A consistent operational scale-up is reshaping foundry protocols, stamping procedures, and high-pressure die-casting pipelines, fueled by the manufacturing necessity to deliver high-integrity structural elements that drop overall curb weight without compromising strict vehicle crash safety benchmarks worldwide.

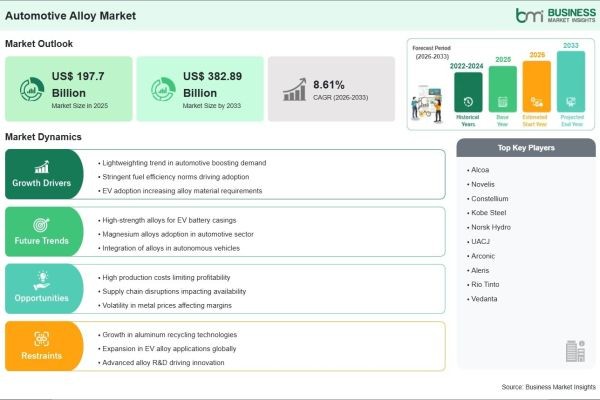

Based on market intelligence from Business Market Insights, the global Automotive Alloy Market is anticipated to reach US$ 382.89 billion by 2033, mounting from its 2025 value of US$ 197.7 billion at a projected CAGR of 8.61% from 2026 to 2033.

Download Sample Report : https://www.businessmarketinsights.com/sample/BMIPUB00035555

What Are Automotive Alloys?

Automotive alloys are engineered metal combinations designed to improve the physical and mechanical properties of raw metals, primarily aluminum, magnesium, steel, and titanium, for specific vehicle applications. These advanced materials are essential for reducing the weight of vehicles—thereby improving fuel economy—while maintaining or enhancing safety, durability, and performance. By alloying metals, engineers can customize properties like strength-to-weight ratios, heat resistance, and structural rigidity.

Technological advancements in advanced metallurgy, such as the development of high-strength aluminum alloys, lightweight magnesium alloys, and sophisticated alloying elements, are profoundly reshaping the automotive alloy industry. Manufacturers are increasingly focusing on delivering materials with superior structural integrity, enhanced corrosion resistance, and excellent formability, which are essential for complex body-in-white (BIW) structures and chassis components. This strategic shift allows global automotive OEMs to achieve highly optimized vehicle light-weighting, significantly improve energy efficiency, and comfortably meet global environmental compliance mandates.

Common automotive alloy applications include engine blocks, wheels, transmission housings, chassis components, suspension systems, and increasingly, battery enclosures for electric vehicles. Modern automotive alloy manufacturing incorporates precision casting, extrusion, and forging processes, alongside innovative post-treatment technologies that ensure the reliability of these critical components under intense road stress. The adoption of these materials is heavily influenced by the global shift toward electric vehicle (EV) technology, where weight reduction is critical to battery range optimization.

Industry Drivers

A major driver of the Automotive Alloy Industry is the urgent need for vehicle light-weighting to improve fuel economy and battery efficiency. As automotive standards mandate lower emissions and EVs require longer ranges, manufacturers are aggressively replacing heavy ferrous materials with lighter alloys. This shift directly translates into robust, recurring demand for aluminum and magnesium-based alloys across global automotive manufacturing networks.

The rapid growth of the electric vehicle (EV) market is another crucial growth factor. EVs require specialized, lightweight components to offset the weight of large battery packs. This specific requirement drives immense procurement of high-performance aluminum casting alloys for battery housings, electric motor housings, and cooling systems, effectively expanding the addressable market for alloy manufacturers.

Furthermore, a heightened focus on material sustainability and circular economy practices is boosting demand for recycled alloys. The automotive industry is increasingly adopting secondary (recycled) aluminum and magnesium alloys, which provide significant energy savings during production compared to primary metal refining. This sustainability drive is strongly supported by OEM commitments to net-zero manufacturing, ensuring sustained demand for high-quality, recycled-content alloy products.

Industry Segmentation

By Material Type

- Aluminum Alloys: The dominant segment due to their excellent strength-to-weight ratio, high corrosion resistance, and widespread adoption in engine blocks, wheels, and BIW structures.

- Magnesium Alloys: A rapidly growing segment, favored for being the lightest structural metal, ideal for weight-critical interior and chassis components.

- Steel Alloys (High-Strength): Continue to play a critical role in safety-critical structural applications where high durability is required.

By Component

- Engine Parts: Historically the largest segment, though transitioning toward powertrain and structural components in the EV era.

- Chassis & Suspension: Essential for reducing unsprung mass and improving vehicle handling and comfort.

- Wheels: A major market segment characterized by high-volume manufacturing and premium aesthetic customization.

- Body & Exterior: Focuses on light-weighting panels and structural skeletons.

By Vehicle Type

- Passenger Vehicles: The leading end-user segment, driven by global production volumes and the push for consumer-facing fuel efficiency.

- Commercial Vehicles: Growing demand for lighter alloys to increase payload capacity and fuel savings in heavy-duty logistics.

The aluminum alloys segment dominates the industry because of its fundamental versatility and established supply chains in the automotive sector. Chassis and suspension components are seeing rapid growth as manufacturers prioritize vehicle dynamics and weight management. Passenger vehicles account for the largest end-user share, supported by the global proliferation of light-duty EVs.

Regional Insights

- North America maintains a strong position, driven by mature automotive manufacturing, advanced R&D hubs, and the rapid shift toward domestic EV production.

- Asia-Pacific is the fastest-growing region, fueled by massive automotive production volumes in China, India, and Southeast Asia, along with a surging demand for both conventional and electric passenger vehicles.

- Europe continues to grow steadily, supported by strict carbon emission regulations, premium vehicle production, and early adoption of lightweighting technologies across leading OEMs.

- Middle East & Africa is seeing rising interest in automotive manufacturing and localized supply chain developments, particularly in the UAE and Saudi Arabia.

- South & Central America remains an active market, focusing on optimizing local production efficiency for both domestic and regional exports.

Top Players in the Automotive Alloy Industry

The industry is highly competitive, with leading global metals and manufacturing companies focusing on technological integration, recycled material usage, and strategic partnerships with global OEMs.

- Alcoa Corporation

- Constellium SE

- Novelis Inc. (Hindalco Industries)

- Hydro (Norsk Hydro ASA)

- Rio Tinto

- United Company RUSAL

- UACJ Corporation

- Kobe Steel, Ltd.

- AMG Advanced Metallurgical Group

- Steel Dynamics, Inc.

These companies continue to invest heavily in specialized R&D, aiming to develop high-ductility aluminum sheets, advanced magnesium alloys for large-scale casting, and sustainable, low-carbon alloy production pathways.

Technological Innovations

Technological innovation is transforming the Automotive Alloy Industry. The development of high-pressure die casting (HPDC) and large-scale "giga-casting" technologies allows automotive manufacturers to cast massive, single-piece aluminum chassis parts. This revolutionary approach significantly reduces the number of parts, welding processes, and total vehicle weight, dramatically accelerating production times.

Manufacturers are also rapidly advancing the design of high-ductility alloys that can withstand the intense stress of complex stamping processes. The development of these advanced alloys allows for thinner-walled, more intricate vehicle panels that maintain high structural rigidity, improving both fuel efficiency and crash safety performance.

Additionally, the integration of advanced coating technologies—such as specialized surface treatments that prevent corrosion in magnesium components—is another major trend. By overcoming historical limitations of magnesium, these innovations are unlocking new potentials for high-volume weight reduction in structural vehicle parts.

Future Industry Outlook

The future outlook for the Automotive Alloy Industry remains highly positive. Rising global vehicle production, the accelerating transition to electric platforms, continuous technological innovation in lightweight metallurgy, and a growing emphasis on circular material economies are expected to support steady demand through 2033. The ongoing shift toward electric mobility will further cement high-performance, lightweight alloys as a vital component of future vehicle architectures.

As automated manufacturing, smart alloy design, and sustainable production technologies continue to advance, automotive alloys will become even more resilient, lightweight, and seamlessly integrated into global automotive supply chains. Companies that focus on developing robust aluminum/magnesium portfolios, enhancing recycled material content, and providing comprehensive technical support to OEMs are likely to capture the strongest growth opportunities in the coming years.

Frequently Asked Questions (FAQs)

What is the projected size of the Automotive Alloy Market by 2033?

The market is projected to reach US$ 48.2 billion by 2033, rising from US$ 32.5 billion in 2025.

What factors are driving industry growth?

Key drivers include the imperative to reduce vehicle weight for fuel/battery efficiency, the global shift toward electric vehicle (EV) production, and increasing demand for sustainable, high-strength materials.

Which material segment dominates the industry?

Aluminum alloys currently hold the largest market share due to their exceptional strength-to-weight ratio, formability, and widespread use across vehicle structures and components.

Which region leads the industry?

Asia-Pacific is the fastest-growing region, driven by its massive automotive manufacturing footprint and rising consumer demand for both electric and conventional passenger vehicles.

Browse More Reports:

https://www.businessmarketinsights.com/reports/structural-foam-market

https://www.businessmarketinsights.com/reports/substation-automation-and-integration-market

https://www.businessmarketinsights.com/reports/sulphuric-acid-market

About Us

Business Market Insights is a market research platform that provides subscription service for industry and company reports. Our research team has extensive professional expertise in domains such as Electronics & Semiconductor; Aerospace & Defense; Automotive & Transportation; Energy & Power; Healthcare; Manufacturing & Construction; Food & Beverages; Chemicals & Materials; and Technology, Media, & Telecommunications.

Contact Us

If you have any questions about this report or would like further information, please contact us:

Contact person: Ankit Mathur

Email: sales@businessmarketinsights.com

Phone: +16467917070