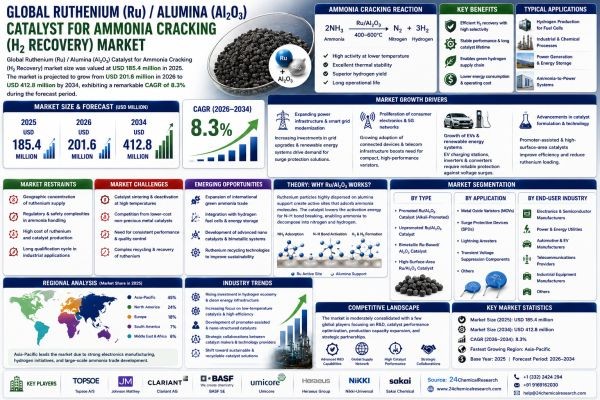

Global Ruthenium (Ru) / Alumina (Al₂O₃) Catalyst for Ammonia Cracking (H₂ Recovery) market size was valued at USD 185.4 million in 2025. The market is projected to grow from USD 201.6 million in 2026 to USD 412.8 million by 2034, exhibiting a remarkable CAGR of 8.3% during the forecast period.

Ruthenium supported on alumina (Ru/Al₂O₃) catalysts are high-performance heterogeneous catalysts specifically engineered to facilitate the thermocatalytic decomposition of ammonia (NH₃) into hydrogen (H₂) and nitrogen (N₂). Alumina serves as a thermally stable, high-surface-area support that enhances ruthenium dispersion, thereby maximizing catalytic activity at lower operating temperatures — typically in the range of 400°C to 600°C. These catalysts are central to ammonia cracking systems designed for on-site, on-demand hydrogen recovery, making them a critical enabling technology for the emerging hydrogen economy. The market is gaining significant momentum driven by the accelerating global transition toward clean hydrogen as an energy carrier and the growing adoption of ammonia as a practical hydrogen storage and transportation medium. Key industry participants such as Haldor Topsoe (Topsoe A/S), Clariant AG, and Johnson Matthey are actively developing and commercializing advanced Ru/Al₂O₃ catalyst formulations to meet evolving industrial requirements.

Get Full Report Here: https://www.24chemicalresearch.com/reports/308736/-market

Market Dynamics:

The market's trajectory is shaped by a complex interplay of powerful growth drivers, significant restraints that are being actively addressed, and vast, untapped opportunities.

Powerful Market Drivers Propelling Expansion

- Rising Global Demand for Green Hydrogen as a Clean Energy Carrier: The accelerating global transition toward decarbonization has positioned hydrogen — particularly green hydrogen — as a cornerstone of future energy systems. Ammonia cracking, which thermally decomposes ammonia (NH₃) into nitrogen and hydrogen, has emerged as one of the most practical pathways for hydrogen recovery and distribution, given ammonia's well-established storage and transportation infrastructure. Ruthenium supported on alumina (Ru/Al₂O₃) catalysts are widely recognized as among the most active materials for this reaction, offering superior low-temperature activity compared to conventional iron- or nickel-based systems. As governments across the European Union, Japan, South Korea, and Australia continue to scale up hydrogen economy roadmaps, the demand for efficient ammonia decomposition catalysts is experiencing meaningful upward pressure. National hydrogen strategies and stimulus programs — including Japan's Green Innovation Fund, the European Hydrogen Bank, and analogous programs in Australia and the United States — have collectively allocated substantial capital toward hydrogen infrastructure, creating durable, long-term procurement demand for high-performance catalysts.

- Ammonia's Established Role as a Hydrogen Storage and Transport Vector: One of the most compelling structural drivers for Ru/Al₂O₃ catalyst adoption is ammonia's inherent advantage as a hydrogen carrier. Liquid ammonia contains approximately 17.6 wt% hydrogen by mass and can be liquefied at relatively mild conditions, making it far more energy-dense and easier to handle than compressed or liquefied hydrogen. This logistical practicality has driven major economies to invest in ammonia-to-hydrogen supply chains, particularly for long-distance intercontinental hydrogen trade routes being developed between Australia, the Middle East, and East Asian importers. Ruthenium catalysts are integral to on-site cracking terminals where high hydrogen recovery efficiency is operationally critical, cementing their role in this emerging value chain. Furthermore, Ru/Al₂O₃ catalysts demonstrate significantly lower activation temperatures for ammonia decomposition compared to non-precious metal alternatives, enabling more energy-efficient hydrogen recovery at practical operating conditions — a key performance advantage as energy costs remain a central concern in green hydrogen economics.

- Technological Advancements in Catalyst Formulation Enhancing Commercial Viability: Ongoing research into promoter-assisted Ru/Al₂O₃ systems — incorporating alkali metals such as cesium (Cs) or barium (Ba) as electronic promoters — has meaningfully improved turnover frequencies and reduced ruthenium loading requirements. Lower ruthenium loading without sacrificing activity directly addresses one of the primary cost concerns associated with precious metal catalysts, improving the economic case for large-scale deployment. Additionally, advances in alumina support engineering, including the development of high-surface-area and thermally stable γ-Al₂O₃ and θ-Al₂O₃ phases, have contributed to improved catalyst longevity under the high-temperature cycling conditions typical of industrial ammonia cracking reactors. These incremental but cumulative improvements are strengthening the competitive positioning of Ru/Al₂O₃ systems against emerging alternatives, making the technology increasingly attractive to project developers and infrastructure investors alike.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/308736/-market

Significant Market Restraints Challenging Adoption

Despite its promise, the market faces hurdles that must be overcome to achieve universal adoption.

- Geographic Concentration of Ruthenium Supply Chain Creating Structural Vulnerability: The supply of ruthenium is geographically concentrated in a small number of producing nations, with South Africa accounting for the dominant share of global platinum group metal (PGM) output from which ruthenium is co-recovered. This concentration introduces geopolitical and logistical risks that can translate into price volatility and supply interruptions for catalyst manufacturers. For industries planning large-scale infrastructure deployments — such as gigawatt-scale ammonia cracking terminals — this supply chain fragility represents a strategic restraint that procurement teams and project financiers must account for in risk assessments. Diversification of ruthenium sourcing or development of efficient recycling and recovery processes for spent catalysts are being explored but remain at early stages of industrial maturity.

- Regulatory and Safety Complexities Associated with Ammonia Handling Infrastructure: Ammonia is a hazardous substance subject to stringent regulatory oversight across transportation, storage, and processing operations in virtually all major markets. The permitting, environmental impact assessment, and safety compliance requirements associated with building ammonia import and cracking terminals add time, cost, and uncertainty to project development timelines. These regulatory barriers can delay the deployment of ammonia cracking infrastructure and, by extension, suppress near-term catalyst procurement volumes. While existing agricultural and chemical industry infrastructure provides a regulatory framework to build upon, adapting these frameworks for energy-scale ammonia handling — particularly in jurisdictions without established ammonia import facilities — introduces additional complexity that can slow market development for Ru/Al₂O₃ catalysts in new geographies.

Critical Market Challenges Requiring Innovation

The transition from pilot-scale success to commercial-scale ammonia cracking presents its own set of formidable challenges. Catalyst sintering and deactivation under high-temperature operating conditions remain persistent technical concerns. At sustained elevated temperatures — typically ranging from 400°C to over 600°C depending on conversion targets — ruthenium nanoparticles supported on alumina are susceptible to sintering, the agglomeration of active metal particles that reduces accessible surface area and diminishes catalytic activity over time. While promoter additions and support modifications can mitigate sintering rates, complete elimination of thermal deactivation remains an unsolved challenge, necessitating periodic catalyst regeneration or replacement cycles that add operational complexity and lifecycle cost to ammonia cracking systems.

Furthermore, competition from lower-cost non-precious metal catalyst alternatives is intensifying. The research community and several commercial developers are actively pursuing nickel-, cobalt-, and iron-based catalyst systems for ammonia decomposition that could substantially undercut the material cost of Ru/Al₂O₃ formulations. While these base metal alternatives currently require higher operating temperatures to achieve comparable ammonia conversion rates, ongoing advances in nanostructuring, support optimization, and promoter chemistry are narrowing the performance gap. Should a commercially viable non-precious metal catalyst achieve acceptable activity at moderate temperatures, it could displace ruthenium-based systems in cost-sensitive large-scale cracking applications — representing a medium-to-long-term competitive threat that incumbent Ru/Al₂O₃ catalyst producers must monitor closely and respond to through sustained innovation.

Vast Market Opportunities on the Horizon

- Expansion of International Green Ammonia Trade Corridors Opening New End-Use Markets: The development of dedicated green ammonia export projects in high-renewable-resource regions — including Australia's Pilbara, the NEOM project in Saudi Arabia, Namibia's Hyphen Hydrogen Energy project, and Chile's Magallanes region — is creating a new class of hydrogen supply chain that will require large-capacity ammonia cracking terminals at destination ports in Japan, South Korea, Germany, and the Netherlands. Each of these import terminals represents a substantial, recurring procurement opportunity for high-performance Ru/Al₂O₃ catalysts, given that cracking efficiency directly determines the delivered cost of hydrogen to end users. As these supply chains mature from feasibility into engineering and construction phases over the latter half of the 2020s, catalyst demand volumes are expected to scale meaningfully from current niche applications.

- Integration of Ammonia Cracking with Fuel Cell and Industrial Hydrogen Applications: Beyond large-scale hydrogen import terminals, Ru/Al₂O₃ catalysts are finding emerging applications in distributed and mid-scale ammonia cracking systems designed to supply hydrogen for fuel cell power generation, industrial process heating, and maritime fuel applications. The maritime sector, in particular, represents a high-growth opportunity, as ship operators and port authorities evaluate ammonia-fueled vessels that may utilize onboard or dockside cracking to produce hydrogen for fuel cell propulsion. Similarly, remote industrial facilities seeking reliable off-grid power through hydrogen fuel cells are evaluating compact ammonia cracking units where the premium performance of ruthenium-based catalysts justifies the material cost premium through improved system efficiency and reduced balance-of-plant complexity.

- Advances in Catalyst Recycling and Ruthenium Recovery Improving Long-Term Economics: The development of commercially efficient processes for recovering and recycling ruthenium from spent Ru/Al₂O₃ catalyst beds presents a significant opportunity to reduce the effective material cost of these catalysts over their operational lifecycle. Closed-loop ruthenium recovery systems could substantially de-risk the precious metal cost exposure for project operators while also reducing the environmental footprint associated with primary ruthenium mining. Several specialty chemicals and precious metal refining companies are actively developing enhanced hydrometallurgical and pyrometallurgical ruthenium recovery processes. Furthermore, the growing body of academic and industrial research into bimetallic ruthenium catalyst formulations — combining Ru with secondary metals to enhance activity and thermal stability while potentially reducing total ruthenium content — opens a promising pathway for next-generation Ru/Al₂O₃ catalyst products that could broaden the market's competitive appeal considerably.

In-Depth Segment Analysis: Where is the Growth Concentrated?

By Type:

The market is segmented into Promoted Ru/Al₂O₃ Catalyst (Alkali-Promoted), Unpromoted Ru/Al₂O₃ Catalyst, Bimetallic Ru-Based/Al₂O₃ Catalyst, and High-Surface-Area Ru/Al₂O₃ Catalyst. Alkali-Promoted Ru/Al₂O₃ Catalyst currently holds a dominant position within this segment. The addition of alkali metal promoters such as potassium or cesium significantly enhances the electron density on ruthenium active sites, thereby improving nitrogen desorption kinetics — the rate-limiting step in ammonia decomposition. Bimetallic formulations are gaining traction as researchers seek to fine-tune selectivity and thermal stability, while high-surface-area variants offer improved dispersion of ruthenium nanoparticles across the alumina support, maximizing active site availability and overall catalytic performance.

By Application:

Application segments include Hydrogen Production for Fuel Cells, Industrial Hydrogen Supply Chains, Ammonia-to-Power Generation, Onboard Hydrogen Generation (Mobile Applications), and others. Hydrogen Production for Fuel Cells represents the most strategically significant application driving demand for Ru/Al₂O₃ catalysts in the ammonia cracking space. As hydrogen fuel cells gain widespread adoption in transportation and stationary power sectors, the need for a clean, efficient, and safe hydrogen carrier such as ammonia has become increasingly pronounced. Ammonia-to-power generation is gaining momentum in regions pursuing hydrogen-based energy security strategies, while onboard hydrogen generation for mobile applications represents an innovative frontier with strong long-term potential.

By End-User Industry:

The end-user landscape includes the Chemical & Petrochemical Industry, Energy & Power Generation Sector, Transportation & Mobility Sector, and Research & Academic Institutions. The Energy & Power Generation Sector is emerging as the most influential end-user category for Ru/Al₂O₃ catalysts in ammonia cracking applications. The global push toward clean energy infrastructure and net-zero targets is compelling power generators to explore ammonia as a viable hydrogen carrier, with catalytic cracking serving as the critical conversion step. The transportation and mobility sector, driven by the rapid expansion of hydrogen-powered vehicles and maritime applications, is generating substantial new demand. Research and academic institutions play a pivotal upstream role by continuously advancing catalyst formulation science and exploring novel alumina support modifications to enhance durability and activity.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/308736/-market

Competitive Landscape:

The global Ruthenium (Ru) / Alumina (Al₂O₃) Catalyst for Ammonia Cracking (H₂ Recovery) market is characterized by a concentrated group of established specialty catalyst and precious metal chemical manufacturers competing intensively on the basis of technical performance, supply chain reliability, and proprietary formulation expertise. Leading this space are companies with deep experience in platinum group metal (PGM) chemistry and heterogeneous catalysis. Johnson Matthey (UK), Topsoe A/S (Denmark), and Clariant AG (Switzerland) collectively command a commanding share of the global market, underpinned by extensive intellectual property portfolios, vertically integrated PGM supply relationships, and long-standing partnerships with industrial gas and energy customers across key hydrogen economy markets.

Beyond the established leaders, a growing cohort of niche and regionally focused manufacturers — including Heraeus (Germany), Umicore (Belgium), and Nikki-Universal (Japan) — are gaining meaningful traction as the accelerating global interest in green hydrogen production via ammonia cracking creates new commercial entry points. The competitive strategy across the market is overwhelmingly focused on advancing catalyst formulation science to reduce ruthenium loading requirements without compromising activity, alongside forming strategic vertical partnerships with ammonia cracking system integrators and hydrogen infrastructure developers to co-develop and validate next-generation catalyst solutions, thereby securing forward demand across the market's anticipated growth cycle through 2034.

List of Key Ruthenium (Ru) / Alumina (Al₂O₃) Catalyst for Ammonia Cracking Companies Profiled:

- Johnson Matthey (United Kingdom)

- Topsoe A/S (Haldor Topsoe) (Denmark)

- Clariant AG (Switzerland)

- BASF SE (Germany)

- Heraeus Group (Germany)

- Umicore (Belgium)

- Nikki-Universal Co., Ltd. (Japan)

- Sakai Chemical Industry Co., Ltd. (Japan)

- Axens (France)

Regional Analysis: A Global Footprint with Distinct Leaders

- Asia-Pacific: Stands as the leading region in the global Ru/Al₂O₃ Catalyst for Ammonia Cracking market, driven by an aggressive and well-funded pivot toward hydrogen as a central pillar of national energy strategies. Countries such as Japan, South Korea, and Australia have positioned ammonia-to-hydrogen conversion as a practical near-term pathway for clean energy delivery. Japan's government-backed hydrogen society roadmap and South Korea's Hydrogen Economy Promotion Act have catalyzed significant investment in ammonia cracking infrastructure, creating sustained demand for high-performance catalysts. Australia, as a major prospective ammonia exporter, is actively developing the supply chain ecosystem to support large-scale cracking operations at import terminals across Asia. China's expansive industrial base and growing commitment to decarbonizing its chemical and steel sectors further amplify regional demand.

- Europe: Is a compelling and high-priority market for ammonia cracking catalyst technology, underpinned by the European Union's ambitious REPowerEU plan and the broader Hydrogen Strategy targeting significant green hydrogen deployment. Several European nations, including Germany, the Netherlands, and the United Kingdom, are actively developing ammonia import terminals as part of their strategy to diversify energy supply and reduce dependence on fossil fuels. Germany's Hydrogen Action Plan and the Netherlands' port infrastructure developments at Rotterdam position Europe as a major future consumer of cracked hydrogen derived from imported ammonia, with Ru/Al₂O₃ systems consistently favored for their high efficiency and well-documented performance profiles.

- North America, South America, and Middle East & Africa: These regions represent an evolving and increasingly significant frontier of the Ru/Al₂O₃ catalyst market. North America, backed by the Inflation Reduction Act's clean hydrogen production incentives, is fostering a favorable environment for ammonia-based hydrogen delivery pathways. South American nations such as Brazil, Chile, and Argentina are emerging as prospective green ammonia producers with export ambitions, while the Middle East — particularly Saudi Arabia and the UAE — is investing heavily in green and blue ammonia production. While these regions currently represent smaller market volumes relative to Asia-Pacific and Europe, their long-term growth potential is substantial as hydrogen infrastructure investments and ammonia trade flows mature through the latter half of the decade.

Get Full Report Here: https://www.24chemicalresearch.com/reports/308736/-market

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/308736/-market

About 24chemicalresearch

Founded in 2015, 24chemicalresearch has rapidly established itself as a leader in chemical market intelligence, serving clients including over 30 Fortune 500 companies. We provide data-driven insights through rigorous research methodologies, addressing key industry factors such as government policy, emerging technologies, and competitive landscapes.

- Plant-level capacity tracking

- Real-time price monitoring

- Techno-economic feasibility studies

International: +1(332) 2424 294 | Asia: +91 9169162030

Website: https://www.24chemicalresearch.com/