The global pallet stretch wrapping machine market is undergoing a steady but meaningful transformation as warehouse operators and manufacturers shift from manual load securing toward automated, performance-driven end-of-line packaging systems. What was traditionally a low-visibility operational task is now becoming a measurable lever for cost control, throughput optimization, and workplace safety. As distribution networks expand and fulfillment speeds accelerate, wrapping consistency, film efficiency, and system integration are emerging as critical decision variables across logistics and manufacturing environments.

Quick Stats Snapshot

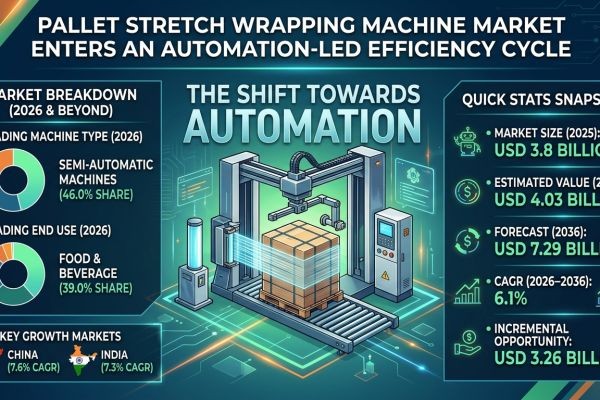

• Market Size (2025): USD 3.8 billion

• Estimated Value (2026): USD 4.03 billion

• Forecast (2036): USD 7.29 billion

• CAGR (2026–2036): 6.1%

• Incremental Opportunity: USD 3.26 billion

• Leading Machine Type (2026): Semi-Automatic Machines (46.0% share)

• Leading End Use (2026): Food & Beverage (39.0% share)

• Key Growth Markets: China (7.6% CAGR), India (7.3% CAGR)

Market Size and Forecast

The pallet stretch wrapping machine market is projected to grow from USD 4.03 billion in 2026 to USD 7.29 billion by 2036, reflecting a CAGR of 6.1%. Growth remains steady and operationally driven, supported by rising warehouse throughput requirements and increasing pressure to reduce dependency on manual labor.

This market does not expand through disruptive spikes but through gradual replacement cycles. Facilities are systematically upgrading from manual wrapping to semi-automatic and fully automatic systems, particularly in environments where load stability, speed, and material optimization directly impact operating margins.

Growth Drivers: Why Wrapping Automation Is Becoming Essential

- Labor Cost Pressures and Workforce Constraints

Manual pallet wrapping is labor-intensive, inconsistent, and physically demanding. Automation reduces workforce dependency while improving safety and repeatability. - E-Commerce and High-Throughput Fulfillment

Rapid order processing requirements are pushing distribution centers to adopt wrapping systems that integrate seamlessly with conveyor lines and automated workflows. - Film Consumption Optimization

Pre-stretch technology enabling 250% to 300% film stretch is becoming standard, significantly reducing material usage per pallet while maintaining load stability. - Warehouse Modernization Initiatives

Global investments in logistics infrastructure are accelerating adoption of semi-automatic and automatic wrapping systems, particularly in emerging markets.

Key Challenges: Balancing Efficiency and Investment

- Capital Investment Barriers: Fully automatic and integrated systems require significant upfront investment, limiting adoption among small and mid-sized operators.

• Integration Complexity: Retrofitting existing facilities with automated wrapping systems often requires layout modifications and conveyor alignment.

• Maintenance and Downtime Risks: Mechanical components, film carriage systems, and calibration requirements increase total cost of ownership.

• Space Constraints: Equipment footprint can be a limiting factor in older warehouses with restricted floor space.

Emerging Opportunities: Where Competitive Advantage Is Building

Automation Integration with Warehouse Systems

Linking wrapping machines with warehouse management systems (WMS) enables real-time monitoring of throughput, film usage, and operational efficiency.

Advanced Load Sensing and Film Control

Next-generation machines are incorporating intelligent load detection and adaptive film tension control to improve consistency across varying pallet configurations.

Robotic and Conveyor-Integrated Systems

High-volume facilities are increasingly adopting fully automated wrapping lines that eliminate manual intervention and forklift dependency.

Sustainability Through Material Reduction

Optimizing film usage is emerging as both a cost and environmental priority, aligning packaging operations with broader sustainability goals.

Segmentation Insights

By Machine Type

• Semi-Automatic Machines (46%) dominate due to cost-performance balance and flexibility in medium-volume operations.

• Fully automatic systems are gaining traction in high-throughput environments with integrated conveyor systems.

• Rotary arm machines are preferred for unstable or heavy loads requiring stationary wrapping.

By End-Use Industry

• Food & Beverage (39%) leads due to high pallet volumes, cold chain logistics, and stringent load stability requirements.

• Pharmaceuticals and consumer goods follow, driven by packaging consistency and regulatory considerations.

• Chemicals and construction materials represent niche but stable demand segments.

Regional Analysis: Automation Adoption Shapes Growth Patterns

Asia-Pacific: High-Growth Manufacturing and Logistics Hub

• China (7.6% CAGR) leads growth, driven by e-commerce expansion and warehouse automation investments.

• India (7.3% CAGR) follows, supported by logistics infrastructure development and organized retail growth.

North America: Automation Driven by Labor Constraints

The United States (6.9% CAGR) is seeing strong adoption of advanced wrapping systems due to labor shortages and fulfillment center expansion.

Europe: Precision and Industrial Efficiency

Germany (6.1%) and broader Europe emphasize integration with automated production lines, particularly in automotive and industrial logistics.

Japan: Quality and Precision Engineering

Japan (5.7%) focuses on high-precision, durable systems integrated with advanced manufacturing environments.

Competitive Landscape: Reliability and Engineering Define Market Leadership

The market is moderately consolidated, with key players including Lantech, Robopac, FROMM, Atlanta Stretch, Signode, Muller LCS, ARPAC LLC, Orion Packaging Systems, Packaging Automation Limited, and Phoenix Wrappers.

Competitive differentiation is driven by:

• Equipment reliability and uptime performance

• Film optimization and pre-stretch efficiency

• Integration capabilities with automated systems

• Global service networks and technical support

Established players benefit from strong installed bases and long-standing relationships with logistics and manufacturing operators.

Strategic Implications for Industry Stakeholders

- For Logistics Operators: Wrapping automation is becoming a core component of throughput optimization and labor cost management.

• For Manufacturers: Consistent load stability reduces product damage and improves supply chain efficiency.

• For Procurement Leaders: Investment decisions must balance capital cost with long-term operational savings and productivity gains.

• For Equipment Manufacturers: Innovation in film efficiency, automation integration, and machine reliability will define competitive positioning.

Future Outlook: Efficiency Gains Will Drive Adoption

Over the next decade, the pallet stretch wrapping machine market will be defined by incremental efficiency gains rather than disruptive change. Facilities will continue transitioning toward higher levels of automation, particularly where throughput demands justify investment.

The convergence of intelligent control systems, robotic integration, and sustainability-focused film optimization will gradually reshape end-of-line packaging operations. However, adoption will remain closely tied to cost justification and operational scalability.

Executive-Level Takeaways

- The market is projected to reach USD 7.29 billion by 2036, driven by automation and efficiency requirements.

• Semi-automatic machines remain dominant, balancing cost and performance for mid-scale operations.

• Food & beverage leads demand due to high-volume, high-frequency pallet handling.

• Film optimization through pre-stretch technology is a key cost-saving driver.

• Asia-Pacific leads growth, while North America and Europe drive automation innovation.

• Integration with warehouse systems and robotics represents the next phase of market evolution.

Full Report View: https://www.futuremarketinsights.com/reports/pallet-stretch-wrapping-machines-market