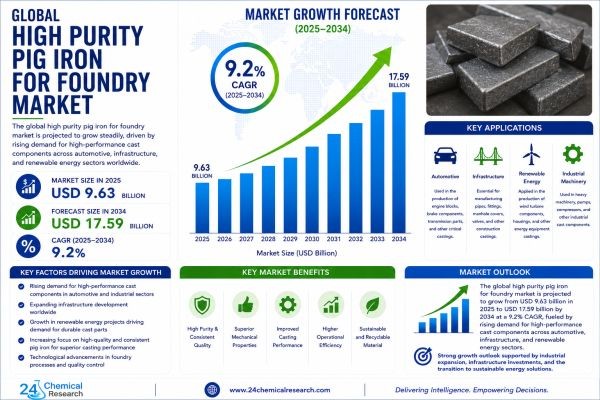

Global High Purity Pig Iron for Foundry Market was valued at USD 9.63 billion in 2025 and is projected to reach USD 17.59 billion by 2034, exhibiting a compelling CAGR of 9.2% during the forecast period.

The increasing demand for high-performance ductile iron castings, automotive foundry materials, wind turbine components, and premium metallurgical feedstock is significantly accelerating growth in the global High Purity Pig Iron for Foundry market. Rising investments in automotive manufacturing, infrastructure development, renewable energy projects, and precision engineering applications are further strengthening demand for low-impurity pig iron across global foundry operations.

High Purity Pig Iron (HPPI), characterized by exceptionally low levels of impurities like sulfur, phosphorus, and titanium, has emerged as a cornerstone material for producing high-performance cast iron components. Its superior metallurgical properties—including consistent carbon content, excellent fluidity, and enhanced mechanical strength—make it indispensable for manufacturing critical automotive, engineering, and infrastructure components. Unlike standard foundry pig iron, HPPI's stringent chemical composition ensures reduced casting defects, improved machinability, and superior performance in demanding applications. The growing use of HPPI in ductile iron production, engine blocks, brake systems, wind turbine hubs, heavy machinery parts, and precision castings is further supporting long-term market expansion.

Get Full Report Here: https://www.24chemicalresearch.com/reports/304839/high-purity-pig-iron-for-foundry-market

Market Dynamics:

The market's growth trajectory is shaped by a dynamic interplay of powerful expansion drivers, significant industry constraints, and substantial untapped opportunities across global manufacturing sectors.

Powerful Market Drivers Propelling Expansion

-

Automotive Industry's Shift Towards High-Performance Components: The global automotive industry, valued at over $2.7 trillion, is increasingly demanding high-integrity castings for engine blocks, brake systems, and transmission components. HPPI enables production of superior ductile iron that offers 20-30% better tensile strength and fatigue resistance compared to conventional materials. With electric vehicle production projected to reach 30 million units annually by 2030, the need for durable, lightweight cast components is creating sustained demand for premium feedstock materials like HPPI. Increasing demand for automotive casting materials, high-strength ductile iron, and precision foundry inputs is significantly supporting market growth.

-

Infrastructure Development and Renewable Energy Expansion: Global infrastructure investment exceeding $5 trillion annually is driving demand for heavy machinery and construction equipment that rely on high-strength cast iron components. Additionally, the wind power sector, expected to double its global capacity by 2030, requires massive HPPI-based castings for turbine hubs and structural parts. These components must withstand extreme environmental stresses, making material purity and consistency non-negotiable for manufacturers. Rising demand for renewable energy castings, construction machinery components, and heavy-duty engineering materials is further contributing to market expansion.

-

Technological Advancements in Foundry Processes: Modern foundries are adopting advanced melting and treatment technologies that require consistent, high-quality raw materials. HPPI's predictable composition allows for precise process control, reducing energy consumption by 15-20% and minimizing scrap rates. This efficiency gain is particularly valuable as foundries face increasing pressure to improve sustainability while maintaining competitive production costs. Growing adoption of advanced foundry technologies, low-defect casting processes, and sustainable metallurgical production methods continues driving demand for high-purity pig iron.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/304839/high-purity-pig-iron-for-foundry-market

Significant Market Restraints Challenging Adoption

Despite its advantages, the market faces considerable obstacles that must be overcome for broader adoption across the manufacturing sector.

-

High Production Costs and Economic Volatility: Producing HPPI requires sophisticated refining processes that elevate manufacturing costs by 25-40% compared to standard pig iron. This cost premium presents a significant barrier for foundries operating with thin profit margins. Furthermore, price volatility in key raw materials—particularly high-grade iron ore and coking coal—creates budgeting challenges, with annual price fluctuations of 15-25% adding uncertainty to long-term planning. Fluctuating energy costs, metallurgical coke prices, and premium-grade iron ore availability continue impacting production economics.

-

Competition from Alternative Feedstock Materials: High-quality steel scrap remains a formidable competitor, offering foundries a cost-effective alternative iron source in many applications. While scrap lacks HPPI's consistency, advanced sorting and processing technologies have improved its quality, making it attractive for non-critical components. This competition is particularly strong in price-sensitive market segments where the performance benefits of HPPI don't justify the additional material cost.

Critical Market Challenges Requiring Innovation

The transition from traditional foundry materials to premium HPPI presents several complex operational and technical challenges that industry participants must address.

Maintaining consistent quality at industrial scale remains difficult, with production yields often reaching only 70-80% of theoretical capacity due to stringent impurity control requirements. The specialized nature of HPPI production also creates supply chain vulnerabilities, as global capacity is concentrated among a limited number of producers in specific regions. This geographic concentration means logistical disruptions, trade policy changes, or regional instability can significantly impact global availability.

Additionally, the market contends with high customer switching costs. Foundries face substantial validation and requalification expenses when changing HPPI suppliers, as material consistency directly affects casting quality and production efficiency. This creates a barrier for new market entrants and reinforces the position of established producers with proven track records. Manufacturers are increasingly focusing on impurity control technologies, energy-efficient ironmaking processes, and advanced quality assurance systems to strengthen competitiveness.

Vast Market Opportunities on the Horizon

-

Expansion in Emerging Economies: Rapid industrialization across Asia-Pacific, Latin America, and Africa presents substantial growth opportunities. Countries like India, Vietnam, and Brazil are developing domestic manufacturing capabilities that require high-quality foundry materials. As these economies advance their automotive and infrastructure sectors, the demand for HPPI is expected to grow at 12-15% annually, significantly outpacing mature markets. Rising investments in domestic foundry capacity, automotive component manufacturing, and infrastructure equipment production are expected to create strong long-term opportunities.

-

Advanced Applications in New Industries: Emerging applications in aerospace, defense, and precision engineering sectors are creating new demand streams. These industries require components with exceptional mechanical properties and reliability, making HPPI an ideal feedstock. The aerospace sector alone is projected to consume 20% more cast components by 2030, driven by increased aircraft production and maintenance requirements. Growing demand for high-integrity castings, precision-engineered components, and safety-critical metallurgical materials is expected to further support market expansion.

-

Sustainability-Driven Material Upgrading: Increasing environmental regulations and sustainability initiatives are pushing foundries to adopt cleaner production inputs. HPPI's efficiency benefits align with these goals, as it enables reduced energy consumption and lower emissions during casting processes. This environmental advantage is becoming a key factor in material selection, particularly in regions with stringent emissions standards. Increasing focus on low-carbon foundry operations and reduced scrap generation is expected to strengthen HPPI adoption across advanced manufacturing sectors.

In-Depth Segment Analysis: Where is the Growth Concentrated?

By Type:

The market is segmented into Basic Grade, Nodular Grade, and other specialty grades. Nodular Grade currently dominates the market, preferred for its critical role in producing high-performance ductile iron castings. This grade's superior mechanical properties—including exceptional strength, toughness, and ductility—make it essential for demanding applications in automotive and heavy machinery sectors. Continuous improvements in production technology are further enhancing nodular grade's consistency and performance characteristics. Rising demand for nodular pig iron in high-strength automotive and engineering castings continues supporting segment growth.

By Application:

Application segments include Automobile, Engineering Machinery, Rail Transit, Wind Power, and other industrial uses. The Automobile segment represents the largest application area, accounting for over 35% of market volume. This dominance is driven by the extensive use of HPPI-based components in engines, drivetrains, and safety-critical systems. The Wind Power segment is expected to show the highest growth rate, driven by global investments in renewable energy infrastructure. Increasing use of HPPI in turbine hubs, rail components, heavy equipment castings, and industrial machinery parts continues driving application diversification.

By End-User Industry:

The end-user landscape includes Automotive, Heavy Machinery, Energy, Construction, and other manufacturing sectors. The Automotive industry maintains the dominant position, leveraging HPPI's properties for producing high-integrity components. The Energy and Construction sectors are emerging as significant growth markets, reflecting increased investments in infrastructure and renewable energy projects worldwide. Growing demand from heavy machinery manufacturers and renewable energy equipment producers is expected to further strengthen market growth.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/304839/high-purity-pig-iron-for-foundry-market

Competitive Landscape:

The global High Purity Pig Iron market is moderately consolidated, characterized by established global leaders and strategic regional players. The market's top three companies—Rio Tinto (Australia/UK), Kobe Steel Ltd. (Japan), and Eramet Group (France)—collectively command approximately 50% of the global market share as of 2025. Their dominance is supported by extensive production capabilities, technological expertise, and well-established customer relationships across key end-use industries.

List of Key High Purity Pig Iron Companies Profiled:

● Rio Tinto (Australia/UK)

● Kobe Steel, Ltd. (Japan)

● Eramet Group (France)

● TiZir Limited (Norway/UK)

● Longfengshan Casting Industry (China)

● Benxi Shentie Iron (China)

● China Hanking Holdings Limited (China)

● Meide Gengchen (China)

Competitive strategies primarily focus on capacity expansion, product quality enhancement, and developing long-term partnerships with major foundries. Companies are investing significantly in R&D to improve production efficiency and reduce costs, while also expanding their global distribution networks to serve emerging markets more effectively. Increasing focus on premium-grade pig iron, low-impurity metallurgy, and sustainable foundry feedstock solutions is expected to intensify market competition.

Regional Analysis: A Global Footprint with Distinct Leaders

● Asia-Pacific: Dominates the global market, holding over 60% share of total demand. This leadership is driven by massive manufacturing bases in China, Japan, and South Korea, particularly in automotive production and heavy industry. The region's rapid infrastructure development and growing renewable energy sector further bolster HPPI consumption. Local producers benefit from integrated supply chains and proximity to both raw materials and end-users. Expanding automotive component manufacturing and wind power equipment production continue strengthening regional demand.

● North America and Europe: Together account for approximately 30% of the global market. These mature markets are characterized by advanced manufacturing processes, stringent quality requirements, and strong demand from automotive and aerospace sectors. While growth rates are more modest than in Asia, these regions maintain significant market value due to their focus on high-performance applications and premium products.

● Rest of World: South America, Middle East, and Africa represent emerging markets with substantial growth potential. These regions are developing their industrial bases and infrastructure, creating new opportunities for HPPI suppliers. While currently smaller in scale, they offer long-term growth prospects as local manufacturing capabilities expand and quality requirements increase.

Frequently Asked Questions (FAQs)

-

What is High Purity Pig Iron used for?

High Purity Pig Iron is used in foundries to produce ductile iron, high-strength castings, automotive components, heavy machinery parts, wind turbine hubs, rail components, and precision engineering castings. -

Why is the High Purity Pig Iron market growing?

The market is growing due to rising demand from automotive manufacturing, infrastructure development, wind power equipment, heavy machinery, and advanced foundry applications requiring low-impurity metallurgical materials. -

Which industries use High Purity Pig Iron?

Major industries using High Purity Pig Iron include automotive, heavy machinery, construction equipment, renewable energy, rail transit, aerospace, defense, and precision engineering sectors. -

What are the advantages of High Purity Pig Iron?

High Purity Pig Iron offers low impurity levels, consistent carbon content, improved casting quality, reduced defects, better machinability, enhanced tensile strength, and superior performance in demanding foundry applications. -

Which region dominates the High Purity Pig Iron market?

Asia-Pacific dominates the global market due to its large automotive manufacturing base, heavy industrial output, infrastructure development, and growing renewable energy equipment production. -

What are the major challenges in High Purity Pig Iron production?

Major challenges include high production costs, raw material price volatility, strict impurity control requirements, limited global production capacity, supply chain concentration, and competition from steel scrap. -

How is the automotive industry impacting the High Purity Pig Iron market?

The automotive industry is significantly increasing demand for High Purity Pig Iron due to its role in producing high-integrity castings for engine blocks, brake systems, drivetrains, electric vehicle components, and safety-critical parts.

Get Full Report Here: https://www.24chemicalresearch.com/reports/304839/high-purity-pig-iron-for-foundry-market

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/304839/high-purity-pig-iron-for-foundry-market

About 24chemicalresearch

Founded in 2015, 24chemicalresearch has rapidly established itself as a leader in chemical market intelligence, serving clients including over 30 Fortune 500 companies. We provide data-driven insights through rigorous research methodologies, addressing key industry factors such as government policy, emerging technologies, and competitive landscapes.

● Plant-level capacity tracking

● Real-time price monitoring

● Techno-economic feasibility studies

International: +1(332) 2424 294 | Asia: +91 9169162030

Website: https://www.24chemicalresearch.com/