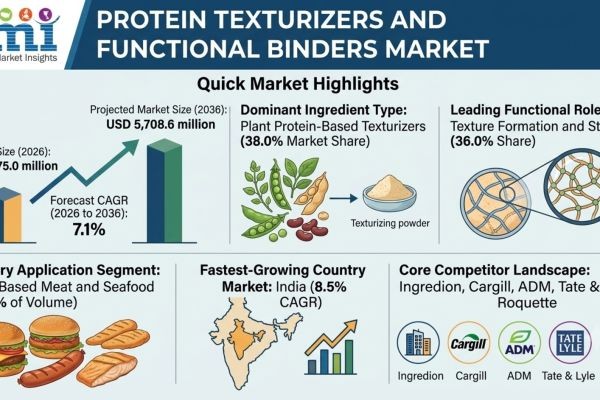

The global protein texturizers and functional binders market is undergoing a significant expansion within the functional food ingredient sector. Valued at USD 2,875.0 million in 2026, the market is projected to reach USD 5,708.6 million by 2036, expanding at a robust compound annual growth rate (CAGR) of 7.1% over the ten-year forecast period.

This market momentum reflects an essential shift from simple protein enrichment toward advanced structural engineering. High concentrations of protein isolates and concentrates frequently introduce formulation defects like dryness, chalkiness, and a crumbly mouthfeel. To maintain repeat consumer purchases, product developers rely on specialized texturizers and binding networks to restore vital elasticity, sliceability, and succulence without diluting labeled nutritional targets.

Request a Sample Report: https://www.futuremarketinsights.com/reports/sample/rep-gb-31472

Quick Market Highlights

- Market Size (2026): USD 2,875.0 million

- Projected Market Size (2036): USD 5,708.6 million

- Forecast CAGR (2026 to 2036):1%

- Dominant Ingredient Type: Plant Protein-Based Texturizers capturing a 38.0% market share

- Leading Functional Role: Texture Formation and Structure commanding a 36.0% share

- Primary Application Segment: Plant-Based Meat and Seafood accounting for 34.0% of volume

- Fastest-Growing Country Market: India, advancing at an impressive 8.5% CAGR

- Core Competitor Landscape: Ingredion, Cargill, ADM, Tate & Lyle, Roquette

Solving the Structural Bottlenecks of High-Protein Formulations

As health-conscious consumers demand greater protein fortification in daily staple foods, manufacturers are confronting major structural challenges. When clean isolates (such as pea, soy, or wheat proteins) are concentrated, they disrupt the surrounding carbohydrate and fat structures, leading to a loss of product cohesion. In plant-based patties, high-protein bars, and gluten-free bakery mixes, this structural breakdown results in severe crumbling or a dry, unappealing texture.

Protein texturizers and functional binders solve this technical issue by building strong macro-molecular networks. Under intense commercial processing conditions like high-moisture extrusion, these agents realign plant proteins into stable, fibrous strands that closely mimic the chew and physical bite of animal meat. Furthermore, they lock in uniform moisture and fat distribution, ensuring that products retain their shape and sensory appeal during final cooking and reheating cycles.

Ingredient Breakdown: Fibrous Plant Texturizers and Hydrocolloid Systems Lead

Formulators utilize distinct material types based on the structural demands, moisture requirements, and clean-label targets of their specific applications:

- Plant Protein-Based Texturizers (38.0% Share): The dominant market category. Driven by the global expansion of meat alternatives, these ingredients are essential for creating realistic, muscle-like fibrous chew and clean bite characteristics.

- Hydrocolloid-Based Binders (27.0% Share): Extensively utilized for versatile viscosity control, emulsion stability, and strong gel formation across dairy alternatives, bakery goods, and processed foods.

- Starch-Based Binders (19.0% Share): Highly favored for their cost efficiency and excellent water-holding capacity, making them standard additions in mass-market snacks and convenience foods.

- Protein Isolate and Concentrate Binders (11.0% Share): Selected when brands prioritize absolute label simplicity and ingredient transparency, enabling single-source protein claims.

- Other Special Blends (5.0% Share): Includes tailored carbohydrate-protein hybrids engineered for highly specific manufacturing environments.

Bite Realism and Moisture Control Set Formulation Priorities

When looking at the primary functional roles driving ingredient procurement, Texture Formation and Structure stands out with a 36.0% share. This clear focus highlights how critical replicating authentic bite and firmness is to gaining mass-market acceptance for plant-based formulations.

Water Binding and Retention holds a 28.0% share, acting as an essential tool for yield management and protecting products from drying out during freezing or extended storage. Fat Mimicry and Juiciness commands 21.0% of demand, helping developers recreate a rich, succulent mouthfeel in low-fat or meat-alternative matrices. The remaining 15.0% share belongs to Product Stability and Integrity, which actively prevents phase separation, crumbling, and weeping during transit and factory handling.

Custom Research Available: https://www.futuremarketinsights.com/customization-available/rep-gb-31104

Meat Alternatives and Bakery Sectors Steer High-Volume Sourcing

Commercial deployment is concentrated heavily in food categories where structural behavior directly determines consumer brand loyalty:

- Plant-Based Meat and Seafood (34.0% Share): The leading application channel, requiring precise texturizing to transform raw plant extracts into realistic nuggets, patties, and structured filets.

- Bakery and Snacks (22.0% Share): Utilized to hold complex grain-and-nut matrices together, giving high-protein energy bars a satisfying chew while preventing dough breakdown on production lines.

- Dairy and Dairy Alternatives (18.0% Share): Relies on hydrocolloid-protein networks to maintain clean particle suspension, providing a smooth, creamy body in high-protein plant milks and yogurts.

- Ready-to-Eat and Convenience Foods (16.0% Share): Deployed to protect the texture and moisture of pre-packaged meals, ensuring they do not become soft or soggy after factory freezing and consumer microwaving.

- Nutrition and Medical Foods (12.0% Share): Integrated into elderly care and clinical meal options to ensure uniform texture and easy digestibility.

Processing Boundaries and Allergen Concerns Limit Market Scaling

Despite clear growth opportunities, the market faces real technical and administrative boundaries. Certain types of hydrocolloid and plant-based binders are highly sensitive to changes in acidity and prolonged heat exposure. If a system is pushed past its limit during retort cooking or high-shear factory mixing, it can break down, causing the product to lose its uniform texture and split apart.

Additionally, navigating regional allergen regulations adds complexity to global supply chains. Widely used texturizing grains, such as wheat gluten and soy concentrates, face strict labeling mandates and shifting consumer acceptance across international borders. These regulatory hurdles force corporate procurement teams to search for non-allergenic alternatives like pea, fava bean, or pulse blends, which can increase formulation costs and development timelines.

Global Perspectives: Urbanization, Vegetarian Traditions, and Clean Labels

Geographic deployment shows distinct, localized market drivers across primary growth hubs:

- India (8.5% CAGR): Expanding rapidly due to surging urban demand for high-quality vegetarian protein snacks, fortified morning foods, and stable ready-to-cook meat alternatives.

- China (8.2% CAGR): Driven by massive industrial processing hubs where manufacturers use scalable starch-protein networks to produce uniform restructured protein snacks for national retail channels.

- Brazil (7.8% CAGR): Prompted by modern front-of-pack nutritional labeling rules, driving processors to adopt advanced binders to protect the yield and bite of reformulated meats.

- United States (6.4% CAGR): Advancing due to premium clean-label demands, where major brands favor allergen-free texturizing systems that preserve established sensory profiles.

- United Kingdom (6.1% CAGR): Shaped by strict retailer specifications, forcing brands to invest in advanced binders that ensure excellent structural stability through chilled and frozen supermarket supply lines.

Consolidated Technology Providers Move Beyond Basic Commodities

The global competitive landscape is led by major ingredient multi-nationals with deep expertise in food rheology and extrusion modeling, including Ingredion, Cargill, ADM, Tate & Lyle, and Roquette.

To secure long-term contracts, these primary suppliers are moving away from selling simple raw texturizers. Instead, they position themselves as complete technical partners, offering full-scale application testing, pilot extrusion trials, and custom-blended systems that combine plant proteins with stabilizing gums to help global food brands bring balanced, protein-rich products to market quickly.

Exclusive Discounts on Full Report: https://www.futuremarketinsights.com/reports/protein-texturizers-and-functional-binders-market

Strategic Outlook

The global protein texturizers and functional binders market has become an essential engineering resource for the modern food industry. By effectively bridging the gap between high nutritional targets and premium eating quality, these specialized ingredients allow brands to deliver clean-label, high-protein foods that perform reliably under harsh factory conditions. Moving forward, the most competitive ingredient suppliers will be those who can develop allergen-free, multi-functional texturizing systems that maintain high structural strength at low inclusion costs.

Executive Takeaways

- The global protein texturizers and functional binders market is on track to reach USD 5,708.6 million by 2036, expanding at a steady 7.1% CAGR.

- Plant protein-based texturizers remain the category leader with a 38.0% market share, favored for their unique ability to replicate authentic, fibrous animal-meat textures.

- Texture Formation and Structure serves as the primary functional driver, commanding 36.0% of global ingredient procurement.

- Plant-based meat and seafood alternatives represent the largest volume application, driving 34.0% of industry demand.

- India represents the fastest-growing geographic territory with an 8.5% CAGR, fueled by the rapid expansion of affordable vegetarian protein items.

- Sourcing trends are shifting heavily toward multi-functional systems that offer clean-label compliance alongside high process stability during extrusion and baking.

Why Choose FMI: https://www.futuremarketinsights.com/why-fmi

Explore More Related Studies Published by FMI Research

Mediterranean Cognitive-First Ingredient Systems Market: https://www.einpresswire.com/article/903332815/mediterranean-cognitive-first-ingredient-systems-market-to-reach-usd-2-290-million-by-2036

Malted Milk Powder Market : https://www.openpr.com/news/4530946/malted-milk-powder-market-to-reach-usd-13-413-7-million-by-2036-as

Older Adults Health Supplements Market : https://www.openpr.com/news/4530960/older-adults-health-supplements-market-to-reach-usd-351-1

Explore In-Depth Food & Beverage Market Insights : https://www.futuremarketinsights.com/industry-analysis/food-and-beverage

About Future Market Insights (FMI)

Future Market Insights, Inc. (FMI) is an ESOMAR-certified, ISO 9001:2015 market research and consulting organization trusted by global enterprises and Fortune 500 companies. FMI delivers actionable market intelligence, competitive benchmarking, and strategic insights across more than 30 industries and 1,200 markets worldwide.

Contact Us

Future Market Insights Inc.

Christiana Corporate, 200 Continental Drive,

Suite 401, Newark, Delaware - 19713, USA

T: +1-347-918-3531

For Sales Enquiries: sales@futuremarketinsights.com

Website: https://www.futuremarketinsights.com