Market Overview and Growth Outlook

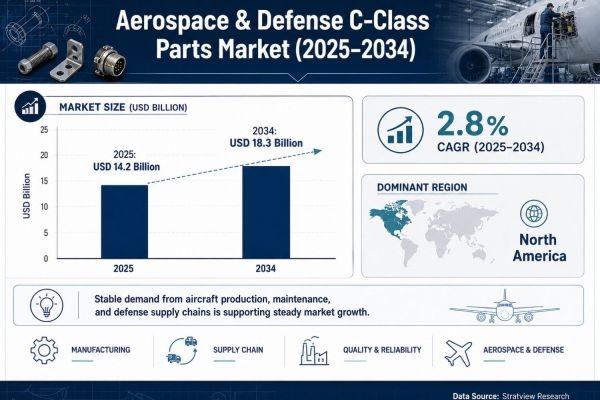

The Aerospace & Defense C-Class Parts Market reached USD 13.6 billion in 2024 after increasing 16.5% from USD 11.7 billion in 2023. Annual market value is expected to reach USD 14.2 billion in 2025 before rising to USD 18.3 billion by the end of the 2025–2034 forecast period.

“The Aerospace & Defense C-Class Parts Market is expected to grow at a CAGR of 2.8% during 2025–2034.” The total cumulative sales opportunity is forecast at USD 165.3 billion. This market intelligence reflects continued demand from aircraft OEMs, airlines, maintenance organizations, distributors, parts brokers, and suppliers serving commercial and military aviation.

The top ten countries accounted for more than 80% of the market in 2024, representing over USD 10.8 billion. The top ten companies collectively represented an estimated 50%–70% share, equivalent to USD 6.8 billion–USD 9.3 billion. These figures indicate meaningful concentration across geographic demand and leading market participants.

Analysis of Aerospace & Defense C-Class Parts Market share must account for differences across aircraft types, component categories, sales channels, end users, and regions. Commercial Aircraft, Hardware Parts, Distributors, OE Sales, and North America occupy leading positions, while Electronic Components and Asia-Pacific provide faster-growing areas within the stated market structure.

Request a free sample report:

https://www.stratviewresearch.com/Request-Sample/aerospace-&-defense-c-class-parts-market#form

Market Segmentation Analysis

Aircraft-Type Analysis includes Commercial Aircraft, Regional Aircraft, General Aviation, Helicopter, and Military Aircraft. Commercial Aircraft is anticipated to remain the demand generator and fastest-growing aircraft category. Production increases for the B737 and A320 family, COMAC’s expansion, new aircraft launches, fleet growth, passenger activity, and air-cargo demand support this position.

Part-Type Analysis includes Hardware Parts, Bearings, Electronic Components, and Machined Parts. Hardware Parts are expected to hold the dominant position because of their broad usage across aircraft structures and systems. Electronic Components are likely to grow fastest, driven by increasing installation across avionics, harnesses, cabin lighting, engines, flight controls, landing gear, and hydraulic systems.

Sales Channel-Type Analysis includes Direct Sales, Distributors, and Parts Brokers. Distributor sales are projected to hold the major share and grow at the fastest pace. Their inventory positions and contractual relationships support consistent delivery. Direct Sales provide control for specialized components, while Parts Brokers facilitate urgent sourcing, hard-to-find replacements, and surplus aftermarket transactions.

End-User-Type Analysis includes OE Sales and Aftermarket Sales. OE Sales are expected to remain the dominant and fastest-growing category. Upcoming programs, order backlogs, long production runs, and passenger traffic support OE demand. Aftermarket consumption continues as aging aircraft require maintenance, replacement parts, system upgrades, refurbishment, and service-life-extension work.

Regional Market Insights

North America is expected to remain the largest market during 2025–2034. The United States operates the world’s largest military aircraft fleet and one of its largest commercial fleets. Regional demand is reinforced by major OEMs, continued aircraft production ramp-ups, and defense spending, sustaining requirements for fasteners, bearings, electronics, and machined products.

Asia-Pacific is likely to expand at the fastest rate. China and India are supporting demand through passenger growth and fleet expansion. Boeing and Airbus assembly facilities in China, COMAC’s C919 launch, India’s growing aerospace sector, and increases in commercial-aircraft fleets provide identifiable drivers for regional component demand.

Emerging Trends Shaping the Aerospace & Defense C-Class Parts Market

Aircraft electrification is supporting faster growth for Electronic Components. More electric aircraft and hybrid-electric propulsion require more connectors, switches, relays, circuit breakers, and related products. As electrical architectures expand across aircraft functions, the component mix is broadening beyond established hardware, bearing, and machined-part requirements.

Aftermarket sourcing models are also gaining significance. Distributors maintain inventory to reduce lead times, while Parts Brokers support urgent repairs, scarce components, and surplus transactions. Direct Sales remain important for specialized components that require strict traceability, performance assurance, regulatory compliance, quality oversight, or intellectual-property protection.

Key Growth Drivers of the Market

- Growth in key aircraft programs: Increasing output of the B737 and A320 family directly raises component volumes required by production lines and associated supply networks.

- Expansion of aircraft manufacturers: COMAC’s entry and production expansion add aircraft programs and sourcing requirements to the established commercial-aerospace ecosystem.

- High component volumes per aircraft: Modern aircraft use large quantities of fasteners and other C-class parts, translating platform production into substantial recurring unit demand.

- Increasing electronic-system requirements: Electrical architectures and hybrid-electric propulsion increase the number and variety of electronic components needed to support performance and efficiency.

- Rising fleet-support demand: Aging aircraft and service-life-extension strategies increase maintenance frequency, replacement demand, refurbishment activity, and requirements for rapid parts availability.

Competitive Landscape

Top Companies in the Market

Howmet Aerospace

Precision Cartparts Corp. (PCC)

Lisi Aerospace

AB SKF

RBC Bearings Incorporated

Stanley, Black & Decker, Inc.

Amphenol Corporation

TriMas Corporation

Eaton Corporation plc

LMI Aerospace (Sonaca Group)

Conclusion and Strategic Outlook

The Aerospace & Defense C-Class Parts Market is projected to expand at a CAGR of 2.8%, rising from USD 14.2 billion in 2025 to USD 18.3 billion in 2034. A cumulative opportunity of USD 165.3 billion supports a continuing market trajectory across production, maintenance, electrical integration, and replacement activities.

Competitive positioning will depend on access to aircraft programs, component portfolios, distribution channels, regional demand centers, and aftermarket customers. The market outlook favors suppliers capable of meeting high-volume requirements while maintaining aerospace standards for quality, traceability, availability, compliance, and delivery performance.

FAQs – Aerospace & Defense C-Class Parts Market

1. What is the projected market size in 2034?

The Aerospace & Defense C-Class Parts Market is forecast to reach USD 18.3 billion by 2034. This compares with USD 13.6 billion in 2024 and USD 14.2 billion expected in 2025.

2. What CAGR will the market register?

The Aerospace & Defense C-Class Parts Market is projected to grow at a CAGR of 2.8% during 2025–2034. Total cumulative sales opportunities are expected to reach USD 165.3 billion during the forecast period.

3. Which factors are increasing component demand?

Commercial-aircraft production, new programs, expanding fleets, electrical-system growth, and recurring maintenance are increasing demand. These factors support consumption across both original-equipment and aftermarket channels.

4. What is the regional market outlook?

North America is expected to remain the largest regional market, reflecting its aircraft fleets, OEM presence, production activity, and defense spending. Asia-Pacific is likely to grow fastest, supported by China’s and India’s expanding aerospace activity.

5. What market risks and investment considerations are relevant?

The market provides a sizable cumulative opportunity, although performance depends on aircraft-production schedules, fleet-maintenance activity, and program exposure. Suppliers must also satisfy demanding expectations for compliance, quality, traceability, inventory availability, and timely delivery.