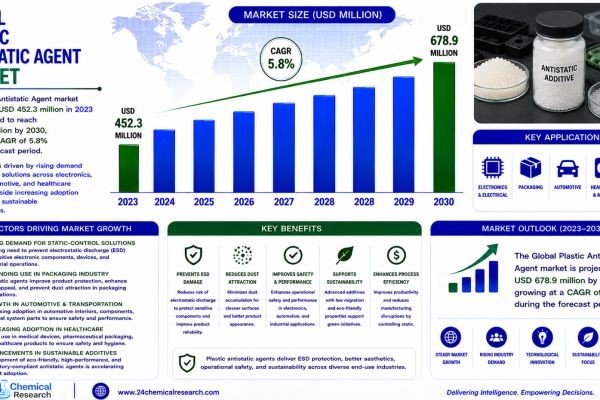

Global Plastic Antistatic Agent market was valued at USD 452.3 million in 2023 and is projected to reach USD 678.9 million by 2030, exhibiting a steady CAGR of 5.8% during the forecast period.

Plastic antistatic agents have evolved from being niche additives to essential components in modern polymer processing. These specialized chemical compounds - including ethoxylated amines, glycerol esters, and quaternary ammonium compounds - mitigate static electricity buildup that can cause serious operational challenges in plastic applications. Their ability to dissipate charges while maintaining material properties makes them indispensable across electronics, packaging, automotive, and industrial sectors where static control is mission-critical.

Get Full Report Here: https://www.24chemicalresearch.com/reports/265733/global-plastic-antistatic-agent-market-2024-2030-185

Market Dynamics:

The market growth trajectory reflects a balancing act between robust industrial demand and evolving regulatory landscapes, with innovative formulations emerging to bridge performance gaps in increasingly sophisticated applications.

Powerful Market Drivers Propelling Expansion

- Electronics Industry Demands: The global electronics sector, valued at over $3 trillion, drives 38% of antistatic agent consumption. Miniaturization trends and sensitivity of microelectronics to electrostatic discharge (ESD) have created rigorous static control requirements, particularly in semiconductor packaging where damage can occur at voltages as low as 100V. Modern antistatic formulations reduce surface resistivity from 1013 to 108 ohms/sq, effectively preventing component failures during manufacturing and end-use.

- Packaging Innovation: Food and pharmaceutical packaging standards increasingly mandate static control to prevent dust attraction and explosion hazards. The migration from conductive carbon black to transparent antistatic agents has enabled compliance without compromising package aesthetics - a critical factor for brand differentiation. Global flexible packaging demand, expected to exceed $300 billion by 2027, presents a substantial growth avenue for transparent antistatic solutions.

- Automotive Electrification: The transition to electric vehicles has increased static-sensitive applications in battery components and interior surfaces. High-performance antistatic compounds now play dual roles - preventing charge accumulation in battery module housings while meeting flame retardancy requirements. With EV production projected to grow at 24% CAGR through 2030, this represents a high-potential sector for specialized antistatic solutions.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/265733/global-plastic-antistatic-agent-market-2024-2030-185

Significant Market Restraints Challenging Adoption

While demand grows, material scientists face persistent challenges in developing next-generation antistatic agents.

- Regulatory Complexities: REACH and FDA compliance creates formulation hurdles, particularly for migratory additives that could leach into food or medical products. Recent restrictions on long-chain alkyl phenols have forced reformulation of 25-30% of commercial antistatic products, with compliance timelines extending 12-18 months for new formulations.

- Performance-Longevity Tradeoffs: Migratory agents typically provide 6-12 months of surface effectiveness before depletion, requiring over-engineering in durable goods. Permanent antistatic additives based on conductive polymers can add 15-20% to material costs, creating economic barriers for price-sensitive applications.

Critical Market Challenges Requiring Innovation

The industry faces technical obstacles that require collaborative solutions between formulators and end-users. Achieving consistent surface resistivity below 109 ohms/sq in polyolefins remains particularly challenging, with some formulations showing 30-40% performance variation across production batches. Furthermore, maintaining effectiveness after secondary processing like thermoforming or injection molding often requires customized additive packages.

Supply chain volatility also poses challenges, with key raw materials like ethoxylated amines experiencing 8-12% annual price fluctuations. These market dynamics incentivize development of bio-based alternatives and more efficient application methods to maintain cost competitiveness.

Vast Market Opportunities on the Horizon

- Advanced Healthcare Applications: The medical device sector presents untapped potential for static-dissipative polymers used in surgical tools, diagnostic equipment, and drug delivery systems. New medical-grade antistatic compounds demonstrate <1% extractables while meeting ISO 10993 biocompatibility standards - a critical advancement for implantable devices.

- Smart Packaging Solutions: Integration of antistatic properties with active packaging functionalities (moisture control, oxygen scavenging) creates value-added solutions. Recent developments in multilayer films combine 108 ohm/sq surface resistivity with 50% reduction in water vapor transmission rates - addressing both static and shelf-life concerns.

- Circular Economy Compatibility: The shift toward polymer recyclability drives demand for non-migratory antistatic agents that don't interfere with repurposing streams. Novel polymer-bound additives maintain effectiveness through multiple processing cycles while meeting increasingly stringent recyclate purity standards in Europe and North America.

In-Depth Segment Analysis: Where is the Growth Concentrated?

By Type:

The market divides between Permanent Antistatic Additives and Migratory Antistatic Agents. Permanent additives, though 20-30% more expensive, dominate high-value applications like medical devices and automotive interiors where long-term performance justifies premium pricing. Migratory agents remain preferred for cost-sensitive, short-lifecycle products like packaging films.

By Application:

The Packaging segment leads current demand, consuming 45% of global antistatic agent volume, driven by food and pharmaceutical safety requirements. However, the Electronic segment shows strongest growth potential (7.2% CAGR) as semiconductor manufacturing scales to meet IoT and 5G deployment needs.

By End-User Industry:

While Packaging Manufacturers represent the largest current market, Automotive Tier 1 Suppliers are emerging as key adopters of advanced antistatic solutions. The intersection of electrification and autonomous driving creates new requirements for static control in sensor housings and battery components that conventional additives cannot meet.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/265733/global-plastic-antistatic-agent-market-2024-2030-185

Competitive Landscape:

The global Plastic Antistatic Agent market features a blend of specialty chemical giants and niche additive specialists. The top five players - Croda, Clariant, BASF, Arkema, and DuPont - collectively hold 58% market share through their extensive product portfolios and global distribution networks. Competition increasingly focuses on developing sustainable, high-performance solutions that address evolving regulatory and application requirements.

List of Key Plastic Antistatic Agent Companies Profiled:

- Croda (UK)

- Clariant (Switzerland)

- Kao Chemicals (Japan)

- Avient (U.S.)

- BASF (Germany)

- Baerlocher (Germany)

- Cargill (U.S.)

- Corbion (Netherlands)

- Arkema (France)

- Emery Oleochemicals (Malaysia)

- ADEKA (Japan)

Competitive strategies emphasize collaborative development with resin producers and converters to create application-specific solutions. Recent years have seen increased M&A activity as majors seek to bolster their technical capabilities in response to market fragmentation.

Regional Analysis: A Global Footprint with Distinct Leaders

- Asia-Pacific: Commands 48% of global consumption, driven by China's electronics manufacturing and packaging sectors. The region's 6.3% CAGR outpaces global averages, supported by rapid industrialization and foreign investment in high-tech manufacturing facilities.

- Europe: Represents 28% market share with stringent regulatory standards pushing innovation in sustainable antistatic solutions. Germany and Italy lead in automotive and industrial applications, while Scandinavian countries drive developments in biobased additives.

- North America: Accounts for 19% of the market, with strong demand from the medical device and specialty packaging sectors. The U.S. remains the innovation hub, accounting for 60% of recent patent filings in advanced antistatic technologies.

Get Full Report Here: https://www.24chemicalresearch.com/reports/265733/global-plastic-antistatic-agent-market-2024-2030-185

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/265733/global-plastic-antistatic-agent-market-2024-2030-185

About 24chemicalresearch

Founded in 2015, 24chemicalresearch has rapidly established itself as a leader in chemical market intelligence, serving clients including over 30 Fortune 500 companies. We provide data-driven insights through rigorous research methodologies, addressing key industry factors such as government policy, emerging technologies, and competitive landscapes.

- Plant-level capacity tracking

- Real-time price monitoring

- Techno-economic feasibility studies

International: +1(332) 2424 294 | Asia: +91 9169162030

Website: https://www.24chemicalresearch.com/