Vinyl Acetate Monomer (VAM) Solution, a critical chemical intermediate produced primarily through the reaction of ethylene and acetic acid, is the foundational building block for a vast array of polymers. It has evolved from a specialty chemical to a cornerstone of modern manufacturing. Its key characteristic—a reactive double bond that readily undergoes polymerization—makes it indispensable for creating materials that are integral to daily life. As a solution, it offers superior handling and processing characteristics compared to the pure monomer, facilitating its safe and efficient integration into complex chemical synthesis and industrial coating applications. This versatility underpins its massive demand across adhesive, paint, textile, and packaging industries worldwide.

Get Full Report Here: https://www.24chemicalresearch.com/reports/265808/global-vinyl-acetate-monomer-solution-market-2024-2030-131

Market Dynamics:

The market's future is being sculpted by a potent mixture of sustained demand drivers, significant operational constraints requiring strategic navigation, and a horizon filled with promising opportunities for growth and innovation.

Powerful Market Drivers Propelling Expansion

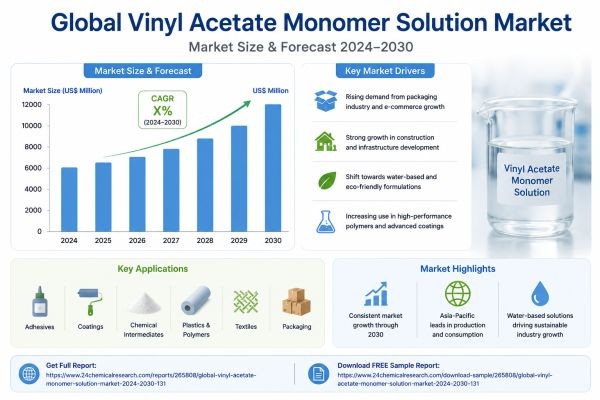

- Surging Demand from the Packaging and Construction Sectors: The relentless growth of e-commerce and the global focus on infrastructure development are primary engines for VAM consumption. Polyvinyl acetate (PVA) emulsions, derived from VAM, are the workhorse binders in water-based adhesives used for packaging, woodworking, and construction. The global packaging industry, valued at over $1 trillion, relies heavily on these adhesives for carton sealing and labeling. Similarly, in construction, VAM-based products are essential for ceramic tile adhesives and dry-mix mortars, with infrastructure investments in emerging economies creating a persistent, high-volume demand that shows no sign of abating.

- Shift Towards Water-Based and Eco-Friendly Formulations: Stringent environmental regulations, such as VOC (Volatile Organic Compound) emission standards in North America and Europe, are dramatically accelerating the transition from solvent-based to water-based systems. VAM-based emulsions are at the forefront of this shift because they offer excellent performance with significantly lower environmental impact. This regulatory push is not just a constraint but a powerful driver, creating a captive market for VAM as industries reformulate their products to meet sustainability mandates and consumer preferences for greener alternatives, which can command a price premium of 10-15%.

- Innovation in High-Performance Polymers and Coatings: Beyond traditional adhesives, VAM is a key component in advanced polymers like Ethylene-Vinyl Acetate (EVA) and Polyvinyl Alcohol (PVOH). The EVA segment is experiencing robust growth, particularly in the solar energy sector where EVA encapsulant sheets are critical for protecting photovoltaic cells, with the global solar panel market expanding at a double-digit CAGR. Furthermore, VAM-based redispersible powders enhance the flexibility and water resistance of construction materials, while PVOH finds extensive use in specialized packaging films and textile sizing, demonstrating the monomer's adaptability to high-value, performance-driven applications.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/265808/global-vinyl-acetate-monomer-solution-market-2024-2030-131

Significant Market Restraints Challenging Adoption

Despite its entrenched position, the VAM market must contend with several formidable challenges that can impede growth and profitability.

- Volatility in Raw Material Prices and Supply Chain Vulnerabilities: VAM production is highly sensitive to the cost and availability of its primary feedstocks: ethylene and acetic acid. These commodities are subject to significant price fluctuations driven by crude oil dynamics, geopolitical tensions, and supply-demand imbalances. A 10-20% swing in ethylene prices can directly compress manufacturer margins by 5-8%. Furthermore, the concentrated nature of production facilities creates supply chain vulnerabilities; an unplanned outage at a major plant can lead to regional shortages and price spikes, causing significant disruption for downstream users who rely on just-in-time inventory models.

- Intense Competition from Alternative Technologies and Substitutes: While VAM is dominant, it faces constant pressure from alternative chemistries. In adhesives, polyurethane dispersions and acrylics compete for market share in specific high-performance applications. In coatings, newer resin technologies are continually being developed. While VAM-based products often hold a cost advantage, they must continually evolve to match the performance characteristics of these alternatives. This necessitates ongoing R&D investment, which can consume 3-5% of annual revenue for producers, simply to maintain their competitive position rather than to capture new growth.

Critical Market Challenges Requiring Innovation

The industry's path forward is complicated by several intrinsic challenges that demand continuous improvement and strategic foresight.

Operational excellence is paramount. VAM production is energy-intensive, and managing the carbon footprint is a growing concern, with potential carbon taxes adding 2-4% to production costs in regulated regions. Process optimization to reduce energy consumption by 10-15% is a key focus area for manufacturers aiming to protect margins and meet corporate sustainability goals. Furthermore, handling and transporting VAM solution requires strict safety protocols to prevent polymerization during transit, adding logistical complexity and cost that are often underestimated.

Another major challenge lies in market maturity in certain segments. In developed regions, growth in traditional applications like paints and standard adhesives is largely tied to GDP growth, typically a low single-digit percentage. This necessitates a strategic pivot towards high-growth emerging markets and the development of innovative, high-value applications to drive volume increases beyond the replacement market. Balancing the commoditized, high-volume segments with specialized, high-margin niches is a delicate act that defines commercial strategy for leading players.

Vast Market Opportunities on the Horizon

- Expansion in Emerging Economies: The most significant growth vector for the VAM market is the rapid industrialization and urbanization in the Asia-Pacific region, particularly in China, India, and Southeast Asia. Rising disposable incomes are fueling demand for packaged goods, while massive government investments in infrastructure and housing create immense demand for construction chemicals. These regions are expected to account for over 70% of the new global demand for VAM-derived products in the coming decade, representing a monumental opportunity for producers who can establish a strong local manufacturing and distribution footprint.

- Development of Bio-based VAM and Circular Economy Models: A frontier of innovation is the development of bio-based routes to VAM, using renewable feedstocks like bio-ethanol instead of fossil-fuel-derived ethylene. While currently at a pilot scale and facing cost hurdles of 25-40% above conventional VAM, this pathway offers a compelling value proposition for brands seeking to reduce their carbon footprint. Early movers in this space are positioning themselves to capture premium market segments. Concurrently, advancements in recycling technologies for VAM-based products, particularly packaging films, are opening up opportunities within the circular economy, turning waste into a valuable resource.

- Advanced Applications in Healthcare and Electronics: The versatility of VAM-derived polymers is finding new expressions in sophisticated sectors. In healthcare, PVOH is used in pharmaceutical film coatings and contact lens lubricants due to its excellent biocompatibility. In electronics, specific grades of EVA are critical for the lamination of flexible printed circuits. These specialized applications, while smaller in volume, offer significantly higher margins and are less susceptible to economic cycles, providing a valuable diversification strategy for technology-focused producers.

In-Depth Segment Analysis: Where is the Growth Concentrated?

By Type:

The market is primarily segmented by production process into the Ethylene Process and the Acetylene Process. The Ethylene Process is the dominant technology globally, favored for its economic scale, efficiency, and alignment with the petrochemical infrastructure. It accounts for the vast majority of world production. The Acetylene Process, while less common on a global scale, remains important in specific regions, particularly China, where coal-based acetylene is a cost-effective feedstock, illustrating how regional resource availability influences production economics.

By Application:

Application segments are diverse, encompassing Adhesives, Chemical Intermediates, Coatings, Food, Plastics, Textiles, and Others. The Adhesives segment is the undisputed leader, consuming the largest share of global VAM production. This is driven by the ubiquitous use of PVA emulsions in everything from paper packaging to wood glue. However, the Chemical Intermediates segment, which includes the production of EVA and PVOH, is exhibiting strong growth, propelled by demand from renewable energy and high-performance materials.

By End-User Industry:

The end-user landscape is broad, including Packaging, Construction, Automotive, Textiles, and Paints & Coatings. The Packaging industry is the largest consumer, leveraging VAM-based adhesives and barrier polymers. The Construction sector is a very close second, utilizing VAM in a wide range of products from paints and sealants to mortars and adhesives, making its demand heavily correlated with global construction activity.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/265808/global-vinyl-acetate-monomer-solution-market-2024-2030-131

Competitive Landscape:

The global Vinyl Acetate Monomer Solution market is highly consolidated and characterized by the dominance of a few major integrated chemical companies. The top players—Celanese (U.S.), LyondellBasell (Netherlands), Dow (U.S.), and Kuraray (Japan)—collectively command a significant majority of the global market share. Their leadership is cemented by massive-scale production assets, backward integration into key feedstocks like acetic acid and ethylene, and extensive global supply chains that provide a formidable competitive advantage.

List of Key Vinyl Acetate Monomer Companies Profiled:

- Celanese (U.S.)

- LyondellBasell (Netherlands)

- Dow (U.S.)

- Kuraray (Japan)

Competitive strategy in this mature market revolves around operational excellence to achieve the lowest production costs, strategic capacity expansions in high-growth regions like Asia, and a focus on developing specialty grades and derivatives that offer higher margins and stronger customer loyalty than standard commodity VAM.

Regional Analysis: A Global Footprint with Distinct Leaders

- Asia-Pacific: Is the dominant force in the global VAM market, representing the largest both in terms of production capacity and consumption. China is the epicenter of this dominance, driven by its massive manufacturing base for downstream products like adhesives, textiles, and paints. The region's growth trajectory is the steepest globally, fueled by continuous industrialization and rising domestic demand.

- North America and Europe: Together, these mature markets represent significant, steady demand centers. While growth rates are more modest compared to Asia-Pacific, they are characterized by a strong focus on high-value, specialty applications and stringent adherence to environmental and safety standards. These regions are hubs of innovation for bio-based and sustainable VAM derivatives.

- South America, and Middle East & Africa: These regions are emerging markets with strong long-term potential. Growth is linked to economic development, infrastructure investments, and the expansion of local manufacturing capabilities. They present opportunities for market penetration and growth, though often accompanied by higher volatility and competitive pressures.

Get Full Report Here: https://www.24chemicalresearch.com/reports/265808/global-vinyl-acetate-monomer-solution-market-2024-2030-131

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/265808/global-vinyl-acetate-monomer-solution-market-2024-2030-131

About 24chemicalresearch

Founded in 2015, 24chemicalresearch has rapidly established itself as a leader in chemical market intelligence, serving clients including over 30 Fortune 500 companies. We provide data-driven insights through rigorous research methodologies, addressing key industry factors such as government policy, emerging technologies, and competitive landscapes.

- Plant-level capacity tracking

- Real-time price monitoring

- Techno-economic feasibility studies

International: +1(332) 2424 294 | Asia: +91 9169162030

Website: https://www.24chemicalresearch.com/