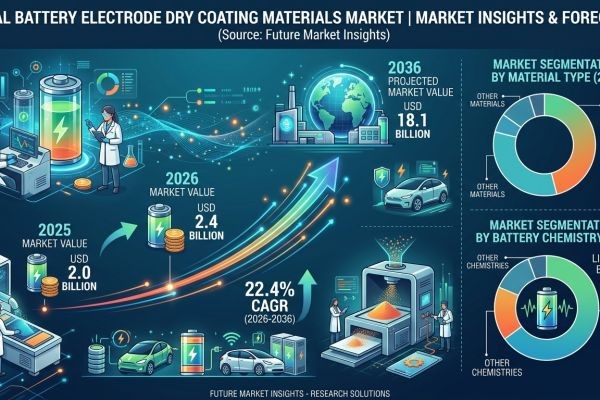

The global battery electrode dry coating materials market is projected to witness monumental expansion over the next decade, supported by the rapid industrialization of electric vehicle (EV) battery manufacturing and a strong push toward energy-efficient gigafactory architectures. The market is expected to grow dramatically, reaching approximately USD 18.1 billion by 2036, up from USD 2.4 billion in 2026, registering a remarkable CAGR of 22.4%, according to the latest analysis by Future Market Insights (FMI).

Market growth is being shaped by tightening environmental regulations targeting toxic solvent emissions, the need to reduce capital expenditures in battery manufacturing facilities, and the global transition toward energy-efficient production methods. Dry coating materials have evolved from a niche laboratory concept into an essential manufacturing breakthrough for high-volume automotive and energy storage cells.

While traditional wet coating methods rely on liquid dispersions, dry coating allows active materials, binders, and conductive additives to form cohesive electrode structures under mechanical shear. Manufacturers are increasingly integrating these solvent-free systems to eliminate extensive drying lines, optimize production speed, and achieve higher energy density within the cell structures.

Battery Electrode Dry Coating Materials Market Snapshot (2026–2036)

Market size outlook toward 2036: USD 18.1 billion Forecast CAGR: 22.4% Dominant material category: Binder systems Fastest-growing application segment: Electric vehicle batteries Key growth countries: China, South Korea, United States, Japan, Germany, India Primary demand channel: Gigafactory and OEM vehicle battery lines

Momentum in the Market

Beginning from an emerging commercialization base in 2026, the global battery electrode dry coating materials market demonstrates accelerated growth throughout the forecast period as eco-friendly manufacturing footprints become critical across major automotive economies. Between 2027 and 2030, expanding investments in global gigafactory construction and the rising necessity to minimize footprint requirements are expected to significantly boost demand for powder-to-film materials.

Increasing urbanization and massive energy transition goals are encouraging cell manufacturers and automakers to prioritize advanced electrode technologies. From 2030 onward, innovation in binder fibrillation performance, ultra-thick electrode architectures, and integration with next-generation solid-state batteries is expected to further strengthen market expansion. Highly efficient dry coating materials capable of supporting high-speed roll-to-roll electrode fabrication are emerging as key differentiators for leading battery suppliers.

The Reasons Behind the Market’s Growth

Demand for battery electrode dry coating materials is rising due to multiple structural and technological factors reshaping the global clean energy ecosystem.

Environmental Regulations Restricting Solvent Emissions Governments and regulatory bodies worldwide are enforcing strict rules to reduce toxic solvent usage, particularly N-Methyl-2-Pyrrolidone (NMP). Dry coating completely removes these hazardous chemicals from the processing floor, minimizing compliance risks and environmental impacts.

Gigafactory Investments and Large-Scale Battery Production The massive scaling up of battery manufacturing hubs requires major reduction in factory footprints and electricity consumption. By removing heavy drying ovens, dry coating slashes the thermal energy needed for electrode processing.

Pressure to Reduce Battery Production Costs Automobile manufacturers face persistent pressure to hit electric vehicle price parity with internal combustion engines. Dry processing lowers capital expenditure by simplifying production lines and boosting yield rates.

Rapid Expansion of Electric Vehicle Manufacturing The unprecedented volume demands of the global EV sector require robust material supply lines that can deliver consistent binder performance and superior electrochemical stability under high production speeds.

Top Segment Application Type

Electric Vehicle Batteries Lead Market Demand Electric vehicle applications account for the overwhelming majority of dry coating material consumption worldwide, supported by massive commercial cell contracts and specific manufacturing needs for ultra-high-capacity battery packs.

Material and Country Growth Analysis

- Binder systems: Central to the dry process, driving the core market through advanced shear fibrillation technologies.

- China: Projected 25.5% CAGR, led by massive gigafactory capacity scaling and vertically integrated battery chains.

- South Korea: Expected 24.2% CAGR, supported by global battery technology leadership and high-energy cell deployment.

- United States: Estimated 23.0% CAGR, fueled by domestic manufacturing incentives and EV localization.

- Japan: Anticipated 21.8% CAGR, driven by pioneering solid-state battery material research.

- Germany: Consistent 20.5% CAGR, backed by strict European carbon footprint mandates and domestic premium automotive lines.

- India: Expanding at an 18.2% CAGR, reflecting a strategic push to establish a domestic advanced chemistry cell ecosystem.

Regional Development: Key Manufacturing Hubs Drive Expansion

The global manufacturing landscape for advanced battery components is shifting toward high-tech regional corridors that balance raw material availability with localized automated assembly infrastructure.

- East Asia: Remains the volume powerhouse, leveraging deep industrial technical expertise to dominate early commercial rollouts of dry processing materials.

- North America: Rapidly building localized capacity, aided by government funding and joint venture gigafactories focused on reducing long-distance supply chain dependencies.

- Europe: Spearheading clean factory initiatives, where high energy costs create a strong direct financial incentive to discard traditional thermal-intensive dry rooms in favor of solvent-free lines.

Cooperative ventures between material innovators and tier-one battery manufacturers are optimizing processing parameters, paving the way for wider industrial adoption across various battery chemistries, including NMC and LFP.

Challenges, Trends, Opportunities, and Drivers

Drivers

- High expansion of electric vehicle manufacturing

- Substantial gigafactory investments globally

- Strict environmental laws curbing solvent usage

- Imperative to decrease battery production costs

Opportunities

- Seamless integration with solid-state battery tech

- Ultra-thick electrode architectures for enhanced energy density

- Modular micro-factory deployment layouts

- Material-to-cell developer strategic partnerships

Trends

- Complete structural shift toward solvent-free manufacturing

- Advanced AI and sensor-controlled dry calenders

- Focus on binder fibrillation and network stability

- Sustainability-driven life cycle assessments (LCA)

Challenges

- High precision requirements for powder processing

- Complex equipment retrofitting for existing lines

- Maintaining uniform material distribution at high speeds

The Competitive Environment

The global battery electrode dry coating materials market features a mix of advanced battery technology developers, specialty chemical corporations, and innovative manufacturing startups competing to commercialize scalable solvent-free lines. Key companies include:

- Tesla (Maxwell technology legacy)

- LiCAP Technologies

- LG Energy Solution

- Sakuu Corporation

- AM Batteries

- Solvay SA

- Arkema SA

These players are investing heavily in customized polymer binder compounds, conductive additives, and high-precision calendering setups. Competition increasingly centers on binder fibrillation performance, conductive network stability, compatibility with high-nickel cathode materials, and the ability to seamlessly integrate with high-speed, roll-to-roll electrode fabrication equipment.

Future Outlook: Toward Cleaner and Safer Battery Ecosystems

The global battery electrode dry coating materials market is entering a transformative decade shaped by automation, lower carbon footprints, and optimized energy densities. Future dry material formulations are expected to function as integrated material systems designed to work alongside next-generation cell designs like solid-state and sodium-ion platforms. As manufacturing methods mature and environmental regulations strengthen, dry coating materials will remain central to achieving highly sustainable and cost-effective energy storage ecosystems worldwide.

For a comprehensive strategic outlook and detailed analysis of technological developments shaping the industry, readers can explore the full report on the official Future Market Insights website: https://www.futuremarketinsights.com/reports/battery-electrode-dry-coating-materials-market