flexible displays, foldable smartphones, electronic skin sensors, and wearable health monitoring devices all require electrode materials capable of maintaining performance under repeated bending, stretching, and compression cycles — requirements that Cu–Ag nanowire networks fulfill with remarkable consistency. As consumer electronics manufacturers accelerate their transition toward form factors that demand conformable substrates, the case for adopting Cu–Ag core-shell nanowire-based transparent electrodes becomes increasingly compelling from both a technical and commercial standpoint.

- Decisive Cost Advantage Over ITO and Pure Silver Nanowire Systems: One of the most decisive drivers for Cu–Ag core-shell nanowires is their pronounced cost advantage relative to incumbent transparent electrode technologies. Indium, the primary constituent of ITO, is a rare and geopolitically concentrated material, making ITO-based electrodes susceptible to supply chain disruptions and price volatility. Pure silver nanowire networks, while technically superior in several respects, carry significant material costs owing to silver's high commodity price. The Cu–Ag core-shell architecture directly addresses this challenge: a copper nanowire core provides the structural backbone and contributes the majority of electrical conductivity at relatively low material cost, while a thin silver shell — applied through electroless deposition, galvanic replacement, or chemical reduction techniques — imparts oxidation resistance and enhanced surface conductivity. This architecture delivers performance metrics approaching those of pure silver nanowire networks at a substantially reduced material cost, broadening the addressable market across price-sensitive applications in emerging economies and large-area device segments. Furthermore, solution-based synthesis routes and roll-to-roll compatible coating techniques — including bar coating, slot-die coating, and spray coating — allow for high-throughput manufacturing on flexible substrates such as polyethylene terephthalate (PET) and polyimide (PI), reducing capital expenditure requirements relative to vacuum-based ITO sputtering.

- Expansion of Organic Photovoltaics and Perovskite Solar Cell Research: The rapid advancement of next-generation photovoltaic technologies — particularly organic solar cells (OSCs) and perovskite solar cells (PSCs) — has significantly amplified research interest and investment in high-performance flexible transparent electrodes. Both OSC and PSC architectures require front electrodes with sheet resistances typically below 20 Ω/sq alongside optical transmittances exceeding 85% in the visible spectrum, specifications that Cu–Ag core-shell nanowire networks can meet while also offering compatibility with low-temperature processing conditions required by organic and perovskite absorber layers. Published research demonstrates that Cu–Ag nanowire-based transparent electrodes integrated into perovskite solar cell architectures have achieved power conversion efficiencies competitive with ITO-based reference devices, providing empirical validation of their functional suitability. As global photovoltaic research programs and industrial solar cell manufacturers increasingly explore flexible, lightweight, and roll-to-roll processable device platforms, Cu–Ag core-shell nanowires are positioned to capture a growing share of the transparent electrode specification landscape within this high-growth application domain.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/308916/-market

Significant Market Restraints Challenging Adoption

Despite its promise, the market faces hurdles that must be overcome to achieve universal adoption.

- Fragmented Intellectual Property Landscape and Licensing Complexity: The Cu–Ag core-shell nanowire technology space is characterized by a densely layered intellectual property environment spanning synthesis methodologies, surface functionalization approaches, network deposition techniques, and device integration processes. Academic institutions, national laboratories, and private companies across the United States, South Korea, China, and Japan have collectively generated an extensive body of patent filings covering various aspects of the core-shell nanowire value chain. For emerging companies and established materials suppliers seeking to commercialize Cu–Ag nanowire electrode products, navigating this IP landscape requires substantial legal due diligence and, in many cases, licensing negotiations that add cost and timeline uncertainty to product development programs. This structural restraint disproportionately disadvantages smaller innovators and startups relative to vertically integrated large corporations with established IP portfolios and cross-licensing agreements.

- Entrenched ITO Supply Chain Infrastructure and Customer Qualification Inertia: The transparent conductive electrode market has been built around ITO over several decades, resulting in deeply entrenched supply chain relationships, established equipment ecosystems, and validated device integration processes across the display, photovoltaic, and touchscreen industries. Device manufacturers operating within these established ITO-based ecosystems face significant switching costs when evaluating alternative electrode materials — including the need to re-optimize device architectures, requalify manufacturing processes, update design rules, and potentially retool deposition and patterning equipment. For high-volume consumer electronics applications where production yields and reliability specifications are exceptionally demanding, the qualification burden for new electrode materials is substantial. Overcoming this institutional inertia typically requires extended field demonstration programs, pilot-scale production partnerships, and reliability data accumulated over multiyear timescales.

Critical Market Challenges Requiring Innovation

Despite the protective function of the silver shell in Cu–Ag core-shell nanowires, ensuring complete, pinhole-free silver coverage across the entire copper nanowire surface remains a persistent manufacturing and reliability challenge. Incomplete or non-uniform shell formation exposes copper to atmospheric oxygen and moisture, initiating oxidation that progressively degrades electrical conductivity and device performance. Accelerated aging studies under elevated temperature and humidity conditions have documented measurable increases in sheet resistance over time in Cu–Ag nanowire networks that do not incorporate supplementary passivation or encapsulation strategies. Developing robust, industrially scalable shell deposition protocols that consistently deliver complete copper surface coverage without introducing structural defects in the nanowire morphology remains one of the field's most pressing technical imperatives.

Additionally, the overall sheet resistance of a Cu–Ag nanowire transparent electrode is governed not only by the intrinsic conductivity of individual nanowires but critically by the contact resistance at nanowire-nanowire junctions within the percolating network. These junctions are frequently coated with residual surfactants, polymer capping agents, or native oxide layers introduced during synthesis, all of which impede electron transport. Post-deposition treatments — including thermal annealing, photonic sintering, plasmonic welding, and chemical treatments — have been investigated to reduce junction resistance, but each approach carries trade-offs in terms of substrate compatibility, throughput, and process complexity. The absence of standardized performance benchmarking protocols specific to flexible transparent electrodes further complicates direct technology comparisons and slows adoption decisions among device manufacturers evaluating new electrode materials.

Vast Market Opportunities on the Horizon

- Rapid Growth of Flexible OLED Displays Creating High-Value Electrode Specification Opportunities: Flexible organic light-emitting diode (OLED) displays represent one of the highest-value and fastest-growing application segments for flexible transparent electrodes, driven by their adoption in foldable smartphones, rollable televisions, and automotive display systems. The technical requirements of flexible OLED architectures — including low sheet resistance, high optical transmittance, excellent mechanical durability under repeated bending, and compatibility with organic semiconductor processing conditions — align closely with the performance characteristics achievable through optimized Cu–Ag core-shell nanowire electrode designs. As display panel manufacturers expand their flexible OLED production capacity and explore next-generation foldable and stretchable display form factors, the opportunity for Cu–Ag nanowire-based transparent electrodes to secure design wins in this segment is substantial.

- Emerging Bioelectronics and Electronic Skin Applications Opening New Addressable Markets: The convergence of materials science, biomedical engineering, and electronics has given rise to a rapidly expanding domain of bioelectronic devices — including epidermal health monitoring patches, neural interface electrodes, electronic skin for robotic prosthetics, and implantable biosensors — that require transparent, flexible, and biocompatible conductive electrodes. Cu–Ag core-shell nanowires possess several properties well-suited to these emerging bioelectronic applications: their network morphology enables stretchability and conformability to curvilinear biological surfaces, their transparency supports optogenetic and optical monitoring applications, and the silver shell surface chemistry can be functionalized with biocompatible coatings to manage cytotoxicity concerns associated with copper. This intersection of flexible electrode technology with bioelectronics represents a nascent but high-growth market opportunity that conventional ITO-based electrode suppliers are structurally unable to address.

- Government-Funded Clean Energy and Advanced Manufacturing Programs Providing Commercialization Support: National and regional government programs targeting clean energy technology development, advanced manufacturing innovation, and critical materials supply chain diversification have increasingly directed funding toward next-generation photovoltaic technologies and the enabling materials that underpin them, including flexible transparent electrodes. In the United States, the European Union, South Korea, Japan, and China, research funding agencies and industrial policy programs have supported work on ITO-alternative transparent conductive materials as part of broader efforts to reduce dependence on indium supply chains and accelerate the commercialization of flexible and lightweight solar energy technologies. Government-supported research consortia and public-private partnership programs also create opportunities for Cu–Ag nanowire developers to build collaborative relationships with device manufacturers and end-users during the pre-commercial phase, reducing technical and market risk while accelerating the path from laboratory demonstration to industrial-scale deployment.

In-Depth Segment Analysis: Where is the Growth Concentrated?

By Type:

The market is segmented into Single-Layer Cu–Ag Core-Shell Nanowires, Multi-Layer Cu–Ag Core-Shell Nanowires, Hybrid Cu–Ag Nanowire Composites, and Ultra-Thin Cu–Ag Nanowire Networks. Single-Layer Cu–Ag Core-Shell Nanowires currently lead the market, favored for their straightforward synthesis process and cost-effective scalability. The copper core provides an economical conductive backbone, while the silver shell imparts superior oxidation resistance and enhanced surface conductivity. Multi-layer variants are increasingly gaining traction in high-performance applications where more rigorous environmental stability is required, and hybrid composite types integrating nanowires with conductive polymers or graphene-based materials are emerging as next-generation solutions for advanced flexible electronics development.

By Application:

Application segments include Flexible Displays & Touchscreens, Organic Solar Cells (OPV), Organic Light-Emitting Diodes (OLEDs), Wearable Electronic Devices, Electromagnetic Interference (EMI) Shielding, and others. Flexible Displays & Touchscreens dominate application-level demand, driven by the rapid proliferation of foldable smartphones, rollable screens, and next-generation human-machine interface technologies. The ability of these nanowire networks to maintain consistent electrical performance under repeated bending and stretching cycles makes them particularly suitable for dynamic display applications. Organic solar cells represent another high-growth application, as the nanowire electrodes enable lightweight, roll-to-roll compatible photovoltaic architectures, while OLED and wearable electronics segments are expected to exhibit among the highest growth rates going forward.

By End-User Industry:

The end-user landscape includes Consumer Electronics Manufacturers, Solar Energy & Photovoltaic Companies, Automotive & Transportation Industry, Healthcare & Medical Device Manufacturers, and Defense & Aerospace Organizations. Consumer Electronics Manufacturers constitute the leading end-user segment, as the relentless pursuit of thinner, lighter, and more flexible device form factors continues to drive substitution away from conventional ITO-based electrodes. Solar energy companies are increasingly integrating these electrodes into next-generation flexible photovoltaic modules, while healthcare device manufacturers are exploring their utility in conformal biosensors and epidermal electronics, appreciating the combination of biocompatibility, transparency, and mechanical durability that Cu–Ag nanowire electrodes uniquely offer.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/308916/-market

Competitive Landscape:

The global Copper–Silver Core-Shell Nanowire for Low-Cost Flexible Transparent Electrode market is at a relatively early commercial stage, characterized by a limited but growing number of specialized nanomaterial manufacturers and advanced materials companies. The market's competitive dynamics are shaped by proprietary shell deposition processes, dispersion formulation expertise, roll-to-roll coating compatibility, and the ability to demonstrate proven long-term oxidation resistance data to device manufacturer customers. Companies that have developed scalable synthesis capabilities for core-shell nanowire architectures — delivering electrodes with sheet resistances typically below 50 Ω/sq and optical transmittances above 85% — hold the strongest competitive positions. Several South Korean and Chinese manufacturers have scaled pilot production lines specifically targeting display and photovoltaic OEM supply chains, leveraging lower raw material and synthesis costs, while Japanese specialty chemical firms with existing metal nanoparticle ink businesses are extending their portfolios toward core-shell nanowire formulations.

List of Key Copper–Silver Core-Shell Nanowire Flexible Transparent Electrode Companies Profiled:

- DOWA Electronics Materials Co., Ltd. (Japan)

- Cambrios Advanced Materials Corporation (United States)

- Blue Nano Inc. (United States)

- C3nano Inc. (United States)

- Hefei Vigon Material Technology Co., Ltd. (China)

- Zhejiang Kechuang Advanced Materials Co., Ltd. (China)

- Nanopyxis Co., Ltd. (South Korea)

- Aiden Co., Ltd. (South Korea)

- Merck KGaA (Sigma-Aldrich Advanced Materials Division) (Germany)

- PlasmaChem GmbH (Germany)

The competitive strategy across leading participants is overwhelmingly focused on advancing shell deposition processes to enhance oxidation resistance, reducing nanowire synthesis costs through continuous flow and scalable solution-phase methods, and forming strategic vertical partnerships with display manufacturers, photovoltaic producers, and wearable electronics companies to co-develop application-specific electrode formulations and validate performance under real-world operating conditions, thereby securing long-term design wins and future demand.

Regional Analysis: A Global Footprint with Distinct Leaders

- Asia-Pacific: Is the dominant region in the global Cu–Ag Core-Shell Nanowire for Low-Cost Flexible Transparent Electrode market, holding the largest share driven by its expansive electronics manufacturing ecosystem, robust research infrastructure, and aggressive investment in next-generation display and photovoltaic technologies. Countries such as China, South Korea, Japan, and Taiwan are at the forefront of developing and adopting flexible transparent electrode solutions. Government-backed initiatives promoting advanced materials research and domestic semiconductor self-sufficiency have further accelerated the integration of novel nanowire-based electrode technologies across the region. China leads within Asia-Pacific owing to its unmatched scale in electronics manufacturing and an intensifying national focus on advanced nanomaterials, while South Korea and Japan contribute significant technological depth through their world-class display and semiconductor industries, both nations actively investing in ITO replacement strategies.

- North America: Represents a significant and innovation-driven market for Cu–Ag core-shell nanowire flexible transparent electrode technologies. The United States hosts a dense network of university research laboratories, national institutes, and start-up ventures focused on advanced nanomaterial development and flexible electronics. Funding from federal agencies and venture capital has supported exploratory and translational research in Cu–Ag core-shell nanowire synthesis and electrode fabrication, with demand notably influenced by the region's growing organic photovoltaics, flexible displays, and electronic skin sectors. North America's strong intellectual property environment encourages innovation but can also raise barriers to rapid cost-driven scale-up compared to Asia-Pacific counterparts.

- Europe: Europe's market is shaped by its strong academic research base, sustainability mandates, and strategic investments in green energy technologies. Leading research institutions across Germany, the Netherlands, the United Kingdom, and France are actively engaged in studying nanowire-based electrode materials for applications in organic solar cells, smart windows, and flexible lighting. The European Union's focus on reducing dependency on critical raw materials, including indium, creates a favorable environment for ITO alternatives such as Cu–Ag core-shell nanowire systems. Industry collaborations under EU-funded programs are facilitating technology transfer from laboratory to pilot-scale production, positioning Europe as a steady growth market with emphasis on quality, performance, and environmental compatibility.

- South America and Middle East & Africa: These regions represent the emerging frontier of the Cu–Ag Core-Shell Nanowire market. While currently at an early research and development stage with limited commercial-scale manufacturing infrastructure in place, growing investments in renewable energy — particularly solar photovoltaics — may in the medium term stimulate interest in cost-effective transparent electrode solutions. Government-led science and technology diversification strategies in Gulf nations and increasing academic activity in Brazil and South Africa are beginning to create ecosystems more receptive to advanced nanomaterial research, with meaningful commercial activity expected to develop as sustained investment and international knowledge transfer partnerships expand across both regions.

Get Full Report Here: https://www.24chemicalresearch.com/reports/308916/-market

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/308916/-market

About 24chemicalresearch

Founded in 2015, 24chemicalresearch has rapidly established itself as a leader in chemical market intelligence, serving clients including over 30 Fortune 500 companies. We provide data-driven insights through rigorous research methodologies, addressing key industry factors such as government policy, emerging technologies, and competitive landscapes.

- Plant-level capacity tracking

- Real-time price monitoring

- Techno-economic feasibility studies

International: +1(332) 2424 294 | Asia: +91 9169162030

Website: https://www.24chemicalresearch.com/