A consistent operational scale-up is redefining heavy defense engineering and defense supply chain pipelines, fueled by the strategic necessity to manufacture highly versatile, crew-protected platforms capable of maintaining tactical mobility across diverse terrains and severe operational theaters worldwide.

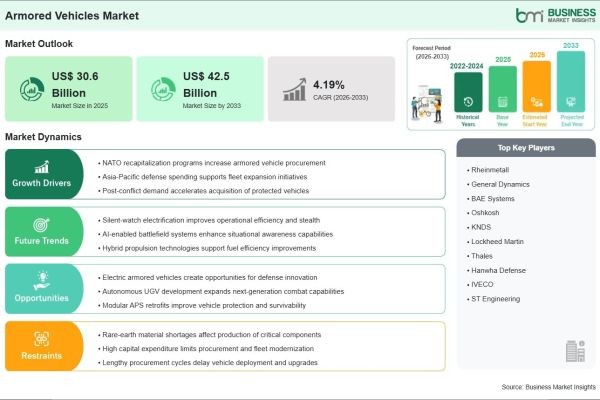

Based on market intelligence from Business Market Insights, the global Armored Vehicles Market is anticipated to reach US$ 42.5 billion by 2033, mounting from its 2025 value of US$ 30.6 billion at a projected CAGR of 4.19% from 2026 to 2033.

Technological advancements in advanced composite armor, electric and hybrid propulsion integration, and active protection systems (APS) are profoundly reshaping the armored vehicles industry. Manufacturers are increasingly focusing on delivering highly modular, survivable platforms equipped with artificial intelligence-based battlefield management systems, unmanned system integration, and advanced situational awareness capabilities. This strategic shift allows global defense forces to achieve superior mobility, lethality, and adaptability across multi-domain operations while addressing the evolving complexity of modern combat scenarios.

Download Sample Report : https://www.businessmarketinsights.com/sample/BMIPUB00035541

What Are Armored Vehicles?

Armored vehicles are specialized military platforms designed to provide robust ballistic protection, all-terrain mobility, and superior combat capabilities in hostile operational environments. These highly engineered vehicles are critical for maintaining safe troop transportation, forward reconnaissance, and direct fire support during battlefield engagements and peacekeeping missions. They provide military personnel with essential survivability against improvised explosive devices (IEDs), mine blasts, and kinetic threats.

Common armored vehicle configurations include Main Battle Tanks (MBTs), Armored Personnel Carriers (APCs), Infantry Fighting Vehicles (IFVs), and Mine-Resistant Ambush-Protected (MRAP) vehicles. Modern armored infrastructure is increasingly migrating from traditional heavy steel configurations to lightweight composite armor and modular designs. These state-of-the-art platforms are rigorously tested to meet strict defense and survivability standards, ensuring that armed forces can navigate challenging terrains and asymmetric warfare zones while maintaining the highest standard of crew safety.

Industry Drivers

A major driver of the Armored Vehicles Industry is the unprecedented surge in geopolitical tensions and the resulting expansion of global defense budgets. As nations worldwide aim to upgrade aging military fleets, defense authorities are investing heavily in the procurement of advanced tactical vehicles and heavy combat platforms. The need to accommodate complex, multi-domain operations safely, particularly in asymmetrical and urban warfare environments, necessitates robust investments in next-generation armored capabilities.

The strict operational mandates for enhanced troop survivability and modularity are also crucial growth factors. Traditional legacy vehicles often lack the agility and protection required against modern explosive threats. Defense organizations facing evolving battlefield dynamics are actively retrofitting or replacing older fleets in favor of versatile, blast-resistant platforms like MRAPs and modernized IFVs.

Furthermore, the rising integration of smart defense concepts and digitalization provides a sustained boost to leading defense contractors. The transition toward intelligent, network-centric vehicles, which link individual units to real-time command and control data, optimizes battlefield coordination, enhances threat detection through unmanned integrations, and ensures seamless overall mission management.

Industry Segmentation

By Platform

- Armored Personnel Carriers (APC): A major revenue segment, critical for providing infantry forces with protected transport across hostile environments.

- Infantry Fighting Vehicles (IFV): Essential for safely carrying troops into battle while offering direct fire support and anti-armor capabilities.

- Main Battle Tanks (MBT): Heavily armored platforms offering massive firepower and breakthrough capabilities for high-intensity conflicts.

- Mine-Resistant Ambush-Protected (MRAP): Specially designed to withstand IEDs and ambushes, widely utilized in counter-insurgency and asymmetric warfare operations.

By Mobility

- Wheeled: The fastest-growing segment, favored for superior on-road speeds, lower maintenance costs, and high strategic mobility for rapid deployment.

- Tracked: Traditional systems that still maintain a strong market presence primarily due to unmatched off-road capability and payload capacities in heavy combat scenarios.

By Propulsion

- Conventional: Accounts for the largest share due to the proven reliability of diesel engines in rugged military environments.

- Electric & Hybrid: Driven by the need for silent watch capabilities, reduced thermal signatures, and improved fuel efficiency, this segment is witnessing rapid R&D investments.

The APC and IFV segments dominate the industry due to their critical role in modern troop deployment and versatility across low and high-intensity conflicts. Wheeled mobility remains a highly attractive segment because it fundamentally reduces logistical footprints and operational overhead. Conventional propulsion holds the largest share, though hybrid-electric systems are emerging rapidly supported by rising defense innovation investments.

Regional Insights

- North America holds a significant market share, driven by massive defense modernization programs and continuous funding for maintaining tactical overmatch capabilities.

- Asia-Pacific is the fastest-growing region, fueled by rising defense spending, border security concerns, and domestic military manufacturing initiatives across major regional powers.

- Europe maintains a steady growth trajectory, supported by heightened regional security challenges, NATO commitments, and active procurement of advanced fighting vehicles across Eastern and Western European nations.

- Middle East & Africa is experiencing premium growth, with nations actively upgrading their armored fleets to counter regional insurgencies and safeguard national borders.

- South & Central America remains an active market, focusing on upgrading legacy vehicles and enhancing internal security capabilities.

Top Players in the Armored Vehicles Industry

The industry is highly competitive, with leading global defense contractors focusing on modular design innovation, active protection systems, and strategic procurement contracts with national militaries.

- General Dynamics Corporation

- BAE Systems plc

- Rheinmetall AG

- Lockheed Martin Corporation

- Oshkosh Defense, LLC

- Thales Group

- Nexter Systems

- Krauss-Maffei Wegmann (KMW)

- ST Engineering

- Otokar Otomotiv ve Savunma Sanayi A.S.

These companies continue to invest heavily in specialized R&D, aiming to develop autonomous capabilities, advanced survivability suites, and intelligent battlefield management platforms.

Technological Innovations

Technological innovation is transforming the Armored Vehicles Industry. The rapid shift toward Active Protection Systems (APS) allows modern vehicles to detect, track, and intercept incoming anti-tank guided missiles (ATGMs) and rocket-propelled grenades (RPGs) before they strike the armor. By projecting a localized defensive perimeter, these systems dramatically reduce the need for heavy passive armor, enhancing mobility without sacrificing safety.

Manufacturers are also rapidly advancing autonomous and optionally manned solutions. The development of unmanned ground vehicles (UGVs) and robotic combat vehicles provides a highly reliable tactical advantage, which is particularly revolutionary for dangerous reconnaissance or explosive ordnance disposal missions where risking human crews is strategically unfeasible.

Additionally, the integration of hybrid-electric drives represents a major trend. These propulsion systems allow for "silent watch" operations, significantly reducing acoustic and thermal signatures, providing critical stealth capabilities to ensure undetected troop movements and minimize vulnerability to thermal targeting.

Future Industry Outlook

The future outlook for the Armored Vehicles Market remains highly positive. Rising global geopolitical instability, continuous technological breakthroughs in lightweight armor, and an industry-wide commitment to fleet modernization are expected to support robust demand through 2033. The ongoing shift toward smart, connected fighting platforms will further secure the long-term operational resilience of global defense forces.

As autonomous battlefield capabilities, enhanced threat-adaptive protection, and sustainable hybrid propulsion models continue to advance, armored vehicles will become even more lethal, survivable, and critical to global military operations. Companies that focus on expanding AI software integrations, modular vehicle architectures, and comprehensive lifecycle support networks are likely to capture the strongest growth opportunities in the coming years.

Frequently Asked Questions (FAQs)

What is the projected size of the Armored Vehicles Market by 2033?

The market is projected to reach US$ 42.5 billion by 2033, rising from US$ 30.6 billion in 2025.

What factors are driving industry growth?

Key drivers include the global expansion of defense budgets to counter rising geopolitical tensions, ongoing military modernization programs, and the demand for enhanced troop survivability against modern asymmetrical threats.

Which segment dominates the industry?

Armored Personnel Carriers (APCs) and Infantry Fighting Vehicles (IFVs) currently hold substantial market shares due to their essential roles in providing safe troop transport and direct combat support.

Which region leads the industry?

North America maintains a dominant position due to its massive defense expenditure and continuous fleet modernization efforts, while the Asia-Pacific region is the fastest-growing market fueled by regional security concerns and military buildup.

Browse More Reports:

https://www.businessmarketinsights.com/reports/western-europe-autoinjectors-market

https://www.businessmarketinsights.com/reports/asean-medical-robotics-market

https://www.businessmarketinsights.com/reports/nordic-medical-robotics-market

About Us

Business Market Insights is a market research platform that provides subscription service for industry and company reports. Our research team has extensive professional expertise in domains such as Electronics & Semiconductor; Aerospace & Defense; Automotive & Transportation; Energy & Power; Healthcare; Manufacturing & Construction; Food & Beverages; Chemicals & Materials; and Technology, Media, & Telecommunications.

Contact Us

If you have any questions about this report or would like further information, please contact us:

Contact person: Ankit Mathur

Email: sales@businessmarketinsights.com

Phone: +16467917070