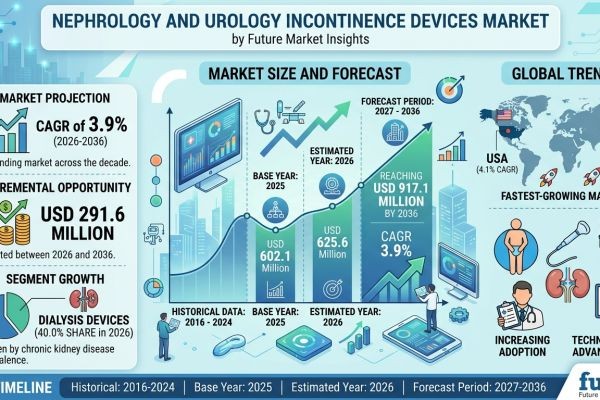

The global nephrology and urology incontinence devices market is projected to witness steady expansion over the next decade, supported by rising prevalence of chronic kidney disease (CKD) and growing demand for advanced urological management across the globe. The market is expected to grow steadily, reaching approximately USD 917.1 million by 2036, registering a CAGR of 3.9%, according to the latest analysis by Future Market Insights (FMI).

Market growth is being shaped by increasing investments in medical infrastructure, growing consumer awareness regarding continuous kidney care, and rapid adoption of advanced urological treatments. Incontinence and renal therapy devices have evolved from critical hospital infrastructure into essential solutions spanning ambulatory and home-based care. While traditional clinic setups continue to dominate device consumption, providers are increasingly integrating automated and patient-centric technologies to comply with modern healthcare expectations and improve patient outcomes.

Global Nephrology and Urology Incontinence Devices Market Snapshot (2026–2036)

Market size outlook toward 2036: USD 917.1 million

Forecast CAGR: 3.9%

Dominant end-user category: Hospitals and Clinics

Fastest-growing segment: Home Care and Outpatient Continence Management (~4.1% CAGR in USA)

Key growth countries: United States, United Kingdom, Japan, South Korea, Germany

Primary demand channel: Direct institutional procurement and medical supply channels

Momentum in the Market

Beginning from steady institutional adoption levels, the global nephrology and urology incontinence devices market demonstrates accelerated growth throughout the forecast period as home-based dialysis and outpatient treatments expand across multiple countries. Between 2026 and 2036, expanding end-stage renal disease (ESRD) therapeutic needs and rising geriatric populations are expected to significantly boost demand for integrated urology systems.

Increasing healthcare expenditure and higher incidence of lifestyle diseases like diabetes are encouraging healthcare systems and manufacturers to prioritize patient-centric technologies. From 2036 onward, innovation in non-invasive continence management devices and integration with digital health monitoring systems is expected to further strengthen market expansion. Smart devices capable of tracking real-time fluid dynamics and delivery rates are emerging as key differentiators in modern patient care.

The Reasons Behind the Market’s Growth

Demand for nephrology and urology incontinence devices is rising due to multiple structural and clinical factors reshaping the regional medical device ecosystem.

Rising Prevalence of Chronic Kidney Disease (CKD)

Growing instances of hypertension and diabetes globally are escalating the numbers of patients progressing to End-Stage Renal Disease (ESRD), requiring ongoing dialysis and continuous device support.

Expanding Aging Population Demographics

The aging global population significantly elevates the clinical incidence of urinary incontinence and pelvic floor issues, directly propelling market adoption across major medical segments.

Growing Infrastructure and Supportive Reimbursements

Established nephrology care networks and favorable institutional coverage policies—such as Medicare reimbursement for home dialysis therapies—are accelerating device procurement.

Shift Toward Home Care and Outpatient Care

Patients are increasingly prioritizing specialized home-based management solutions, accelerating product adoption beyond traditional hospital corridors.

Top Segment Application Type

Hospitals and Clinics Lead Market Demand

Institutional care centers account for the majority of nephrology and urology device utilization globally, supported by robust clinical infrastructure and continuous patient inflows requiring advanced intervention.

Device Type Analysis

Dialysis Devices and Equipment: Steady demand driven by persistent long-term therapeutic needs

Urinary Incontinence & Pelvic Organ Prolapse Devices: Expanding rapidly due to aging demographics

Urinary Stone Treatment Equipment: Rising application due to minimally invasive procedure trends

Benign Prostatic Hyperplasia (BPH) Treatment Devices: Growing with elevated male patient healthcare awareness

Regional Development: Established Networks and Reimbursements Drive Expansion

The global market landscape is heavily shaped by strong healthcare delivery systems across major developed and emerging economies:

United States: Market leader supported by Medicare home dialysis reimbursement and extensive clinic networks

United Kingdom & European Union: Steady growth anchored by well-established public healthcare coverage

Japan & South Korea: Rapidly expanding target demographics and robust localized care infrastructure

Localized partnerships between medical technology developers and clinical service providers are maximizing supply efficiency while expanding immediate therapy accessibility.

Challenges, Trends, Opportunities, and Drivers

Drivers

- High prevalence of CKD and ESRD

- Rising global aging demographics

- Favorable healthcare and home-care reimbursement policies

- Increased demand for specialized urological treatment

Opportunities

- Integrated digital health and sensor-based monitoring

- Minimally invasive stone and incontinence treatment platforms

- Specialized product lines tailored for home-care environments

- Collaborative clinical development with extensive dialysis chains

Trends

- Transition toward automated home dialysis systems

- Increased adoption of private and ambulatory care settings

- Focus on patient safety and comfort enhancement

- Sustainable and efficient product development loops

Challenges

- High maintenance and procurement costs for heavy equipment

- Complex regulatory approvals across distinct geographic markets

- Socio-economic disparities in advanced healthcare access

Country Growth Outlook (2026-2036)

The market's long-term trajectory is closely tied to therapeutic advancements and demographic shifts across key regional healthcare networks:

United States: 4.1% CAGR

Japan: 3.9% CAGR

South Korea: 3.8% CAGR

United Kingdom: 3.8% CAGR

European Union: 3.7% CAGR

The Competitive Environment

The global nephrology and urology incontinence devices market is moderately consolidated, with major medical device developers competing through clinical innovation, extensive distribution channels, and regulatory compliance. Leading companies include:

- Boston Scientific Corporation

- Coloplast A/S

- Medtronic plc

- Becton, Dickinson and Company (BD)

- Hollister Incorporated

- ConvaTec Group Plc

- Axonics, Inc.

These players are investing heavily in advanced implant portfolios, streamlined disposable designs, and home-compatible dialysis platforms while securing multi-year distribution contracts with top hospital networks.

Future Outlook: Toward Intelligent and Safer Mobility

The global nephrology and urology incontinence devices market is entering a transformative decade shaped by automation, patient-centric design, and accessible home care. Future treatment portfolios are expected to work alongside real-time diagnostic software to deliver personalized treatment schedules and minimize emergency hospitalizations. As medical systems adapt to demographic shifts, these devices will remain central to delivering better health outcomes globally.

For a comprehensive strategic outlook and detailed analysis of technological developments shaping the industry, readers can explore the full report on the official Future Market Insights website: https://www.futuremarketinsights.com/reports/nephrology-and-urology-incontinence-devices-market