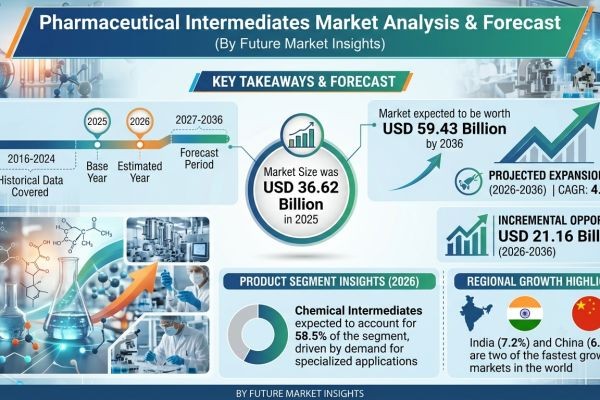

The global pharmaceutical intermediates market is projected to witness strong expansion over the next decade, supported by rising demand for generic drugs and increasing pharmaceutical R&D investments across the globe. The market is expected to grow steadily, reaching approximately USD 59.4 billion by 2036, registering a CAGR of 4.5%, according to the latest analysis by Future Market Insights (FMI).

Market growth is being shaped by increasing regulatory requirements, growing institutional modernization, and rapid adoption of advanced performance-validated technologies. Pharmaceutical intermediates have evolved from basic chemical building blocks into essential, high-quality regulatory-compliant components required for the synthesis of active pharmaceutical ingredients (APIs). While chemical intermediates continue to dominate procurement, manufacturers are increasingly expanding specialized capabilities to comply with modern safety expectations and improve final drug formulation outcomes.

Global Pharmaceutical Intermediates Market Snapshot (2026–2036)

- Market size outlook toward 2036: USD 59.4 billion

- Expected market value by 2026-end: USD 38.3 billion

- Forecast CAGR: 4.5%

- Dominant product category: Chemical Intermediates (58.5% share)

- Fastest-growing category segment: Generic Drug Intermediates (54.2% share)

- Key growth countries: India, China, Germany, USA, Saudi Arabia

- Primary demand channel: CMO and CRO manufacturing integration

Momentum in the Market

Beginning from steady regional adoption levels, the global pharmaceutical intermediates market demonstrates accelerated growth throughout the forecast period as regulatory compliance becomes mandatory across multiple countries. Between 2026 and 2036, expanding generic drug manufacturing and rising global disease burdens are expected to significantly boost demand for integrated formulation systems. Increasing aging populations and higher clinical trial pipelines are encouraging governments and drug manufacturers to prioritize outsourced production technologies.

From 2036 onward, innovation in custom intermediate synthesis and integration with green chemistry practices is expected to further strengthen market expansion. Smart manufacturing architectures capable of optimizing scalability based on molecule complexity and regulatory alignment are emerging as key differentiators in new supplier models.

The Reasons Behind the Market’s Growth

Demand for pharmaceutical intermediates is rising due to multiple structural and technological factors reshaping the global healthcare ecosystem.

Expansion of Generic Drug Manufacturing

Governments and health institutions are expanding generic drug access to manage escalating healthcare costs, driving large-scale procurement of certified intermediates.

Growing R&D Investments and Pipelines

Rapid expansion of advanced therapeutic pipelines, particularly for complex and chronic diseases, is increasing reliance on high-quality specialized intermediates.

Rising Outsource and Procurement Models

Pharmaceutical brands are prioritizing flexible manufacturing models by outsourcing production to CMOs and CROs to reduce structural infrastructure costs.

Infrastructure Modernization

The rise of sophisticated production lines in emerging hubs is creating specialized demand for performance-validated and high-purity chemical blocks.

Top Segment Application Type

Chemical Intermediates Lead Market Demand

Chemical intermediates account for the majority of installations across manufacturing lines, supported by their established cost-effectiveness and broad compatibility.

Application Analysis

- Analgesics & Anti-inflammatory Drugs: Steady demand driven by universal consumption.

- Cardiovascular & Anti-diabetic Drugs: High CAGR supported by chronic disease prevalence.

- Antimicrobial & Anti-cancer Drugs: Fastest-growing therapeutic segments due to precision pipeline expansion.

Regional Development: Global Manufacturing Ecosystem Drives Expansion

The global space is rapidly evolving into a consolidated procurement hub for pharmaceutical components, supported by cost-efficient production and expanding supplier networks.

- India: Regional production leader expanding rapidly with a projected 7.2% CAGR.

- China: Following close behind at a 6.4% CAGR, driven by infrastructure modernization.

- USA & Germany: Advanced biopharmaceutical innovation hubs maintaining steady growth.

Localized manufacturing partnerships between global suppliers and regional contract manufacturers are improving supply chain efficiency while accelerating technology adoption.

Challenges, Trends, Opportunities, and Drivers

Drivers

- Expansion of generic drug ecosystems

- Rising global disease burden and aging population

- Increasing clinical trial pipelines and drug approvals

- Demand for scalable, high-volume production capabilities

Opportunities

- High-purity, compliance-aligned intermediate lines

- Green chemistry and sustainable synthesis processes

- Specialized intermediates for custom drug formulations

- Integration with outsourced contract development platforms

Trends

- Shift from fragmented suppliers to consolidated procurement

- Strategic collaborations across the pharma value chain

- Increased focus on regulatory filing and validation assistance

- Technology transfer and operational optimization workflows

Challenges

- Cost pressures for entry-level procurement contracts

- Tightening international regulatory frameworks and guidelines

- Complex supply chain logistics across global hubs

Country Growth Outlook

The market’s growth trajectory is closely tied to pharmaceutical industrialization and regulatory implementation across major world economies:

- India: Manufacturing leadership and strong generics ecosystem.

- China: Expanding vehicle production capacity and rising quality standards.

- Germany: Advanced biotechnology innovation and quality benchmarks.

- USA: High biopharmaceutical spending and stringent FDA compliance.

The Competitive Environment

The global pharmaceutical intermediates market is moderately consolidated, with Tier 1 providers competing through innovation, localized manufacturing, and regulatory compliance, while Tier 2 and Tier 3 players leverage regional specialization.

Leading and emerging companies include:

- Chiracon GmbH

- Codexis, Inc.

- A.R. Life Sciences Private Limited

- Dishman Group

- Dextra Laboratories Limited

These players are investing heavily in advanced synthesis technologies, sustainable materials, and scalable production systems while forming long-term partnerships with major pharma buyers to strengthen supply chains.

Future Outlook: Toward Intelligent and Safer Mobility

The global pharmaceutical intermediates market is entering a transformative decade shaped by automation, regulatory consolidation, and stricter efficacy expectations. Future intermediate production lines are expected to function as integrated validation modules working alongside digital process tracking and real-time monitoring. As international markets mature and safety awareness strengthens, certified intermediates will remain central to achieving reliable and high-performance therapeutic ecosystems throughout the healthcare sector.

For a comprehensive strategic outlook and detailed analysis of technological developments shaping the industry, readers can explore the full report on the official Future Market Insights website: https://www.futuremarketinsights.com/reports/pharmaceutical-intermediates-market