A significant operational scale-up is redefining automated test script execution, high-frequency signal emulation, and laboratory testing workflows, fueled by the commercial necessity to deploy highly reliable, multi-band diagnostic equipment capable of processing dense network protocols without compromising delivery timelines worldwide.

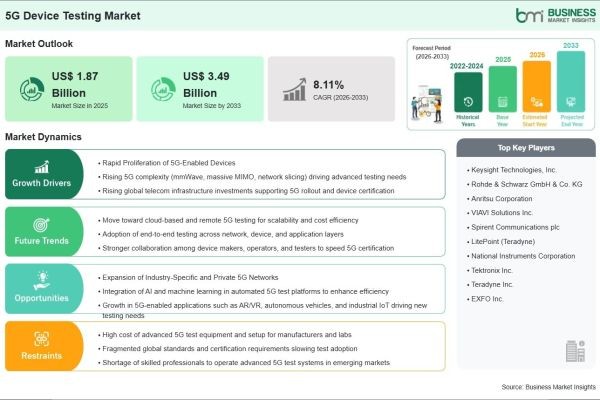

Based on market intelligence from Business Market Insights, the global 5G Device Testing Market is anticipated to reach US$ 3.49 Billion by 2033, mounting from its 2025 value of US$ 1.87 Billion at a projected CAGR of 8.11% from 2026 to 2033.

Technological advancement is transforming this market, with test equipment vendors introducing highly sophisticated Over-the-Air (OTA) testing chambers and automated one-box signaling testers capable of handling both sub-6 GHz and millimeter-wave (mmWave) frequencies. These innovations are essential for validating advanced antenna architectures like Massive MIMO. As the telecommunications ecosystem transitions toward virtualized and open network architectures (Open RAN), strong collaboration between chipset designers, telecom operators, and test instrument manufacturers is ensuring that 5G hardware meets stringent global regulatory and quality standards before commercial deployment.

Download Sample Report : https://www.businessmarketinsights.com/sample/BMIPUB00033242

What Is 5G Device Testing?

5G device testing is the comprehensive evaluation of 5G-capable user equipment (UE)—such as smartphones, IoT sensors, and autonomous vehicle modules—to verify their functionality, performance, and compliance with 3GPP network standards. Operating within specialized laboratory and manufacturing environments, its fundamental purpose is to ensure that a device can successfully connect to a 5G network, maintain stable data transfer at high speeds, and manage power efficiently without causing signal interference.

The technology encompasses a wide range of analytical methodologies, including protocol testing, radio frequency (RF) testing, radio resource management (RRM), and application-level performance testing. Because 5G devices utilize complex multi-antenna arrays (Massive MIMO) and highly directional beamforming, modern testing heavily relies on Over-the-Air (OTA) methodologies rather than traditional cabled connections. This ensures devices perform optimally under real-world conditions, handling varying frequency bands from sub-6 GHz to high-frequency mmWave spectrums.

Market Drivers

A primary driver of the 5G Device Testing Market is the rapid global expansion of 5G Standalone (SA) networks. Unlike earlier Non-Standalone (NSA) deployments that relied on existing 4G LTE cores, 5G SA operates on an entirely new cloud-native core architecture. This architectural shift requires rigorous new testing protocols to validate ultra-reliable low-latency communication (URLLC) and network slicing capabilities, forcing device manufacturers to heavily invest in upgraded testing instrumentation to guarantee seamless network integration.

The explosive proliferation of 5G-integrated industrial and consumer devices acts as the second major driver. Beyond standard smartphones, 5G modems are being embedded into connected vehicles, smart city infrastructure, augmented reality (AR) headsets, and industrial robotics. Each of these diverse form factors requires exhaustive interoperability and regulatory compliance testing to guarantee mission-critical reliability, thereby significantly expanding the customer base for testing equipment vendors beyond traditional mobile phone manufacturers.

Furthermore, the technical complexities associated with millimeter-wave (mmWave) frequencies and Massive MIMO technologies are catalyzing the procurement of advanced testing gear. mmWave signals are highly susceptible to environmental attenuation and require precise beamforming to function. Testing these parameters necessitates sophisticated anechoic chambers and high-frequency spectrum analyzers, driving substantial capital expenditure across R&D and production facilities globally.

Market Segmentation

By Equipment Type

- Spectrum & Signal Analyzers: The dominant equipment segment, essential for analyzing complex RF signals, verifying frequency accuracy, and identifying interference in wide-bandwidth 5G spectrums.

- Oscilloscopes: Critical for analyzing time-domain signals and verifying the power consumption and digital interfaces of high-speed 5G chipsets.

- Network Analyzers: Utilized for high-accuracy testing of 5G network components, including antennas, RF modules, and high-frequency transmission systems.

- Signal Generators: Used to simulate real-world 5G base station signals to test how a receiver responds under varying network loads and fading conditions.

- Over-the-Air (OTA) Test Systems: Experiencing rapid growth, these specialized chambers are mandatory for testing mmWave devices that lack physical RF connector ports.

By End User

- IDMs & ODMs (Integrated & Original Design Manufacturers): The largest segment, heavily utilizing testing equipment during the R&D and mass-production phases of custom 5G devices and RF chipsets.

- Telecom Equipment Manufacturers: Relying on rigorous testing to validate base station hardware, small cells, and Open RAN radio units before carrier deployment.

- Telecom Operators: Utilizing testing solutions for network acceptance, field validation, and ensuring user devices perform optimally on their specific spectrum holdings.

The Spectrum & Signal Analyzers segment held the dominant market share in 2025 due to its indispensable role in RF validation, while the IDMs & ODMs end-user segment is projected to register the highest growth rate as the diversity of 5G-enabled hardware expands.

Regional Insights

- Asia-Pacific remains the dominant and fastest-growing market, fueled by massive commercial 5G rollouts, government-backed technological initiatives, and the heavy concentration of consumer electronics and semiconductor manufacturing hubs in China, Taiwan, and South Korea.

- North America maintains a highly advanced market position, characterized by heavy investments in mmWave deployment, private 5G networks for industrial use, and early-stage 6G research and development.

- Europe is witnessing steady growth driven by strict telecom regulatory standards, expanding Open RAN initiatives, and strong adoption of 5G connectivity within the regional automotive manufacturing sector.

- Middle East & Africa is experiencing targeted adoption as Gulf nations aggressively modernize their digital infrastructure to support smart city frameworks.

- South America is an emerging market, with testing requirements growing steadily as regional carriers expand their mid-band 5G coverage footprints.

Top Players in the 5G Device Testing Market

The competitive landscape is characterized by global test and measurement leaders focusing on software-defined architectures, automated testing suites, and advanced high-frequency hardware capabilities.

- Keysight Technologies, Inc.

- Anritsu Corporation

- Rohde & Schwarz GmbH & Co KG

- Teradyne, Inc. (LitePoint)

- National Instruments Corporation (NI)

- Advantest Corporation

- Spirent Communications plc

- Viavi Solutions Inc.

- EXFO Inc.

- Teledyne LeCroy

Leading companies are actively allocating R&D capital to develop integrated "one-box" testers and AI-driven automation software to help manufacturers accelerate their time-to-market while reducing total testing costs.

Technological Innovations

The integration of Artificial Intelligence (AI) and machine learning into testing software is revolutionizing the 5G device testing market. Modern test automation platforms utilize AI algorithms to rapidly analyze massive datasets generated during RF and protocol testing. This capability allows engineers to instantly identify anomaly patterns, predict potential device failures under specific network loads, and dramatically reduce the time-to-market for complex 5G smartphones and IoT modules.

Advancements in Over-the-Air (OTA) testing chambers have been critical for the commercialization of mmWave devices. Because 5G antennas are deeply integrated into the device chassis without physical diagnostic ports, vendors have developed compact, highly shielded OTA enclosures. These systems simulate complex 3D signal environments and dynamic beamforming scenarios, ensuring that a device's antenna array can seamlessly track and lock onto cellular towers even while in rapid motion.

Furthermore, the evolution of "One-Box" testing solutions is streamlining production line efficiency. Traditionally, validating a cellular device required a sprawling rack of disparate instruments. Today, manufacturers have engineered highly integrated, software-defined testers that combine signaling, RF measurement, and protocol validation into a single compact unit, significantly reducing the factory floor footprint and lowering the total cost of test for high-volume device manufacturers.

Future Market Outlook

The future outlook for the 5G Device Testing Market is exceptionally optimistic, directly tied to the ongoing evolution of 3GPP standards (such as Release 17 and 18) and the preliminary research phase of 6G technologies through 2033. As cellular connectivity becomes the backbone of autonomous transportation, remote robotic surgery, and advanced smart manufacturing, the tolerance for device failure will drop to zero, mandating even more rigorous pre-deployment testing regimes.

Market leadership in the upcoming decade will be defined by software agility and high-frequency hardware capabilities. Test equipment vendors that can deliver scalable, cloud-connected automated testing suites and seamlessly upgrade their platforms to support sub-Terahertz frequencies will secure a decisive competitive advantage in the rapidly advancing wireless telecommunications ecosystem.

Frequently Asked Questions (FAQs)

What is the projected size of the 5G Device Testing Market by 2033?

The market is projected to reach US$ 2.65 Billion by 2033, rising from US$ 1.45 Billion in 2025.

What is the CAGR for the 5G Device Testing Market?

The market is expected to grow at a CAGR of 7.82% from 2026 to 2033.

Which equipment segment is essential or dominant?

The Spectrum & Signal Analyzers segment held the dominant market share in 2025 due to its indispensable role in analyzing signal integrity, bandwidth, and interference in complex 5G networks.

Which region is expected to grow the fastest?

Asia-Pacific is projected to exhibit the fastest growth and highest market share, driven by a massive concentration of semiconductor manufacturers, aggressive 5G rollouts, and booming consumer electronics production.

What is the primary factor driving demand?

The rapid global deployment of 5G Standalone (SA) networks and the escalating complexity of validating mmWave and Massive MIMO devices are the primary catalysts for market expansion.

Browse More Reports:

https://www.businessmarketinsights.com/reports/high-performance-medical-plastics-market

https://www.businessmarketinsights.com/reports/high-speed-data-converter-market

https://www.businessmarketinsights.com/reports/titanium-dioxide-market

About Us

Business Market Insights is a market research platform that provides subscription service for industry and company reports. Our research team has extensive professional expertise in domains such as Electronics & Semiconductor; Aerospace & Defense; Automotive & Transportation; Energy & Power; Healthcare; Manufacturing & Construction; Food & Beverages; Chemicals & Materials; and Technology, Media, & Telecommunications.

Contact Us

If you have any questions about this report or would like further information, please contact us:

Contact person: Ankit Mathur

Email: sales@businessmarketinsights.com

Phone: +16467917070