The E-Mobility Industry is undergoing a massive structural transformation worldwide, accelerated by stringent global carbon-emission mandates, aggressive corporate fleet electrification targets, and a rapid decline in lithium-ion battery production costs. As urban centers prioritize sustainable transit infrastructure, the shift from traditional internal combustion engine (ICE) vehicles to electrified alternatives has evolved from a regulatory checkbox into a multi-trillion-dollar market reality.

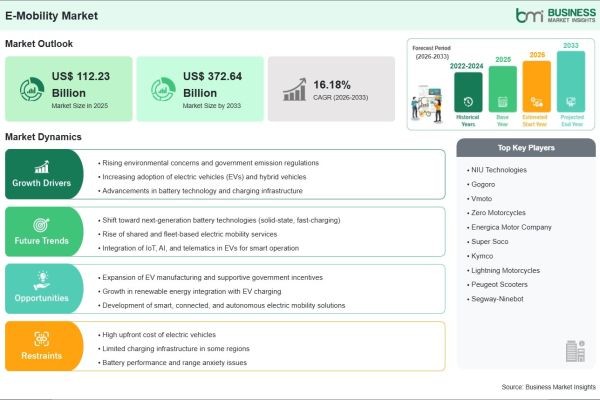

According to Business Market Insights, the global E-Mobility Market size is expected to reach US$ 372.64 Billion by 2033 from US$ 112.23 Billion in 2025. The market is estimated to record a CAGR of 16.18% from 2026 to 2033.

Technological breakthroughs in solid-state cell chemistries, silicon carbide (SiC) power electronics, and ultra-fast direct-current (DC) charging architectures are fundamentally reshaping the operational capabilities of electric powertrains. Top-tier manufacturers are aggressively investing in software-defined vehicle (SDV) frameworks, over-the-air (OTA) updates, and vehicle-to-grid (V2G) bi-directional power systems to smoothly integrate electric mobility platforms into the broader localized smart grid ecosystem.

Download Sample Report : https://www.businessmarketinsights.com/sample/BMIPUB00032702

What Is E-Mobility?

E-Mobility, or electric mobility, refers to the utilization of electric powertrains, localized energy storage systems, and connected digital solutions to propel transport platforms. This encompassing technology landscape covers a wide range of applications, including battery electric vehicles (BEVs), plug-in hybrid electric vehicles (PHEVs), fuel cell electric vehicles (FCEVs), electric micro-mobility solutions (e-bikes, e-scooters), and the high-voltage charging networks that support them.

Unlike traditional vehicles reliant on petroleum combustion, an e-mobility ecosystem leverages high-efficiency electric motors, advanced traction battery packs, and intelligent power management systems. This modern framework converts grid energy into motion with exceptionally high thermal efficiency, opening up opportunities for comprehensive fleet decarbonization, minimized maintenance cycles, and direct pairing with smart, renewable energy resources.

Market Drivers

A primary driver pushing the E-Mobility Industry forward is the continuous deployment of aggressive net-zero emissions policies and financial incentives by international governments. Financial subsidies, purchase tax exemptions, and structural penalties on carbon footprints are compelling commercial fleet operators and private consumers alike to swap their ICE units for electric models at an unprecedented rate.

Substantial technological cost-optimization in traction battery manufacturing represents another crucial growth variable. Increased factory automation, vertical raw-material supply integrations, and the broader commercial adoption of cost-effective chemistries like Lithium Iron Phosphate (LFP) have steadily reduced the total cost of ownership (TCO) for EVs, making them highly competitive with traditional fuel alternatives.

Furthermore, the dramatic expansion of high-power public charging infrastructure is significantly neutralizing consumer "range anxiety." The global deployment of high-voltage DC fast-charging networks across major transit corridors enables long-distance electric travel, heavily driving up mass-market vehicle adoption rates.

Additionally, the rising focus on corporate environmental, social, and governance (ESG) compliance is urging large logistics, distribution, and ride-hailing firms to rapidly electrify their last-mile delivery fleets, creating massive bulk-order backlogs for commercial electric vans and heavy trucks.

Market Segmentation

By Vehicle Type

- Passenger Electric Cars

- Electric Commercial Vehicles (Vans, Trucks, Buses)

- Electric Two-Wheelers & Three-Wheelers (Micro-Mobility)

- Industrial & Off-Highway Electric Vehicles

By Battery Type

- Lithium-Ion (NMC, LFP, NCA)

- Solid-State Batteries

- Lead-Acid and Nickel-Metal Hydride (NiMH)

By Voltage Range

- Low Voltage (Below 60V - Micro-Mobility)

- Medium Voltage (60V to 400V - Light Commercial & Hybrids)

- High Voltage (Above 400V to 800V+ - Premium BEVs & Heavy Trucks)

By Charging Ecosystem

- AC Residential Charging Systems

- Public DC Fast-Charging Stations

- Wireless Induction Charging Networks

The passenger electric cars segment accounts for the dominant share of global market revenue, driven by high consumer adoption and dense product pipelines from volume automotive brands. Concurrently, the electric commercial vehicles segment is logging the fastest compound annual growth rate, fueled by inner-city emission bans and a highly favorable TCO formula for high-mileage delivery fleets.

Regional Insights

- Asia-Pacific represents the largest and most dynamic e-mobility hub globally, led by China's dominant position in battery supply chains, heavy government infrastructure funding, and high domestic consumer demand for connected smart vehicles.

- Europe commands a substantial market position, heavily driven by strict Euro 7 vehicle emission mandates, localized internal combustion phase-out schedules, and robust consumer adoption across premium Western European markets.

- North America is accelerating its domestic deployment speed, supported by major federal funding frameworks for localized battery gigafactories and extensive highway charging network rollouts.

- Middle East & Africa and South & Central America are making steady structural progress, anchored by urban electric bus mass-transit upgrades and targeted luxury residential installations in expanding urban economies.

Top Players in the E-Mobility Industry

The global e-mobility landscape features intense competition among legacy automotive engineering heavyweights and agile, tech-first EV disruptors. Key competitors focus on securing long-term battery raw-material contracts, building out proprietary charging ecosystems, and deploying complex software platforms.

- Tesla, Inc.

- BYD Company Ltd.

- Volkswagen AG

- Toyota Motor Corporation

- BMW Group

- General Motors Company

- Stellantis N.V.

- Hyundai Motor Company

- Mercedes-Benz Group AG

- Nissan Motor Co., Ltd.

These corporations are pouring heavy capital expenditure into building localized assembly hubs, optimizing automated battery management software, and adapting new manufacturing platforms to drastically scale down overall structural production costs.

Technological Innovations

Rapid advances in power semiconductor engineering are yielding massive efficiency gains across modern e-mobility systems. The industry-wide transition from traditional silicon insulated-gate bipolar transistors (IGBTs) to Silicon Carbide (SiC) and Gallium Nitride (GaN) substrates allows vehicle inverters to operate at significantly higher temperatures with minimal switching losses, stretching overall driving range per charge cycle.

Furthermore, the shift to 800-volt powertrain architectures is gaining massive traction among premium vehicle platforms. This high-voltage architecture cuts required charging times in half compared to older 400-volt configurations, allowing vehicles to add hundreds of kilometers of range in under fifteen minutes of active connection.

Simultaneously, the industry deployment of unified interoperability standards, such as the cross-industry Matter and Megawatt Charging System (MCS) protocols, is systematically removing cross-brand friction, helping electric platforms interface cleanly with intelligent grid architectures, micro-grids, and decentralized residential solar installations.

Future Market Outlook

The long-term trajectory for the E-Mobility Industry remains exceptionally strong. As the global transport sector steadily detaches itself from fossil-fuel dependence, electric mobility platforms will continue to transform from simple zero-emission alternatives into fully integrated, bidirectional energy storage nodes on wheels.

The upcoming maturation of true solid-state battery cells—which promise double the volumetric energy density of current chemistry baselines while nearly eliminating thermal runaway risks—is poised to unlock completely new market horizons. Manufacturing entities that consistently secure resilient, ethically sourced battery materials, maintain deep digital software ecosystems, and lead in thermal efficiency designs will position themselves at the top of the global transport landscape.

Frequently Asked Questions (FAQs)

What is the difference between AC charging and DC fast charging?

AC (Alternating Current) charging relies on the vehicle's internal onboard charger to convert electricity into a usable format, making it ideal for slower overnight home charging. DC (Direct Current) fast charging delivers high-voltage power directly to the battery pack from an external station, bypassing the car's converter to charge the vehicle significantly faster.

How does Vehicle-to-Grid (V2G) technology benefit users?

V2G technology allows an electric vehicle to not only draw power from the local electricity grid but also pump excess stored energy back into it. This allows vehicle owners to act as grid stabilizers during peak demand periods, often earning energy credits or financial incentives in the process.

Are solid-state batteries currently used in mass-market e-mobility?

No, the majority of mass-market electric platforms currently run on liquid-electrolyte lithium-ion configurations. Solid-state battery systems are currently transitioning through advanced pilot-production testing phases, with broader commercial mass-market rollouts projected over the next few years.

How does colder weather impact the efficiency of electric powertrains?

Low ambient temperatures can temporarily slow down electrochemical reactions within a lithium-ion battery, slightly reducing active driving range and slowing charging speeds. Modern models combat this by integrating advanced heat pumps and intelligent pre-conditioning thermal management routines.

Browse More Reports:

https://www.businessmarketinsights.com/reports/asia-pacific-airway-management-devices-market

https://www.businessmarketinsights.com/reports/gcc-airway-management-devices-market

https://www.businessmarketinsights.com/reports/benelux-self-injection-device-market

About Us

Business Market Insights is a market research platform that provides a subscription service for industry and company reports. Our research team has extensive professional expertise in domains such as Electronics & Semiconductor; Aerospace & Defense; Automotive & Transportation; Energy & Power; Healthcare; Manufacturing & Construction; Food & Beverages; Chemicals & Materials; and Technology, Media, & Telecommunications.

Contact Us

If you have any questions about this report or would like further information, please contact us:

Contact person: Ankit Mathur

Email: sales@businessmarketinsights.com

Phone: +16467917070