Metamaterial electromagnetic bandgap (EBG) absorber sheets are engineered composite structures designed to suppress, absorb, or redirect electromagnetic waves across specific frequency bands. Unlike conventional absorbers, these materials derive their properties from precisely engineered periodic structures rather than chemical composition alone, enabling them to exhibit negative permittivity, negative permeability, or simultaneous negative values of both — characteristics not found in naturally occurring materials. This fundamental distinction gives EBG-based absorber sheets a decisive performance advantage across a growing range of demanding applications. They are widely deployed across defense, aerospace, telecommunications, and consumer electronics for electromagnetic interference (EMI) shielding, radar cross-section reduction, and antenna performance enhancement — and the breadth of that application base continues to widen as technology requirements become more stringent across virtually every industry.

Get Full Report Here: https://www.24chemicalresearch.com/reports/308669/metamaterial-absorber-sheet-market

Market Dynamics:

The market's trajectory is shaped by a complex interplay of powerful growth drivers, significant restraints that are being actively addressed, and vast, untapped opportunities that are beginning to attract sustained investment attention from both established players and well-funded new entrants.

Powerful Market Drivers Propelling Expansion

-

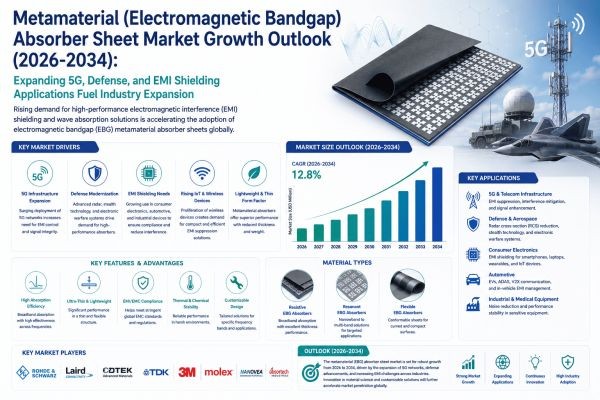

Surging Demand for Advanced EMI Shielding in Defense and Aerospace Applications: The metamaterial EBG absorber sheet market is experiencing significant momentum, primarily driven by the escalating demand for high-performance electromagnetic interference shielding solutions across defense and aerospace sectors. Modern defense platforms — including stealth aircraft, unmanned aerial vehicles, and naval vessels — require materials capable of absorbing radar and microwave frequencies across broad bandwidths without adding substantial weight or bulk. EBG-based absorber sheets fulfill this requirement by engineering periodic structures that suppress surface wave propagation and reflect electromagnetic energy within targeted frequency bands, making them a preferred choice over conventional foam or ferrite-based absorbers. The performance gap between EBG-based solutions and legacy absorbing materials has become increasingly difficult for defense procurement agencies to ignore, particularly as platform survivability requirements tighten and the electromagnetic threat landscape grows more complex.

-

Rapid Proliferation of 5G Infrastructure and Wireless Communication Systems: The global rollout of 5G networks has introduced complex electromagnetic compatibility challenges that traditional absorber materials are simply ill-equipped to handle. Operating across millimeter-wave frequencies — typically ranging from 24 GHz to 100 GHz — 5G base stations, small cells, and associated hardware generate dense electromagnetic environments prone to interference and signal degradation. Metamaterial EBG absorber sheets, engineered to operate effectively at these higher frequencies, are increasingly being integrated into antenna arrays, base station enclosures, and terminal devices to isolate radiating elements and improve overall signal integrity. The compactness and tunability of EBG structures make them particularly advantageous in densely packed 5G equipment where space constraints are critical. Furthermore, with emerging 6G research programs already validating EBG-based absorptive geometries in the sub-terahertz frequency range, the long-term demand pipeline extending well beyond the current decade is becoming increasingly well-defined.

-

Automotive Electrification and ADAS Sensor Proliferation Creating New Demand Streams: Beyond telecommunications, the automotive sector's accelerating transition toward electric vehicles and advanced driver-assistance systems is further reinforcing demand for metamaterial EBG absorber solutions. EVs contain numerous high-frequency electronic control units, LiDAR systems, and radar modules operating in the 77 GHz and 79 GHz bands that must coexist without electromagnetic interference. Metamaterial EBG absorber sheets are being evaluated and adopted by automotive OEMs and Tier-1 suppliers as a reliable solution for intra-vehicle EMC management. Leading automotive manufacturers across the United States, Europe, and China have initiated OEM-level qualification programs for EBG materials as standard EMC components within radar housings, supporting a broader and increasingly sustainable diversification of the market's end-use base that complements the traditionally dominant defense and aerospace demand channels.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/308669/metamaterial-absorber-sheet-market

Significant Market Restraints Challenging Adoption

Despite its considerable promise, the market faces structural hurdles that must be overcome to achieve broader commercial adoption and unlock the full scale of addressable demand across mid-tier and cost-sensitive application segments.

-

High Manufacturing Complexity and Cost Constraints Limiting Wider Commercialization: The most notable restraint remains the high cost and complexity associated with fabricating periodic metamaterial structures at commercial scales. Achieving the precise geometric patterning required for EBG functionality demands advanced manufacturing techniques such as photolithography, laser etching, or inkjet printing of conductive inks on flexible substrates. These processes require tightly controlled conditions and expensive capital equipment, which elevates production costs substantially relative to conventional absorber materials. For cost-sensitive markets such as consumer electronics and mid-range automotive applications, this pricing gap remains a significant barrier to adoption that has yet to be fully resolved, even as process innovations continue to close the gap incrementally.

-

Scalability Constraints and Supply Chain Immaturity Impeding Market Expansion: A primary restraint on the market is the relative immaturity of its manufacturing supply chain. The specialized raw materials required — including high-frequency substrates such as Rogers laminates, PTFE-based composites, and conductive inks with precise electrical properties — are sourced from a limited number of qualified suppliers globally. Any disruption in this supply base, whether due to geopolitical tensions, raw material shortages, or logistics constraints, can have a disproportionately large impact on production continuity. Furthermore, scaling up from prototype or small-batch fabrication to high-volume production without compromising the geometric precision essential to EBG performance is a technical challenge that many manufacturers have not yet fully resolved, creating a persistent gap between laboratory-demonstrated capability and commercially viable production throughput.

Critical Market Challenges Requiring Innovation

The transition from specialized defense procurement to broader commercial application presents its own distinct set of challenges. One of the inherent technical limitations of EBG-based absorbers is their tendency to exhibit peak absorption performance within relatively narrow frequency bands. While researchers have made meaningful progress in designing wideband and multiband EBG structures through multi-layer configurations and fractal geometries, achieving broadband absorption comparable to traditional carbon-loaded foam absorbers — particularly across sub-GHz to multi-GHz ranges simultaneously — remains an active area of research rather than a fully commercialized capability. This restricts applicability in scenarios requiring omnidirectional or ultra-wideband EMI suppression, which are precisely the conditions encountered in many of the fastest-growing application environments.

Additionally, the absence of universally recognized performance standards specific to metamaterial EBG absorbers creates procurement and qualification uncertainty, particularly for defense and aerospace customers who operate under rigorous material certification requirements. Without standardized test protocols defining how EBG absorber sheets should be characterized across frequency, temperature, and environmental stress parameters, procurement cycles tend to be extended and technically demanding. This slowdown affects market penetration even in cases where the technical merit of EBG solutions is well established and clearly superior to incumbent alternatives, creating a meaningful drag on revenue conversion from identified demand opportunities.

Vast Market Opportunities on the Horizon

-

Integration with Flexible and Conformal Electronics Opening New Application Frontiers: The convergence of metamaterial engineering with flexible electronics manufacturing represents one of the most compelling growth opportunities available to the EBG absorber sheet market today. Advances in roll-to-roll printing, screen printing of conductive inks, and flexible substrate technologies are progressively enabling the fabrication of EBG structures on conformable, lightweight sheets that can be applied to curved and irregular surfaces. This capability unlocks application opportunities across wearable health monitoring devices, conformal antenna systems for unmanned platforms, and flexible displays where managing electromagnetic emissions is critical to regulatory compliance and system performance. As flexible electronics manufacturing matures and unit costs decline, metamaterial EBG absorbers stand to benefit directly from expanded design freedom and access to new end-use markets that were previously inaccessible to rigid absorber formats.

-

Rising Investment in Quantum Computing and Advanced Semiconductor Facilities Creating Specialized Demand: Quantum computing infrastructure and next-generation semiconductor fabrication facilities operate in extraordinarily electromagnetically sensitive environments where even minor EMI can compromise qubit coherence or semiconductor lithography processes. This creates a specialized but high-value demand segment for metamaterial EBG absorbers capable of delivering precise, frequency-selective isolation within controlled laboratory and cleanroom environments. Several national governments and major technology corporations have announced substantial capital investments in quantum computing research infrastructure, suggesting that this niche but technically demanding segment will expand meaningfully over the coming years, providing a premium-priced, high-margin opportunity for EBG absorber sheet manufacturers capable of meeting stringent performance and cleanliness specifications.

-

Commercial Space and Low Earth Orbit Satellite Constellations as an Emerging High-Growth End-Market: The ongoing development of satellite constellations for low Earth orbit broadband communications presents an additional and rapidly expanding opportunity. Satellites operating in dense LEO constellations must manage inter-satellite electromagnetic interference while minimizing mass — a performance profile uniquely well-suited to metamaterial EBG absorber sheets, which offer superior frequency selectivity at significantly lower areal densities than conventional absorber materials. As commercial space activity intensifies and satellite manufacturing volumes increase substantially across multiple programs, the space segment is poised to become a strategically important and high-growth end-market for advanced metamaterial absorber technologies over the forecast period through 2034.

In-Depth Segment Analysis: Where is the Growth Concentrated?

By Type:

The market is segmented into Single-Layer EBG Absorber Sheets, Multi-Layer EBG Absorber Sheets, Frequency-Selective Surface (FSS) Based Absorbers, and Hybrid Metamaterial Absorber Sheets. Multi-Layer EBG Absorber Sheets represent the leading segment within this category, driven by their superior broadband electromagnetic absorption capability across multiple frequency ranges. The multi-layer architecture enables engineers to tailor impedance matching and loss mechanisms with a high degree of precision, making these sheets exceptionally suitable for demanding defense and aerospace applications. Hybrid metamaterial absorber sheets are also gaining notable traction as they combine the benefits of both traditional absorbing materials and structured EBG geometries, offering a compelling balance of performance, flexibility, and manufacturability for next-generation electromagnetic interference management solutions across both established and emerging application sectors.

By Application:

Application segments include Radar Cross Section (RCS) Reduction, Electromagnetic Interference (EMI) Shielding, Antenna Performance Enhancement, Wireless Communication Systems, and others. Radar Cross Section (RCS) Reduction stands as the dominant application segment, underpinned by growing strategic investments in stealth technology by defense establishments worldwide. EBG absorber sheets offer an unmatched ability to suppress backscattered electromagnetic waves across wide incident angles, making them indispensable for next-generation stealth platforms and low-observable military assets. EMI shielding is emerging as another highly critical application area, particularly as the proliferation of high-frequency electronics, 5G infrastructure, and automotive radar systems intensifies the need for robust electromagnetic compatibility solutions across both commercial and industrial end-use environments.

By End-User Industry:

The end-user landscape includes Defense and Military, Aerospace and Aviation, Telecommunications and Electronics, Automotive, and Healthcare and Medical Devices. Defense and Military continues to be the dominant end-user segment, as national defense agencies and prime contractors seek advanced electromagnetic absorption solutions to achieve radar stealth, electronic warfare superiority, and platform survivability in contested electromagnetic environments. The stringent performance requirements of this sector continually push material innovation boundaries, encouraging manufacturers to develop EBG sheets with enhanced durability and wide-angle absorption. However, Telecommunications and Electronics is a rapidly ascending end-user category, driven by the accelerating deployment of 5G networks and the miniaturization of electronic assemblies where managing electromagnetic interference is of paramount importance to system reliability and regulatory compliance.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/308669/metamaterial-absorber-sheet-market

Competitive Landscape:

The global Metamaterial (Electromagnetic Bandgap) Absorber Sheet market remains a highly specialized and technically demanding segment, populated predominantly by advanced materials manufacturers, defense contractors with in-house R&D capabilities, and university-affiliated spin-off companies. The market structure is moderately consolidated at the tier of established players, with competition driven by material performance specifications such as insertion loss, operating frequency range, and thickness constraints rather than price alone. Leading the competitive space are established RF and microwave absorber manufacturers such as Laird Performance Materials (United Kingdom/USA), Cuming Microwave Corporation (USA), and TDK Corporation (Japan), which collectively benefit from established supply chains, certified manufacturing processes, and existing relationships with aerospace, defense, and telecommunications OEMs. Their dominance is underpinned by extensive IP portfolios, simulation-validated product lines, and demonstrated track records of supply continuity under demanding procurement conditions.

At the niche and emerging player level, several smaller manufacturers and research-driven companies have carved out defensible positions by focusing specifically on metamaterial and EBG-based absorber architectures. The market continues to see entry from photonic and RF metamaterial startups as 5G, autonomous vehicle radar, and satellite communication demands accelerate requirements for thin, broadband, and angle-stable absorber solutions. Competition at this level centers on proprietary unit cell geometries, simulation-validated performance, and the ability to supply custom-dimensioned sheets at low-to-mid production volumes with short lead times. The competitive strategy across both tiers is overwhelmingly focused on R&D investment to enhance product performance and reduce costs, alongside forming strategic partnerships with end-user companies to co-develop and validate application-specific solutions, thereby securing future demand pipelines in a market where customer qualification cycles are long and incumbency advantages are strong.

List of Key Metamaterial (Electromagnetic Bandgap) Absorber Sheet Companies Profiled:

-

Laird Performance Materials (United Kingdom / USA)

-

TDK Corporation (Japan)

-

AGC Inc. (Japan)

-

Withwave (South Korea)

-

API Technologies (USA)

-

Mast Technologies (USA)

-

Metaboards Ltd. (United Kingdom)

-

Murata Manufacturing Co., Ltd. (Japan)

Regional Analysis: A Global Footprint with Distinct Leaders

-

North America: Stands as the leading region in the Metamaterial EBG Absorber Sheet Market, driven by a combination of robust defense investment, advanced research infrastructure, and a well-established ecosystem of technology developers and end-users. The United States is home to several pioneering research institutions and defense-oriented organizations that have long prioritized electromagnetic compatibility and stealth technology applications. The region's dominance is reinforced by consistent government funding channeled through defense agencies toward next-generation electromagnetic management materials, alongside the rapid proliferation of 5G infrastructure and the growing complexity of electronic systems in automotive and consumer electronics sectors that have further expanded the addressable market beyond purely defense-oriented demand.

-

Europe & Asia-Pacific: Together, they form a powerful and rapidly growing secondary bloc. Europe's strength is driven by a strong tradition of precision engineering, a well-funded defense sector with active programs in Germany, France, the United Kingdom, and Sweden, and the European Union's emphasis on technological sovereignty that has spurred domestic research and collaborative pan-European programs. Asia-Pacific, meanwhile, is emerging as one of the fastest-growing regions, propelled by escalating defense modernization programs, rapid expansion of telecommunications infrastructure, and a growing base of electronics manufacturing across China, Japan, South Korea, and India. China's substantial investment in indigenous defense technologies and its expansive 5G deployment programs have created particularly significant opportunities for EBG absorber sheet manufacturers operating or expanding in the region.

-

South America and Middle East & Africa: These regions represent the emerging frontier of the EBG absorber sheet market. While currently smaller in scale, they present meaningful long-term growth opportunities driven by defense modernization efforts, incremental telecommunications infrastructure development, and growing awareness of electromagnetic compatibility requirements. Brazil's air force and navy modernization programs have introduced selective demand for advanced electromagnetic materials, while in the Middle East, countries such as Saudi Arabia, the United Arab Emirates, and Israel represent active procurement markets driven by defense modernization and electronic systems upgrades. Partnerships with international technology providers are expected to play a key role in enabling broader market development across both regions over the medium to long term.

Get Full Report Here: https://www.24chemicalresearch.com/reports/308669/metamaterial-absorber-sheet-market

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/308669/metamaterial-absorber-sheet-market

About 24chemicalresearch

Founded in 2015, 24chemicalresearch has rapidly established itself as a leader in chemical market intelligence, serving clients including over 30 Fortune 500 companies. We provide data-driven insights through rigorous research methodologies, addressing key industry factors such as government policy, emerging technologies, and competitive landscapes.

-

Plant-level capacity tracking

-

Real-time price monitoring

-

Techno-economic feasibility studies

International: +1(332) 2424 294 | Asia: +91 9169162030

Website: https://www.24chemicalresearch.com/