A consistent operational scale-up is redefining manufacturing press lines, automated tool-and-die design, and quality inspection workflows, fueled by the commercial necessity to deliver flawless, high-volume components capable of meeting strict quality benchmarks worldwide.

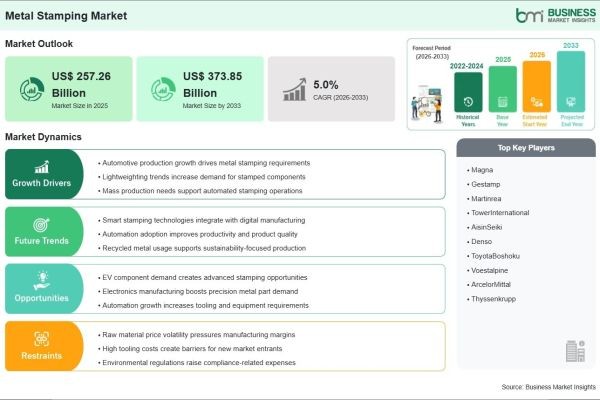

Based on market intelligence from Business Market Insights, the global Metal Stamping Market is anticipated to reach US$ 373.85 billion by 2033, mounting from its 2025 value of US$ 257.26 billion at a projected CAGR of 5.0% from 2026 to 2033.

Technological advancements in servo-driven presses, robotic automation, and digital quality-control systems are transforming the Metal Stamping Market. Manufacturers are increasingly integrating smart manufacturing practices and advanced die technologies to improve production efficiency, reduce material waste, and meet the stringent precision requirements of modern vehicle architectures and electronic devices. As the automotive industry—particularly the electric vehicle (EV) segment—continues to prioritize lightweight structures and thermal management, sophisticated metal stamping processes are emerging as a critical component for maintaining competitive, cost-effective, and high-volume production cycles.

Download Sample Report : https://www.businessmarketinsights.com/sample/BMIPUB00035660

What Is Metal Stamping?

Metal stamping is a cold-forming manufacturing process that uses dies and stamping presses to transform flat metal sheets into specific, complex shapes. The process involves various techniques such as blanking, punching, bending, coining, and embossing to create high-precision components. It serves as a foundational manufacturing step for producing mission-critical parts used across multiple industrial value chains.

The technology offers significant advantages, including the ability to achieve exceptional dimensional consistency, high production throughput, and significant material utilization efficiency. By utilizing advanced progressive and transfer die technologies, manufacturers can mass-produce intricate components like body panels, electrical connectors, brackets, and battery enclosures, ensuring structural integrity and performance reliability in the final assembled products.

Market Drivers

A major driver of the Metal Stamping Market is the surging demand for lightweight and high-strength metal components in the automotive and transportation sectors. As OEMs strive to improve fuel efficiency and extend the range of electric vehicles, they rely on stamped parts for vehicle body structures, chassis reinforcement, and crash safety assemblies. The transition to advanced high-strength steels (AHSS) and aluminum alloys requires sophisticated stamping capabilities to maintain part geometry while reducing total vehicle weight.

The rapid expansion of the consumer electronics and telecommunications industries is another powerful driver. Miniaturization in electronics requires high-precision stamped connectors, shielding plates, and heat sinks that can be produced in massive volumes with zero-defect tolerances. Metal stamping provides the cost-efficient, scalable solution needed to keep pace with the fast-moving product cycles inherent in the global electronics market.

The ongoing integration of automation and "smart" factory technologies is further expanding the market. The adoption of servo-controlled presses and IoT-enabled monitoring allows manufacturers to achieve higher levels of process repeatability and real-time quality control. This operational shift reduces production downtime, lowers scrap rates, and enables metal stamping facilities to operate with the flexibility required to support just-in-time manufacturing models.

Market Segmentation

By Process

- Blanking: Dominates the market as the foundational step for shaping raw sheet metal into functional forms, widely adopted for its efficiency in high-volume production.

- Bending: Utilized extensively for creating angles and structural forms in automotive frames and appliance casings.

- Embossing: Adds strength and aesthetic detail to metal surfaces, commonly used in paneling and interior components.

- Coining: Achieves extremely high precision and fine detail, essential for specialized electrical contacts and fasteners.

- Flanging: Provides necessary edges for structural assembly and rigidity in complex sheet metal housings.

By Application

- Automotive & Transportation: Represents the largest application segment, driven by the need for body panels, structural frames, and EV battery housing.

- Consumer Electronics: Registers high growth due to demand for compact, high-precision enclosures and connectors.

- Industrial Machinery: Requires robust, durable stamped components for heavy-duty operational hardware.

- Aerospace: Utilizes precision stamping for lightweight brackets, shielding, and interior fittings that meet strict safety standards.

- Electrical & Electronics: Relies on stamped busbars, terminals, and lead frames for power distribution.

By Press Type

- Mechanical Press: Remains the industry standard for high-speed, high-volume production due to consistent force delivery and cycle stability.

- Hydraulic Press: Preferred for deep-draw and complex forming operations where constant pressure control is critical.

- Servo Press: The fastest-growing segment, offering unmatched control over slide motion, stroke speed, and energy efficiency.

The automotive sector continued to anchor global demand in 2025, while the blanking process remained the leading method for scale-intensive operations, accounting for over 32% of total market revenue.

Regional Insights

- Asia-Pacific holds the largest share of the global market, anchored by China's dominant manufacturing output, rapid industrialization in India, and the widespread presence of high-volume electronics and automotive assembly lines.

- North America remains a highly significant market, driven by advanced manufacturing initiatives in the United States, significant investments in EV supply chains, and a robust aerospace sector.

- Europe continues to experience steady growth, fueled by strict vehicle emission standards, high-end engineering requirements, and the strong presence of legacy luxury automotive brands.

- Middle East & Africa is gradually emerging as a region for specialized industrial growth and regional infrastructure development.

- South & Central America is expanding its manufacturing base as regional automotive production volumes increase to serve localized consumer demand.

Top Players in the Metal Stamping Market

The market is highly competitive, featuring global automotive suppliers and specialized metal fabrication firms focusing on advanced die engineering and process automation.

- Gestamp Automoción, S.A.

- Magna International Inc.

- Toyota Motor Corporation

- Nissan Motor Co., Ltd.

- Ford Motor Company

- Kenon Holdings Ltd.

- FRP Holdings Inc.

- Aisin Corporation

- Tower International

- Martinrea International Inc.

These industry leaders continue to invest in servo-press technology, robotic material handling, and sustainable material sourcing to enhance production capabilities and maintain their competitive edge in high-precision markets.

Technological Innovations

Technological innovation is transforming the Metal Stamping Market through the development of servo-driven press technology, advanced digital die monitoring, and the use of sustainable, lightweight alloy materials. These advancements focus on maximizing output speed while maintaining strict quality control over complex geometries.

The shift toward servo-driven presses represents a massive leap in process flexibility. Unlike traditional mechanical presses, servo presses allow operators to program the exact speed and dwell time of the press ram at any point in the cycle. This control enables the stamping of difficult-to-form high-strength materials without tearing or excessive spring-back, directly supporting the trend toward thinner, stronger automotive parts.

Additionally, the integration of real-time IoT sensors into stamping dies allows for "predictive maintenance." By monitoring vibration, tonnage, and acoustic patterns, manufacturers can detect potential die fatigue or alignment issues before they result in defective parts or production stoppages. This transition to proactive, data-driven maintenance is significantly reducing total cost of ownership and increasing equipment uptime.

Future Market Outlook

The future outlook for the Metal Stamping Market remains strong. The ongoing electrification of the global vehicle fleet, the demand for compact electronic components, and the necessity for manufacturing efficiency will support robust market expansion through 2033.

As the sector navigates the dual demands of mass production and hyper-customization, metal stamping will evolve into a more digital and adaptive process. Companies that focus on integrating automated die-change technologies, optimizing energy consumption via servo-driven systems, and developing deep expertise in lightweight alloy stamping are positioned to secure dominant long-term growth opportunities.

Frequently Asked Questions (FAQs)

What is the projected size of the Metal Stamping Market by 2033?

The market is projected to reach US$ 373.85 Billion by 2033, rising from US$ 257.26 Billion in 2025.

What is the CAGR for the Metal Stamping Market?

The market is expected to grow at a CAGR of 5.00% from 2026 to 2033.

Which process segment dominates the market?

The blanking segment holds the largest market share due to its foundational role in mass production and widespread application across all major industries.

Which application segment leads the market?

Automotive & Transportation leads the market, driven by the high volume of stamped metal components required for vehicle bodywork, chassis, and safety systems.

Which region accounts for the largest share?

Asia-Pacific holds the largest market share, supported by large-scale manufacturing infrastructure and high consumer demand for automotive and electronics products.

Browse More Reports:

https://www.businessmarketinsights.com/reports/medical-supplies-market

https://www.businessmarketinsights.com/reports/neurointerventional-devices-market

https://www.businessmarketinsights.com/reports/spinal-fusion-devices-market

About Us

Business Market Insights is a market research platform that provides subscription service for industry and company reports. Our research team has extensive professional expertise in domains such as Electronics & Semiconductor; Aerospace & Defense; Automotive & Transportation; Energy & Power; Healthcare; Manufacturing & Construction; Food & Beverages; Chemicals & Materials; and Technology, Media, & Telecommunications.

Contact Us

If you have any questions about this report or would like further information, please contact us:

Contact person: Ankit Mathur

Email: sales@businessmarketinsights.com

Phone: +16467917070