(R)-3-Aminopiperidine Dihydrochloride is a chiral building block and pharmaceutical intermediate widely utilized in the synthesis of active pharmaceutical ingredients (APIs). As a piperidine derivative in its dihydrochloride salt form, it offers enhanced stability and water solubility, making it particularly valuable in medicinal chemistry applications. The compound plays a critical role in the development of drugs targeting diabetes, central nervous system disorders, and various other therapeutic areas—most notably as a key intermediate in the synthesis of dipeptidyl peptidase-4 (DPP-4) inhibitors such as alogliptin and trelagliptin. What truly sets this compound apart is its enantiopure configuration, which enables pharmaceutical manufacturers to achieve the precise stereochemical outcomes demanded by modern drug development pipelines.

The market is gaining momentum driven by the rising global burden of type 2 diabetes, increased pharmaceutical R&D investment in chiral chemistry, and growing demand for enantiopure intermediates in drug manufacturing. Furthermore, the expanding pipeline of small-molecule therapeutics and the shift toward stereoselective synthesis in the pharmaceutical industry continue to support demand. Key manufacturers operating in this space include Sigma-Aldrich (Merck KGaA), Combi-Blocks, AK Scientific, and Amadis Chemical, among others offering high-purity grades for research and commercial-scale applications.

Get Full Report Here: https://www.24chemicalresearch.com/reports/307576/aminopiperidine-dihydrochloride-market

Market Dynamics:

The market's trajectory is shaped by a complex interplay of powerful growth drivers, significant restraints that are being actively addressed, and vast, untapped opportunities. Understanding these forces is essential to appreciating why this niche but strategically important compound is attracting increasing attention from pharmaceutical companies, contract manufacturers, and investors worldwide.

Powerful Market Drivers Propelling Expansion

-

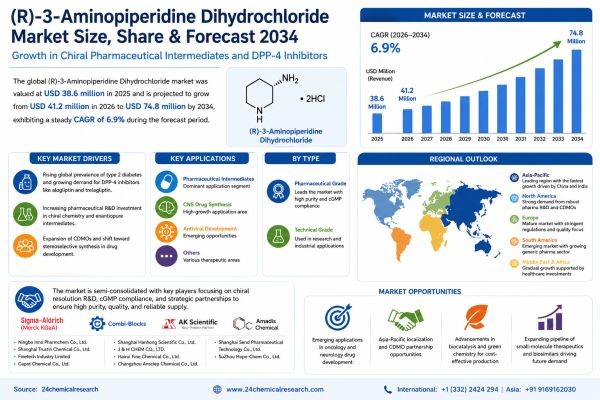

Surging Demand from the Global Diabetes Drug Pipeline: The single most powerful driver for this market is the relentless global expansion of type 2 diabetes therapeutics. With the International Diabetes Federation estimating that over 537 million adults were living with diabetes as of 2021, and that figure projected to rise to 783 million by 2045, the pharmaceutical industry faces an urgent mandate to develop and scale effective treatments. (R)-3-Aminopiperidine Dihydrochloride sits at the very heart of this effort because it serves as the critical chiral intermediate for DPP-4 inhibitors like alogliptin, a drug class that has demonstrated strong clinical efficacy with favorable safety profiles. As more generics of branded DPP-4 inhibitors enter the market, demand for cost-effective, high-purity supply of this intermediate is accelerating rapidly—making it one of the most strategically significant fine chemicals in the diabetes drug manufacturing ecosystem.

-

Growing Demand in Pharmaceutical Synthesis Across CNS and Oncology: The (R)-3-Aminopiperidine Dihydrochloride market is propelled by its critical role as a chiral building block in synthesizing complex pharmaceuticals well beyond diabetes treatments. This compound's high enantiomeric purity makes it indispensable for developing enantioselective drugs, particularly in CNS and cardiovascular therapies. With global pharmaceutical R&D investments reaching over $200 billion annually, demand for such intermediates has surged, driving market expansion at a robust pace. Key pharma players integrate this compound into piperidine-based drug syntheses across a growing range of therapeutic indications, enhancing therapeutic efficacy while streamlining regulatory submission timelines.

-

Expansion of Contract Development and Manufacturing Organizations (CDMOs): Contract development and manufacturing organizations are increasingly relying on (R)-3-Aminopiperidine Dihydrochloride to meet the needs of innovator companies pursuing novel drug candidates. The global CDMO market has been growing at a notable pace as large pharmaceutical companies increasingly outsource non-core synthesis activities, and this trend is directly benefiting suppliers of specialized chiral intermediates. Furthermore, the shift toward biologics and small-molecule hybrids has amplified usage of precisely configured building blocks. This trend is evident in the 7-8% CAGR observed in chiral intermediate segments, as manufacturers scale production to support pipeline advancements across oncology, immunology, and infectious disease.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/307576/aminopiperidine-dihydrochloride-market

Significant Market Restraints Challenging Adoption

Despite its promise and growing relevance, the market faces real hurdles that manufacturers and end-users must actively navigate to achieve widespread and sustainable adoption.

-

High Production Costs and Complex Chiral Manufacturing: Manufacturing (R)-3-Aminopiperidine Dihydrochloride involves complex chiral resolution processes, resulting in elevated costs that restrain broader adoption. Energy-intensive hydrogenation and purification steps contribute to margins as low as 15-20% for producers. Because of this, pricing remains a barrier for low-volume applications and for smaller generic drug manufacturers operating on tight cost structures. Intellectual property protections around proprietary synthesis methods further limit market entry, and while large-scale facilities can mitigate some expenses through economies of scale, smaller firms frequently face capacity utilization issues below 70%, which significantly hinders their ability to compete on price and reliability. Environmental regulations on solvent use and waste disposal add further compliance burdens, though ongoing process optimizations promise gradual relief over the medium term.

-

Regulatory Compliance Pressures and Supply Chain Vulnerabilities: Stringent FDA and EMA guidelines demand rigorous purity testing and comprehensive documentation for every batch of pharmaceutical-grade (R)-3-Aminopiperidine Dihydrochloride. This increases validation costs by up to 20% per batch and places a disproportionate burden on smaller players, accelerating market consolidation around a handful of technically capable, well-capitalized producers. At the same time, fluctuations in raw material sourcing pose significant hurdles. Dependence on specialized chemical suppliers predominantly based in Asia-Pacific regions exposes the market to geopolitical tensions, currency fluctuations, and logistics disruptions—vulnerabilities that were sharply highlighted during the COVID-19 pandemic. Efforts to diversify supply chains are underway, but they require substantial upfront investment and extended timelines for regulatory re-qualification of alternative sources.

Critical Market Challenges Requiring Innovation

The transition from laboratory-scale production to reliable industrial-scale manufacturing presents its own distinct set of challenges for this compound. Achieving consistent enantiomeric excess at commercial volumes demands highly controlled reaction conditions, sophisticated analytical infrastructure, and rigorous process validation protocols. Smaller producers frequently struggle with batch-to-batch reproducibility, which is a significant concern for pharmaceutical customers whose regulatory filings are tied to specific impurity profiles. These technical hurdles necessitate meaningful R&D investments, often consuming a substantial portion of revenue for fine chemical firms, creating a meaningful barrier to entry for new market participants who lack the process chemistry expertise and capital to compete effectively.

Additionally, the market contends with an immature and sometimes fragmented supply chain, particularly for the precursor materials required in asymmetric synthesis routes. Price volatility for specialty reagents and chiral catalysts used in the production process creates economic uncertainty for manufacturers attempting to offer stable long-term pricing to their pharmaceutical customers. Furthermore, the added complexity and cost of storing and transporting this compound under appropriate conditions—given its hygroscopic nature in some forms—adds another layer of operational challenge that end-users must factor into their procurement strategies.

Vast Market Opportunities on the Horizon

-

Emerging Therapeutic Applications in Oncology and Neurology: The (R)-3-Aminopiperidine Dihydrochloride market holds strong potential in oncology and neurology drug development, where piperidine motifs are increasingly featured in lead compounds. Pipeline drugs targeting GPCR receptors, with over 50 candidates in Phase II/III trials incorporating piperidine scaffolds, present lucrative integration points for this intermediate. This evolving demand profile could expand market volume meaningfully in the coming years. Beyond established applications, research into novel kinase inhibitors and neurological disease treatments is opening new synthetic pathways where the precise stereochemistry offered by this compound delivers critical value that racemic alternatives simply cannot match.

-

Asia-Pacific Localization and CDMO Partnership Opportunities: Asia-Pacific's rapid pharmaceutical sector growth, with India and China aggressively ramping up API production capabilities, offers compelling localization opportunities for suppliers of (R)-3-Aminopiperidine Dihydrochloride. Indian generic drug manufacturers, in particular, are actively seeking reliable domestic or regional sources of high-purity chiral intermediates to reduce import dependency and strengthen their cost competitiveness in global export markets. Partnerships with CDMOs in the region could capture significantly more demand from contract services, particularly as regulatory standards in Asia continue to converge with international norms, raising quality expectations and creating natural advantages for established suppliers of validated, cGMP-compliant intermediates.

-

Technological Advancements in Biocatalysis and Green Chemistry: Innovations in asymmetric synthesis and biocatalysis are lowering production costs and improving environmental profiles simultaneously, representing a genuine double-win for the industry. Enzymatic resolution and whole-cell biocatalysis approaches are gaining ground as viable alternatives to traditional chemical resolution methods, with demonstrated potential to reduce solvent waste by up to 30% while improving enantioselectivity. Furthermore, the biosimilars boom and the broader expansion of biologics-adjacent small-molecule therapeutics are set to increase chiral intermediate needs at a strong pace, positioning (R)-3-Aminopiperidine Dihydrochloride favorably among the beneficiaries of this structural industry shift. Strategic investments in green production technology will unlock sustained competitive advantages for early movers in this space.

In-Depth Segment Analysis: Where is the Growth Concentrated?

By Type:

The market is segmented into Pharmaceutical Grade and Technical Grade. Pharmaceutical Grade currently leads the market by a substantial margin, favored for its exceptional purity and adherence to stringent Good Manufacturing Practice standards. This grade is indispensable for high-value active pharmaceutical ingredient synthesis, where even minor impurities can compromise drug efficacy, patient safety, and regulatory approval timelines. The technical grade, while more cost-accessible, serves niche research and non-pharmaceutical industrial applications where the ultra-high purity requirements of drug manufacturing do not apply.

By Application:

Application segments include Pharmaceutical Intermediates, CNS Drug Synthesis, Antiviral Development, and others. The Pharmaceutical Intermediates segment currently dominates, serving as the core application where this compound functions as a critical chiral building block in multi-step organic syntheses for complex therapeutics. It enables precise stereochemical control that is essential for bioactive molecule development across diverse therapeutic categories. However, the CNS Drug Synthesis and Antiviral Development segments are expected to exhibit above-average growth rates in the coming years, driven by robust R&D pipelines in both areas and the demonstrated therapeutic relevance of piperidine-containing drug candidates.

By End-User Industry:

The end-user landscape includes Pharmaceutical Manufacturers, Biotechnology Firms, and Research Institutions. Pharmaceutical Manufacturers account for the largest share, leveraging the compound's unique stereochemistry for scalable production of enantiomerically pure drugs and prioritizing suppliers who can guarantee consistent quality to streamline their regulatory-compliant manufacturing pipelines. Biotechnology firms are rapidly emerging as a significant growth end-user segment, reflecting the expansion of small-molecule drug discovery programs within the biotech sector, while academic and industrial research institutions provide steady baseline demand for smaller quantities of high-purity material.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/307576/aminopiperidine-dihydrochloride-market

Competitive Landscape:

The global (R)-3-Aminopiperidine Dihydrochloride market is semi-consolidated and characterized by a concentration of specialized fine chemical manufacturers competing on the basis of purity, supply reliability, regulatory compliance credentials, and process chemistry expertise. The market structure remains fragmented yet concentrated, with top manufacturers holding over 60% of global production capacity, driven by rising demand for this enantiopure intermediate across antiretroviral drugs, CNS therapeutics, and other API syntheses. Chinese manufacturers have established a particularly strong foothold, benefiting from advanced asymmetric synthesis capabilities, cost-effective production infrastructure, and proximity to key raw material supply chains.

Niche and emerging players are increasingly focusing on high-purity custom synthesis and sustainable production methods, including biocatalytic approaches, to differentiate themselves in regulated markets where quality credentials are paramount. The competitive dynamics emphasize quality consistency and supply reliability amid global pharma outsourcing trends, positioning established manufacturers with proven cGMP track records for sustained market leadership. Western entities primarily act as custom manufacturers, resellers, or distributors, with limited large-scale primary production, though this dynamic is gradually shifting as geopolitical supply chain concerns prompt some diversification of sourcing toward European and North American custom synthesis providers.

List of Key (R)-3-Aminopiperidine Dihydrochloride Companies Profiled:

-

Ningbo Inno Pharmchem Co., Ltd. (China)

-

Shanghai Trustin Chemical Co., Ltd. (China)

-

Finetech Industry Limited (China)

-

Capot Chemical Co., Ltd. (China)

-

Shanghai Hanhong Scientific Co., Ltd. (China)

-

J & H CHEM CO., LTD. (China)

-

Hairui Fine Chemical Co., Ltd. (China)

-

Changzhou Ansciep Chemical Co., Ltd. (China)

-

Shanghai Send Pharmaceutical Technology Co., Ltd. (China)

-

SuZhou Hope-Chem Co., Ltd. (China)

-

Sigma-Aldrich (Merck KGaA) (Germany/U.S.)

-

Combi-Blocks (U.S.)

The competitive strategy across the leading players is overwhelmingly focused on investment in chiral resolution R&D to enhance enantiomeric purity and reduce production costs, alongside the pursuit of cGMP certifications and quality audits that open doors to tier-one pharmaceutical customers. Strategic vertical partnerships with CDMO and innovator pharma clients to co-develop validated synthesis routes and secure long-term supply agreements are becoming an increasingly important competitive differentiator in this market.

Regional Analysis: A Global Footprint with Distinct Leaders

-

Asia-Pacific: Is the undisputed production leader and the fastest-growing consumption region, driven by robust chemical manufacturing ecosystems in China and India. China dominates global supply, hosting extensive production capacities for chiral intermediates supported by sophisticated asymmetric synthesis infrastructure, skilled process chemists, and government backing for the fine chemicals sector. India's rapidly expanding generic pharmaceutical industry generates strong and growing domestic demand for high-purity (R)-3-Aminopiperidine Dihydrochloride, particularly as Indian manufacturers scale up production of DPP-4 inhibitor generics for global export markets. Innovation hubs in Singapore and South Korea contribute through process optimization research, further strengthening the region's competitive position.

-

North America: Remains a critically important demand center, anchored by the world's largest and most innovative pharmaceutical industry. The U.S. drives demand through extensive drug discovery pipelines requiring high-quality chiral piperidine intermediates for enantioselective synthesis of both novel and generic APIs. Contract research organizations and CDMOs play a key role in custom manufacturing, ensuring compliance with stringent FDA standards. Canada's growing biotech sector contributes via specialized applications in oncology and CNS therapeutics. While large-scale domestic production of this specific intermediate is limited, North American procurement activity is substantial and increasingly focused on qualifying multiple sources to reduce supply chain concentration risk.

-

Europe: Maintains a mature and quality-focused market, characterized by rigorous regulatory frameworks including EMA guidelines that demand exceptional purity documentation and traceability. Germany and Switzerland host premier fine chemical producers with expertise in piperidine chemistry, serving established pharma giants developing treatments for metabolic, neurological, and infectious diseases. Emphasis on green chemistry and sustainable manufacturing routes is driving gradual adoption of biocatalytic production methods. Cross-border collaborations within the EU streamline supply chains, while Eastern European nations are emerging as increasingly cost-competitive hubs for intermediate synthesis.

-

South America & Middle East and Africa: These regions represent emerging markets for (R)-3-Aminopiperidine Dihydrochloride, with Brazil and Argentina leading adoption in South America amid growing generic drug sectors. Import reliance on Asia persists across both regions, but investments in local pharmaceutical manufacturing capacity signal gradually expanding opportunities. Rising chronic disease prevalence, including diabetes, is spurring demand for the downstream drugs that rely on this intermediate, while regulatory harmonization efforts and healthcare infrastructure investments are creating the conditions for longer-term market development.

Get Full Report Here: https://www.24chemicalresearch.com/reports/307576/aminopiperidine-dihydrochloride-market

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/307576/aminopiperidine-dihydrochloride-market

About 24chemicalresearch

Founded in 2015, 24chemicalresearch has rapidly established itself as a leader in chemical market intelligence, serving clients including over 30 Fortune 500 companies. We provide data-driven insights through rigorous research methodologies, addressing key industry factors such as government policy, emerging technologies, and competitive landscapes.

-

Plant-level capacity tracking

-

Real-time price monitoring

-

Techno-economic feasibility studies

International: +1(332) 2424 294 | Asia: +91 9169162030

Website: https://www.24chemicalresearch.com/