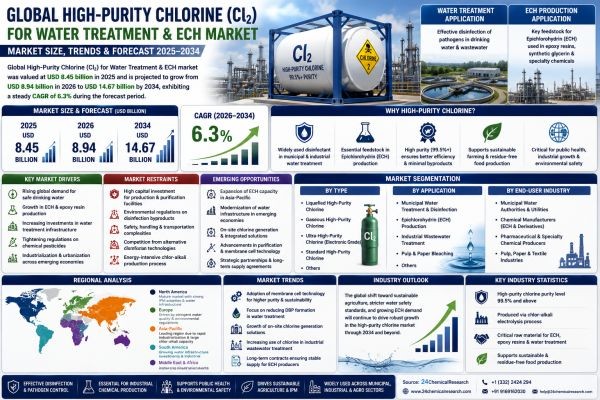

Global High-Purity Chlorine (Cl₂) for Water Treatment & ECH market was valued at USD 8.45 billion in 2025 and is projected to grow from USD 8.94 billion in 2026 to USD 14.67 billion by 2034, exhibiting a steady CAGR of 6.3% during the forecast period.

High-purity chlorine (Cl₂) occupies an indispensable position in the global chemical industry, serving two foundational roles that are unlikely to be displaced anytime soon. On one hand, it functions as the most widely deployed disinfectant in municipal and industrial water treatment systems worldwide, effectively eliminating pathogens, bacteria, viruses, and other harmful microorganisms from drinking water and wastewater streams. On the other hand, it serves as an essential feedstock in the production of epichlorohydrin (ECH)—a critical chemical intermediate used to manufacture epoxy resins, synthetic glycerol, and a wide range of specialty chemicals. This dual-market utility gives high-purity chlorine a uniquely resilient demand profile, one that is anchored in public health mandates on one side and industrial chemical growth on the other.

Get Full Report Here: https://www.24chemicalresearch.com/reports/308648/highpurity-chlorine-for-water-treatment-ech-market

Market Dynamics:

The market's trajectory is shaped by a complex interplay of powerful growth drivers, significant restraints that are being actively addressed, and vast, untapped opportunities across both established and emerging economies.

Powerful Market Drivers Propelling Expansion

- Rising Global Demand for Safe Drinking Water and Municipal Water Treatment Infrastructure: The global push to ensure access to clean and safe drinking water continues to be one of the most powerful forces driving demand for high-purity chlorine. Municipalities across both developed and developing economies are investing heavily in water treatment infrastructure, where chlorine remains the most widely deployed disinfectant due to its proven efficacy against a broad spectrum of pathogens, including bacteria, viruses, and protozoa. High-purity chlorine, specifically grades with purity levels of 99.5% and above, is increasingly preferred in water treatment applications because even trace-level impurities can generate harmful disinfection byproducts (DBPs), making purity a non-negotiable parameter for utilities operating under tightening regulatory scrutiny. The water treatment chemicals market, of which high-purity chlorine is a foundational input, is projected to grow at a compound annual growth rate exceeding 5% through the latter part of this decade, driven by urbanization, aging infrastructure replacement, and stricter potable water safety standards globally.

- Epichlorohydrin (ECH) Production Growth Fueling High-Purity Chlorine Consumption: Epichlorohydrin is a critical chemical intermediate primarily used in the production of epoxy resins, synthetic glycerin, and water treatment chemicals such as polyamide-epichlorohydrin (PAE) resins. The manufacturing of ECH via the allyl chloride route and the more modern glycerin-based route both require high-purity chlorine as a key feedstock. As global demand for epoxy resins expands—driven by construction, wind energy composites, automotive lightweighting, and electronics—ECH producers are scaling up capacity, which in turn intensifies demand for chlorine of consistent and elevated purity. Any deviation in chlorine purity directly impacts ECH yield and downstream product quality, making supply reliability a critical competitive differentiator for chlorine producers serving this segment.

- Industrialization and Urbanization Across Asia-Pacific and the Middle East Accelerating Infrastructure Investment: Beyond municipal applications, industrial water treatment—including cooling towers, boiler feed water systems, and process water in food and pharmaceutical manufacturing—is emerging as a significant and steadily growing demand center. Rapid urbanization across South Asia, Southeast Asia, and the Middle East is intensifying investments in new water treatment and distribution infrastructure, directly boosting chlorine consumption. These industrial users require not only consistent chlorine purity but also reliable on-site or near-site delivery infrastructure, because high-purity chlorine is typically handled as a liquefied gas under pressure, demanding stringent logistics and safety protocols. Producers capable of meeting both quality and supply chain requirements are well-positioned to capture expanding industrial water treatment contracts.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/308648/highpurity-chlorine-for-water-treatment-ech-market

Significant Market Restraints Challenging Adoption

Despite its entrenched position across multiple industries, the high-purity chlorine market faces structural restraints that temper the pace of volume growth and complicate market entry for new players.

- Environmental and Regulatory Pressure on Chlorinated Byproduct Formation: One of the most persistent structural restraints on the high-purity chlorine market—particularly in the water treatment segment—is the evolving regulatory landscape surrounding disinfection byproducts. Regulatory agencies including the U.S. EPA, the European Environment Agency, and the World Health Organization have progressively tightened maximum contaminant levels (MCLs) for DBPs in drinking water. Because DBP formation is a direct function of chlorine dose, organic matter content, and treatment conditions, utilities face a constrained optimization challenge: applying sufficient chlorine to ensure microbiological safety while minimizing DBP generation. This dynamic limits aggressive growth in chlorine dosing rates and encourages utilities to invest in upstream organic matter removal processes to reduce overall chlorine demand, moderating market volume growth even as the installed base of chlorinated treatment systems remains large and stable.

- Capital-Intensive Infrastructure Requirements Limiting Market Entry and Expansion: The production of high-purity chlorine requires substantial capital investment in membrane cell or diaphragm cell electrolysis technology, followed by liquefaction, purification, and filling infrastructure capable of meeting stringent purity specifications. Upgrading from standard-grade chlorine production to high-purity grades suitable for sensitive water treatment and ECH applications demands investment in advanced purification systems to remove impurities such as moisture, nitrogen trichloride (NCl₂), and other chlorinated compounds. These capital barriers restrict the number of qualified suppliers globally, leading to regional supply concentration risks and limiting the ability of the market to rapidly absorb demand surges. In developing regions where water treatment infrastructure investment is growing fastest, the lack of local high-purity chlorine production capacity can create import dependency and supply chain vulnerabilities.

Critical Market Challenges Requiring Innovation

The high-purity chlorine market contends with a set of operational and strategic challenges that require sustained innovation and capital commitment to overcome. Stringent handling, storage, and transportation regulations create significant operational complexity throughout the supply chain. Classified as a toxic gas under international chemical regulations including GHS (Globally Harmonized System) and subject to strict controls under frameworks such as the U.S. EPA's Risk Management Program (RMP) and OSHA's Process Safety Management (PSM) standard, chlorine handling demands robust engineering controls, continuous leak detection systems, emergency response infrastructure, and highly trained personnel. Compliance with these overlapping regulatory regimes adds meaningful operational cost for both producers and end-users.

Furthermore, competition from alternative disinfection technologies presents a moderate but growing challenge. Technologies such as ultraviolet (UV) disinfection, ozonation, and chloramination are gaining ground in municipal water treatment, particularly in markets where regulatory concern over chlorine-derived DBPs such as trihalomethanes (THMs) and haloacetic acids (HAAs) is intensifying. While these alternatives rarely replace chlorine entirely—residual disinfection in distribution systems still typically relies on chlorine—they can reduce the volume of chlorine required per treatment cycle, exerting moderate downward pressure on demand growth in mature, well-regulated markets. Additionally, raw material and energy cost volatility present ongoing headwinds. Chlorine is produced almost exclusively via the chlor-alkali electrolysis process, which is one of the most energy-intensive chemical manufacturing operations, with electricity typically representing 50–60% of total production costs for chlor-alkali facilities.

Vast Market Opportunities on the Horizon

- Expansion of ECH Capacity in Asia-Pacific Driven by Epoxy Resin and Specialty Chemical Demand: Asia-Pacific, led by China, has emerged as the dominant and fastest-growing region for ECH production and consumption, underpinned by the region's massive and expanding epoxy resin manufacturing base. China's construction sector, wind turbine manufacturing industry, and electronics supply chain collectively consume vast quantities of epoxy resins, sustaining robust ECH demand. As domestic ECH producers invest in capacity expansions and technology upgrades—including the shift toward the more sustainable glycerin-to-ECH route—the need for reliable, high-purity chlorine supply is increasing. This creates a clear commercial opportunity for chlor-alkali producers in the region to differentiate through purity guarantees, consistent supply agreements, and technical service support tailored to ECH manufacturers' quality requirements.

- Water Infrastructure Modernization in Emerging Economies Representing a Long-Term Demand Catalyst: Rapid urbanization across South Asia, Southeast Asia, Sub-Saharan Africa, and Latin America is generating sustained investment in new water treatment and distribution infrastructure. International development financing—from institutions such as the World Bank, Asian Development Bank, and regional development funds—is channeling capital into water and sanitation projects in countries where large portions of the population still lack reliable access to treated water. These programs are creating durable, long-cycle demand for water treatment chemicals including high-purity chlorine, as newly built treatment plants require both initial chemical inventory and ongoing operational supply. Chlorine producers with the logistics infrastructure and regulatory compliance capabilities to serve these markets are positioned to establish early competitive footholds in regions that will account for a growing share of global water treatment chemical consumption over the coming decade.

- On-Site Chlorine Generation and Integrated Solution Opportunities: The growing interest in on-site chlorine generation technology—using sodium chloride electrolysis to produce sodium hypochlorite or dilute chlorine at the point of use—is creating opportunities for technology providers and chemical companies to offer integrated solutions to utilities and industrial water users seeking to reduce transport risk while maintaining disinfection efficacy. While on-site generation competes with delivered liquid chlorine in some applications, it also expands the overall addressable market for chlorine-based disinfection by making it accessible to smaller-scale and remote water treatment operations that previously faced supply chain constraints.

In-Depth Segment Analysis: Where is the Growth Concentrated?

By Type:

The market is segmented into Liquefied High-Purity Chlorine, Gaseous High-Purity Chlorine, Ultra-High-Purity Chlorine (Electronic Grade), and Standard High-Purity Chlorine. Liquefied High-Purity Chlorine stands as the dominant type in this market, owing to its superior handling efficiency, ease of storage in pressurized cylinders, and logistical convenience for large-scale industrial consumers. Its concentrated form allows for precise dosing in water treatment facilities, making it the preferred choice for municipal and industrial operators seeking consistent disinfection performance. Gaseous chlorine, while essential for certain chemical synthesis applications including ECH production, requires stringent safety infrastructure, limiting its adoption to technically equipped facilities. Ultra-high-purity grades are increasingly sought after where contamination tolerances are extremely low, particularly in specialty chemical synthesis and pharmaceutical manufacturing.

By Application:

Application segments include Municipal Water Treatment & Disinfection, Epichlorohydrin (ECH) Production, Industrial Wastewater Treatment, Pulp & Paper Bleaching, and others. Epichlorohydrin (ECH) Production represents one of the most technically demanding and rapidly expanding applications for high-purity chlorine, driven by escalating demand for epoxy resins, synthetic glycerin, and water treatment chemicals derived from ECH. The stringent purity requirements in ECH synthesis make high-purity chlorine indispensable, as impurities can critically disrupt reaction yields and product quality. Municipal water treatment and disinfection also constitute a foundational application, underpinned by tightening regulatory frameworks worldwide governing safe drinking water standards. Industrial wastewater treatment is gaining momentum as environmental compliance obligations intensify across manufacturing sectors.

By End-User Industry:

The end-user landscape includes Municipal Water Authorities & Utilities, Chemical Manufacturers (ECH & Derivatives), Pharmaceutical & Specialty Chemical Producers, and Pulp, Paper & Textile Industries. Chemical Manufacturers engaged in ECH and derivative production emerge as the most technically sophisticated and volume-intensive end users of high-purity chlorine, demanding consistently high-grade supply to maintain process integrity and product compliance. Municipal water authorities and utilities constitute a large and stable end-user base, driven by public health mandates and government-regulated treatment protocols. The pharmaceutical sector, while smaller in volume, commands the highest purity thresholds and represents a premium revenue opportunity for suppliers capable of meeting pharmaceutical-grade chlorine specifications with full traceability and documentation.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/308648/highpurity-chlorine-for-water-treatment-ech-market

Competitive Landscape:

The global High-Purity Chlorine (Cl₂) for Water Treatment & ECH market is dominated by a concentrated group of large-scale integrated chemical manufacturers operating chlor-alkali facilities worldwide, and it is characterized by high capital barriers, technology-driven differentiation, and long-term contractual relationships with end users. Leading players such as Olin Corporation, Westlake Chemical Corporation, and INEOS Inovyn maintain significant competitive advantages through vertically integrated chlor-alkali operations, which allow them to produce chlorine at scale while co-producing caustic soda—a critical economic lever in cost management. Olin Corporation, headquartered in the United States, is among the largest chlorine producers globally, supplying both merchant chlorine for water treatment applications and captive chlorine for downstream derivatives including ECH. In Europe, Covestro AG and INEOS Inovyn represent major integrated chlorine producers with strategic positions in both the water treatment supply chain and ECH-linked epoxy resin production. Xinjiang Zhongtai Chemical and Tianyuan Group in China have emerged as dominant regional players benefiting from large-scale capacity expansions driven by domestic demand for water infrastructure and epoxy resin manufacturing.

Beyond the tier-one integrated producers, several specialized and regionally focused manufacturers play an important role in shaping market dynamics. Tokuyama Corporation in Japan and Hanwha Solutions Corporation in South Korea supply high-purity chlorine primarily to serve their domestic water treatment sectors and petrochemical industries, including ECH synthesis pathways. The competitive landscape is further shaped by tightening environmental regulations around chlorine handling, transportation, and mercury-free electrolysis mandates—factors that continue to consolidate production among well-capitalized, membrane cell-based manufacturers and progressively eliminate smaller legacy operators. The competitive strategy across the industry is overwhelmingly focused on operational efficiency, product purity certification, and forming strategic long-term supply agreements with key end-user companies to co-develop and validate supply chain solutions, thereby securing future demand.

List of Key High-Purity Chlorine (Cl₂) Companies Profiled:

- Olin Corporation (United States)

- Westlake Chemical Corporation (United States)

- INEOS Inovyn (United Kingdom / Belgium)

- Covestro AG (Germany)

- Solvay SA (Belgium)

- Tokuyama Corporation (Japan)

- Hanwha Solutions Corporation (South Korea)

- Xinjiang Zhongtai Chemical Co., Ltd. (China)

- Tianyuan Group Co., Ltd. (China)

- SPOLCHEMIE a.s. (Czech Republic)

Regional Analysis: A Global Footprint with Distinct Leaders

- Asia-Pacific: Stands as the dominant region in the high-purity chlorine market, driven by the region's rapid industrialization, expanding chemical manufacturing base, and increasing urgency around safe drinking water access. Countries such as China, India, Japan, and South Korea are at the forefront of chlorine consumption, with China commanding a particularly significant share owing to its large-scale chlor-alkali industry and extensive ECH production capacity. The region's growing population centers are placing heightened pressure on water infrastructure, spurring public and private investment in water treatment systems that rely on high-purity chlorine as a core disinfectant. Asia-Pacific hosts the world's largest chlor-alkali production capacity, and ongoing capacity additions alongside technological upgrades toward membrane cell technology are improving the purity levels achievable in chlorine production.

- North America: Represents a mature yet strategically significant market for high-purity chlorine in both water treatment and ECH applications. The United States maintains a well-established chlor-alkali industry, and chlorine continues to serve as the backbone of municipal drinking water disinfection across the country. Aging water infrastructure in many urban centers is prompting modernization investments that sustain demand for high-purity chlorine. Environmental regulations enforced by agencies such as the EPA impose rigorous standards on chlorine handling, storage, and application, encouraging the adoption of advanced membrane cell production methods and driving preference for higher-purity chlorine grades.

- Europe: Holds a prominent position in the high-purity chlorine market, underpinned by stringent water quality directives and a sophisticated chemical industry. The European Union's Drinking Water Directive and industrial emissions regulations compel water utilities and chemical producers to maintain high standards for chlorine purity. Germany, France, the Netherlands, and Belgium are key consuming nations, supported by an established chlor-alkali sector that has largely transitioned to membrane cell technology. Sustainability considerations are increasingly shaping procurement decisions, with a growing emphasis on minimizing chlorinated by-products in water treatment and reducing the environmental footprint of ECH production.

- South America and Middle East & Africa: These regions represent the emerging frontier of the high-purity chlorine market. South America, led by Brazil, is supported by ongoing efforts to extend safe drinking water access to underserved populations and expand industrial chemical production. In the Middle East and Africa, severe water scarcity has spurred significant investment in desalination and water treatment infrastructure, where chlorine plays a critical disinfection role. Gulf Cooperation Council countries, particularly Saudi Arabia and the UAE, are expanding water treatment capacity as part of broader water security strategies, while Africa's long-term growth prospects are supported by urbanization trends and increasing international development funding for water and sanitation projects.

Get Full Report Here: https://www.24chemicalresearch.com/reports/308648/highpurity-chlorine-for-water-treatment-ech-market

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/308648/highpurity-chlorine-for-water-treatment-ech-market

About 24chemicalresearch

Founded in 2015, 24chemicalresearch has rapidly established itself as a leader in chemical market intelligence, serving clients including over 30 Fortune 500 companies. We provide data-driven insights through rigorous research methodologies, addressing key industry factors such as government policy, emerging technologies, and competitive landscapes.

- Plant-level capacity tracking

- Real-time price monitoring

- Techno-economic feasibility studies

International: +1(332) 2424 294 | Asia: +91 9169162030

Website: https://www.24chemicalresearch.com/