To answer the question “what is event-driven architecture in insurance”, it is a design approach where insurance systems respond to real-time events—such as weather alerts, claims updates, or exposure changes—by automatically triggering workflows across underwriting, claims, pricing, and risk operations. Instead of relying on batch updates or siloed reporting, data flows continuously through an “event bus,” enabling insurers to react as soon as something happens in the real world.

In catastrophe (CAT) risk, this shift is becoming critical.

Real-time data is here—but real-time action is not

If you look strictly at capability, the insurance industry is closer than ever to operating in near real time during catastrophe events. Carriers can now ingest live hazard feeds, overlay them with exposure data, and identify impacted policyholders almost instantly. Agencies like the U.S. National Weather Service and NOAA’s National Centers for Environmental Information provide continuous updates on storm paths, rainfall intensity, wind speeds, and flood risk. Combined with geospatial analytics and AI models, insurers can now see where losses are likely to occur almost as they unfold.

Five years ago, this level of visibility would have been considered advanced. Today, it is standard.

But here is the problem: visibility has not translated into execution.

Decision latency is the real bottleneck

The biggest constraint in modern catastrophe risk operations is no longer data availability—it is decision latency, the time gap between signal and action.

Even with sophisticated CAT models from firms like Aon and large-scale IoT-driven claims insights highlighted in industry research (such as Gallagher reports), organizations still struggle to convert insights into immediate operational response.

That lag appears in three critical steps:

First, validating incoming data across multiple systems.

Second, assigning ownership of decisions.

Third, pushing approvals through layered governance structures.

Individually, these steps make sense. But during catastrophe conditions, they compound into delays that cost insurers billions.

In 2025 alone, global insured catastrophe losses reached approximately $130 billion, yet only about half of re/insurers used real-time analytics to actively guide response decisions. The rest were still reacting after the fact.

Why traditional insurance systems break during CAT events

The issue is not lack of intelligence—it is fragmentation.

Exposure data often sits in underwriting systems, claims imagery lives in adjuster platforms, and CAT intelligence is locked inside third-party modeling tools. These systems do not communicate in real time.

For example, during major wildfire events in the United States, tens of thousands of claims can be generated in days. Yet underwriting teams cannot dynamically adjust pricing or prioritize portfolios because hazard feeds and exposure systems are not connected in a live decision loop.

The result is a familiar pattern: data moves in minutes, but decisions move in hours—or longer.

Secondary perils such as floods following storms or fires following freezes now account for a majority of insured losses in many CAT years, yet workflows remain largely manual. Even when models predict these cascading risks accurately, the lack of automated execution prevents timely response.

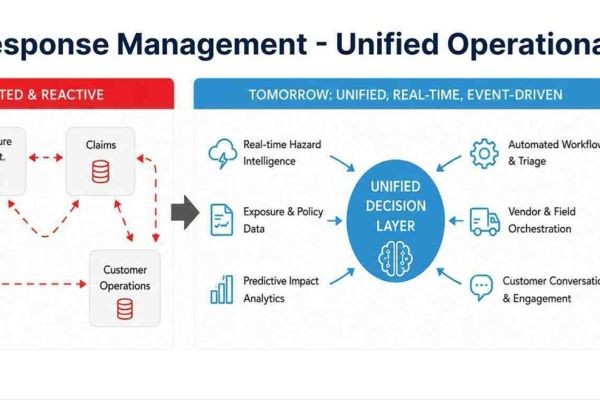

Event-driven architecture: the missing “decision bus”

This is where event-driven architecture becomes transformative.

Instead of treating systems as isolated databases what is event-driven architecture in insurance, platforms use a continuous stream of “events”:

- A hurricane changes path

- A wildfire crosses a boundary zone

- A policyholder’s property enters a flood zone

- A claim is filed with geotagged damage data

Each event triggers downstream actions automatically—without waiting for batch processing or human routing.

This creates what the industry has long lacked: a decision bus, where intelligence flows directly into action.

For example, when a flood warning is issued, the system can instantly:

- Flag exposed policies

- Pre-authorize emergency claim payments

- Notify policyholders

- Allocate adjusters to high-impact zones

All within minutes, not days.

Why this shift matters now

Catastrophe risk is becoming more frequent, more complex, and more interconnected. Climate volatility is increasing both primary and secondary perils, and regulators are tightening expectations around response times and consumer protection.

Post-event analyses, including those reviewed by insurance regulators after major U.S. disasters, consistently show the same issue: insurers often know what is happening in real time, but cannot act on it fast enough.

Event-driven architecture closes that gap.

The future: from reactive insurance to responsive ecosystems

The next evolution of insurance will not be defined by better models alone, but by how quickly those models translate into action.

Carriers that build real-time event-driven systems will move from reactive claims handling to proactive risk intervention. Instead of responding after losses escalate, they will intervene while events are unfolding.

In catastrophe insurance, speed is no longer a competitive advantage—it is an operational necessity. And event-driven architecture is the foundation that makes it possible.