A critical operational and structural modernization is reshaping global development pipelines, fueled by the physical necessity to deploy robust heavy construction vehicles capable of executing massive urbanization projects and upgrading aging civic infrastructure.

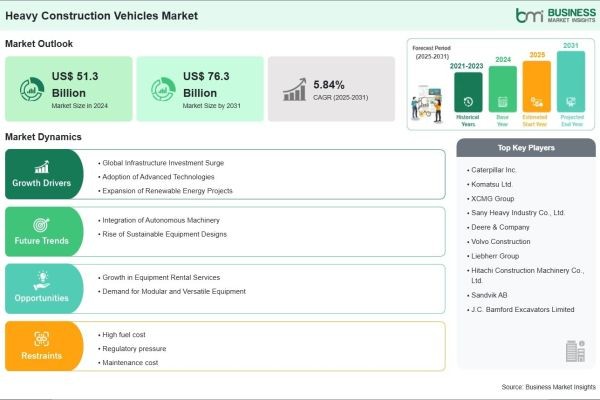

Based on market intelligence from Business Market Insights, the global Heavy Construction Vehicles Market is anticipated to reach US$ 76.3 Billion by 2031, mounting from its 2024 value of US$ 51.3 Billion at a projected CAGR of 5.84% from 2025 to 2031.

Recent shifts in environmental regulations and worksite safety standards are fundamentally altering market dynamics. Leading equipment manufacturers are heavily investing in telematics, automation, and alternative powertrains—specifically electric and hydrogen hybrid systems—to significantly increase operational efficiency while drastically reducing the carbon footprint of intensive construction sites.

Download Sample Report : https://www.businessmarketinsights.com/sample/BMIPUB00031691

What Are Heavy Construction Vehicles?

Heavy construction vehicles are purpose-built, heavy-duty machines designed to execute complex, high-stress tasks in earthwork, material handling, paving, and structural building. Unlike standard commercial trucks, these vehicles are engineered with specialized chassis, reinforced hydraulics, and immense torque capabilities to operate in off-road, rugged environments.

This category encompasses a wide array of specialized equipment. Dump trucks and articulated haulers are utilized for moving massive volumes of soil and aggregate. Concrete mixers and asphalt pavers are essential for roadwork and foundational pouring. Trenchers and rollers prepare the ground for utility laying and surface finishing. Together, these vehicles form the critical fleet required to execute modern civil engineering projects.

Market Drivers

The primary driver accelerating the Heavy Construction Vehicles Market is massive government-backed infrastructure investment. Developing nations are actively building new smart cities, transit networks, and energy grids from the ground up to support booming urban populations. Simultaneously, developed nations are injecting billions into repairing degrading bridges, highways, and water systems. This synchronized global building boom creates a massive, sustained baseline demand for new heavy equipment fleets.

Furthermore, the integration of advanced technology acts as a powerful market catalyst. Fleet managers are increasingly demanding telematics-enabled vehicles. These connected machines transmit real-time data on fuel consumption, hydraulic pressure, and component wear, allowing for predictive maintenance that minimizes costly worksite downtime. As project margins tighten, the ability to optimize fleet utilization through IoT and AI is forcing construction firms to upgrade older, traditional vehicles to smart, connected machines.

Additionally, the aggressive push toward sustainability is forcing a technological turnover. Stringent global emission regulations in major metropolitan areas are heavily penalizing traditional diesel engines. This is compelling major contractors to transition toward fully electric or hybrid construction vehicles, directly boosting sales of next-generation, zero-emission machinery.

Market Segmentation

By Vehicle Type

- Dump Trucks

- Concrete Mixers

- Asphalt Pavers

- Rollers

- Trenchers

- Others

By Fuel Type

- Diesel

- Electric

- Hybrid

By End-User

- Commercial Construction

- Industrial Construction

- Infrastructure Construction

The Dump Trucks segment holds the dominant market share by vehicle type, as they are universally required across all phases of mining, demolition, and site preparation. By fuel type, the Diesel segment currently commands the absolute majority of global volume due to its established infrastructure and high energy density required for heavy loads; however, the Electric segment is projected to register the fastest CAGR over the forecast period. By end-user, Infrastructure Construction remains the most lucrative segment, directly fueled by government-funded mega-projects and urban expansion initiatives.

Regional Insights

- Asia-Pacific commands the largest global market share and dictates industry volume. This absolute dominance is driven by immense infrastructure and real estate development in China and India. Mega-initiatives require unprecedented volumes of earthmoving and paving equipment, supporting a massive localized manufacturing ecosystem.

- North America holds a highly strategic market position characterized by fleet replacement and technological upgrades. Growth is propelled by aggressive government infrastructure spending and a strong residential/commercial building sector. The region heavily favors technologically advanced, fuel-efficient machinery that complies with strict EPA emission standards.

- Europe maintains a robust market position anchored by its strict environmental policies. European construction firms are leading the global charge in adopting electric heavy vehicles and establishing zero-emission construction sites, especially in urban centers across Scandinavia, Germany, and the UK.

- Middle East & Africa is experiencing rapid, concentrated growth. As Gulf nations diversify their economies away from oil, massive sovereign wealth is being poured into futuristic mega-projects. This is creating a sudden and massive demand for cutting-edge construction fleets in the region.

Top Players in the Heavy Construction Vehicles Industry

The competitive landscape is dominated by heavy engineering titans with deep pockets for R&D and expansive global dealer networks. Proving machine reliability in extreme conditions is the absolute key to brand loyalty and market share.

- Caterpillar Inc.

- Komatsu Ltd.

- Volvo Construction Equipment

- Hitachi Construction Machinery

- XCMG Group

- SANY Heavy Industry Co., Ltd.

- J C Bamford Excavators Ltd. (JCB)

- Liebherr Group

- Deere & Company

- Doosan Infracore

To sustain market dominance, these top-tier entities are engaged in a technology race. They are heavily acquiring robotics and AI startups to develop autonomous haulers and investing deeply in proprietary battery technologies to commercialize large-scale electric excavators and dump trucks.

Technological Innovations

Technological innovations in Autonomous and Semi-Autonomous Operation are redefining site safety and productivity. Facing severe shortages of skilled heavy equipment operators, manufacturers are developing AI-driven operating systems. Modern dump trucks and rollers can now be equipped with LiDAR, GPS, and computer vision, allowing them to navigate worksites, avoid obstacles, and perform repetitive tasks completely autonomously or via remote control from an off-site command center.

Furthermore, the breakthrough of High-Voltage Battery Systems is finally making heavy electrification viable. Historically, batteries were too heavy and lacked the energy density to power massive hydraulics for a full shift. New 800V architectures and advanced thermal management systems allow electric heavy vehicles to charge rapidly and deliver instantaneous, immense torque comparable to their diesel counterparts—all with zero exhaust emissions and minimal noise pollution.

Future Market Outlook

The long-term trajectory for the Heavy Construction Vehicles Market is inherently tied to the digitization of the construction industry. The future worksite will operate as a fully connected ecosystem. The market will see the widespread adoption of "Fleet Swarm" technology, where a centralized AI orchestrates the movements of dozens of autonomous heavy vehicles simultaneously to optimize material movement and eliminate idle time.

Moving forward, the industry will also see a strong pivot toward hydrogen fuel cell technology. While pure electric batteries are ideal for smaller urban machinery, hydrogen fuel cells are emerging as the superior zero-emission alternative for massive, high-tonnage mining and construction trucks operating in remote areas, offering rapid refueling times and the extreme power output required for the world's most demanding projects.

Frequently Asked Questions (FAQs)

Why are electric heavy construction vehicles becoming so popular?

Electric heavy vehicles produce zero direct emissions, which is essential for complying with strict new environmental laws in major cities. Additionally, electric motors have fewer moving parts, dramatically reducing maintenance costs, and they operate much quieter, allowing construction in urban areas during nighttime hours without violating noise ordinances.

What is telematics in construction equipment?

Telematics is the integration of sensors, GPS, and cellular technology within the vehicle. It allows the machine to constantly broadcast data about its location, fuel usage, engine health, and operator behavior to fleet managers in real-time, enabling them to spot maintenance issues before the machine breaks down.

How does autonomy work in heavy construction?

Autonomous construction vehicles use a combination of precise GPS mapping, radar, cameras, and artificial intelligence to "see" their environment. They can be programmed to follow exact paths, dump materials in precise locations, or compact soil to specific densities without a human in the cab, ensuring safety in hazardous zones.

Why does the Asia-Pacific region dominate this market?

The Asia-Pacific region, particularly China and India, is undergoing massive, state-sponsored infrastructure building phases—laying millions of miles of new roads, building entire new cities, and expanding ports—which requires an unprecedented volume of heavy construction machinery.

Browse More Reports:

https://www.businessmarketinsights.com/reports/benelux-pressure-monitoring-devices-market

https://www.businessmarketinsights.com/reports/middle-east-pressure-monitoring-devices-market

https://www.businessmarketinsights.com/reports/iot-implantable-cardiac-devices-market

About Us

Business Market Insights is a market research platform that provides a comprehensive subscription service for targeted industry and company intelligence reports. Our research team has extensive professional expertise across dynamic industrial domains such as Electronics & Semiconductor; Aerospace & Defense; Automotive & Transportation; Energy & Power; Healthcare; Manufacturing & Construction; Food & Beverages; Chemicals & Materials; and Technology, Media, & Telecommunications.

Contact Us

If you have any questions about this report or would like further information, please contact us:

Contact person: Ankit Mathur

Email: sales@businessmarketinsights.com

Phone: +16467917070