(R)-N-Benzyl-3-cyanopyrrolidine (CAS 157528-56-8) is a chiral pyrrolidine derivative featuring a benzyl group at the nitrogen position and a cyano substituent at the 3-position of the ring, with a defined (R)-configuration. This specialty fine chemical has steadily transitioned from niche academic applications to become a critical cornerstone in pharmaceutical synthesis workflows. Its defining attributes—including precise stereochemical configuration, high enantiomeric purity, and versatile reactivity as a synthetic scaffold—make it indispensable for a range of advanced drug development programs. Unlike racemic intermediates, the (R)-configured form delivers the specific spatial geometry that translates directly into enhanced binding affinity, improved metabolic stability, and reduced off-target toxicity in bioactive molecules.

Get Full Report Here: https://www.24chemicalresearch.com/reports/307638/nbenzylcyanopyrrolidine-market

The market is gaining meaningful momentum driven by the growing demand for enantiopure intermediates in pharmaceutical synthesis, increasing investment in asymmetric chemistry, and the expanding pipeline of chiral drug candidates requiring pyrrolidine-based scaffolds. Furthermore, the broader industry-wide trend toward stereoselective synthesis in drug discovery continues to underpin demand for high-purity chiral building blocks such as this compound. Key suppliers and fine chemical manufacturers across North America, Europe, and Asia-Pacific are actively expanding their chiral intermediate portfolios to meet evolving pharmaceutical R&D requirements, and the competitive landscape is evolving accordingly.

Market Dynamics:

The market’s trajectory is shaped by a complex interplay of powerful growth drivers, significant restraints that are being actively addressed, and vast, untapped opportunities that forward-looking industry participants are beginning to capitalize on.

Powerful Market Drivers Propelling Expansion

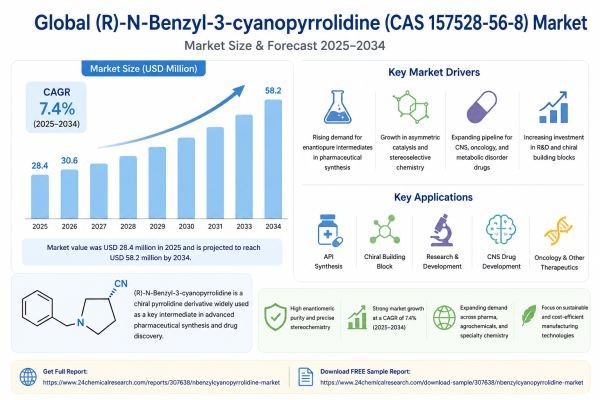

- Rising Demand in Pharmaceutical Synthesis: The (R)-N-Benzyl-3-cyanopyrrolidine market is propelled by its critical role as a chiral building block in advanced pharmaceutical intermediates. This compound serves as a key precursor in the synthesis of bioactive molecules, particularly those targeting metabolic disorders such as type 2 diabetes, where DPP-4 inhibitors like saxagliptin rely on stereospecific pyrrolidine cores. As global pharmaceutical R&D invests heavily in enantioselective processes, demand has surged, with production volumes increasing by approximately 7.5% annually since 2020. This trend underscores its importance in delivering high-purity, single-enantiomer drugs, which command premium pricing in competitive markets and face fewer regulatory hurdles than their racemic counterparts during new drug application submissions.

- Expansion of Asymmetric Catalysis Applications: Advancements in asymmetric catalysis have significantly elevated this compound’s utility beyond traditional batch synthesis. Pharmaceutical firms leverage this pyrrolidine derivative for efficient stereocontrol in complex molecule assembly, reducing synthesis steps and lowering overall costs in long manufacturing campaigns. Market data indicates the segment grew at a 6.2% CAGR from 2021 to 2023, driven by blockbuster drug developments requiring such precision intermediates. While supply chains stabilize post-pandemic, innovative process optimizations continue to fuel scalability, with continuous flow chemistry platforms particularly showing promise for this compound’s synthesis. Key pharmaceutical pipelines incorporating this intermediate project a 12% rise in utilization by 2025, highlighting its entrenched value in drug discovery workflows.

- Expanding CNS and Oncology Drug Pipelines: The compound’s role as a chiral intermediate in the synthesis of central nervous system (CNS)-active agents and NK1 receptor antagonists has opened a steadily growing demand channel. Pharmaceutical firms developing migraine therapeutics, antiemetic drugs for oncology supportive care, and protease inhibitors are incorporating this building block at increasing scales. The (R)-configuration specifically provides the geometric precision needed for effective receptor binding, making substitution with alternative scaffolds technically and commercially unattractive. Furthermore, regulatory approvals for novel therapies amplify this momentum, positioning (R)-N-Benzyl-3-cyanopyrrolidine as indispensable in the modern medicinal chemistry toolkit.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/307638/nbenzylcyanopyrrolidine-market

Significant Market Restraints Challenging Adoption

Despite its promise and growing end-use demand, the market faces meaningful hurdles that must be overcome to achieve broader commercial adoption and scale.

- High Production Costs and Technical Barriers: Manufacturing (R)-N-Benzyl-3-cyanopyrrolidine involves complex stereoselective cyanation and N-protection steps, resulting in elevated production costs that restrain broader adoption across cost-sensitive buyer segments. Capital-intensive equipment for hydrogenation and chiral chromatography pushes per-kilogram prices above $5,000 in many supplier catalogues, limiting penetration into generics-focused manufacturing tiers. Although biocatalytic alternatives are emerging as a promising cost-reduction pathway, they are not yet scaled for commercial viability in most production environments. Intellectual property constraints further impede generic entry, as patented synthetic routes dominate key process steps and foster oligopolistic dynamics, with top suppliers controlling a substantial share of commercial output.

- Regulatory Compliance Hurdles: Stringent ICH guidelines for chiral purity require extensive analytical validation, which can delay market entry for new producers and even slow procurement decisions for existing buyers. Impurity profiling under Q3A standards often extends qualification timelines by 6 to 12 months, straining smaller contract manufacturers who lack established cGMP infrastructure. Additionally, environmental regulations governing cyanide-containing intermediates add a layer of compliance burden—increasing operational overhead and necessitating specialized waste treatment protocols—that larger, vertically integrated manufacturers are far better positioned to absorb than smaller regional players.

Critical Market Challenges Requiring Innovation

The transition from laboratory-scale preparation to industrial-volume manufacturing presents its own distinct set of challenges that go beyond regulatory compliance alone. Scaling enantioselective production remains technically demanding, with commercial-scale synthesis yields hovering around 85 to 90% in typical production runs. This necessitates ongoing R&D investment, which in turn diverts resources from capacity expansion at a time when demand is accelerating. Furthermore, achieving batch-to-batch consistency in enantiomeric excess (ee) values above 99% is technically rigorous and requires sophisticated analytical infrastructure that not all potential market participants possess.

Additionally, the market contends with supply chain vulnerabilities rooted in dependence on specialized precursors and chiral resolution reagents. Fluctuating raw material prices—particularly for benzyl-protected amines and cyanide sources—have led to meaningful cost volatility over recent years. Geopolitical tensions in key sourcing regions complicate consistent availability, and pharmaceutical buyers increasingly demand diversified, multi-source supply strategies to mitigate these risks. Building that redundancy into the supply chain takes time and coordination that the market is only now beginning to address systematically.

Vast Market Opportunities on the Horizon

- Generics Expansion Driven by Patent Expirations: A growing wave of patent expirations on DPP-4 inhibitors and other pyrrolidine-scaffold-based drugs is opening a substantial generics manufacturing opportunity. As branded drug patents lapse, contract manufacturers in Asia-Pacific and India are scaling up API synthesis programs that directly incorporate (R)-N-Benzyl-3-cyanopyrrolidine as a key intermediate. This generics-driven demand channel provides a more price-stable and higher-volume complement to the innovator pharmaceutical segment, potentially driving sustained volume growth through the end of the decade.

- Emerging Applications in Agrochemicals and Specialty Chemistry: A promising frontier lies in extending this compound’s applications to agrochemical synthesis, where chiral pesticides and herbicides are gaining traction for enhanced efficacy and improved environmental safety profiles. With global crop protection markets expanding at approximately 4.5% annually, this pivot could capture meaningful new demand by 2027. Partnerships between fine chemical producers and agrochemical majors offer lucrative co-development and licensing prospects, providing diversification away from pharma-only dependency. Moreover, continuous flow manufacturing advancements are enabling greener, higher-yield production routes that could substantially reduce per-kilogram costs over the medium term.

- Precision Medicine and Custom Synthesis Demand: The rise of precision medicine is amplifying the need for highly customized chiral intermediates tailored to specific molecular targets in oncology and neurology. (R)-N-Benzyl-3-cyanopyrrolidine fits neatly into these specialized pipelines, particularly where the (R)-configuration provides the precise pharmacophore geometry demanded by advanced structure-activity relationship studies. Contract research organizations and custom synthesis providers are increasingly positioning this compound as a go-to scaffold for medicinal chemistry programs, creating a growing ecosystem of small-batch, high-value demand that complements the large-volume generics segment.

In-Depth Segment Analysis: Where is the Growth Concentrated?

By Type:

The market is segmented into Pharmaceutical Grade, Research Grade, and Industrial Grade. Pharmaceutical Grade currently leads the market by a significant margin, favored for its superior quality standards essential for active pharmaceutical ingredient (API) development, ensuring the high enantiomeric purity that is critical for chiral drug efficacy and patient safety in clinical applications. This grade directly supports stringent regulatory demands from bodies like the FDA and EMA, facilitating smoother and faster scale-up from laboratory preparation to commercial production. Research Grade, while smaller in volume, serves a vital function in driving the exploratory chemistry that seeds future commercial demand.

By Application:

Application segments include API Synthesis, Chiral Building Block, Research and Development, and others. API Synthesis leads as the primary application, serving as a key intermediate in synthesizing complex CNS therapeutics, DPP-4 inhibitors, and other enantiomer-specific drugs where the (R)-configuration provides unique stereochemical advantages in binding affinity and metabolic stability. Its role in multi-step organic synthesis pipelines underscores its indispensability for innovative drug discovery programs targeting neurological, metabolic, and oncological disorders. The Research and Development segment, while currently a smaller volume contributor, is growing as more academic and early-phase programs incorporate this scaffold.

By End-User Industry:

The end-user landscape includes Pharmaceutical Companies, Contract Research Organizations, Academic Institutions, and Chemical Manufacturers. Pharmaceutical Companies represent the foremost end-user category, leveraging the compound’s precise stereochemistry for proprietary drug development programs, particularly in optimizing pharmacokinetic profiles for next-generation therapeutics. Their focus on scalable, reproducible synthesis drives consistent demand for supply chains tailored to GMP-compliant processes. Contract Research Organizations are rapidly emerging as a key secondary growth driver, as the global CRO market’s expansion translates directly into increased outsourced demand for high-quality chiral building blocks.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/307638/nbenzylcyanopyrrolidine-market

Competitive Landscape:

The global (R)-N-Benzyl-3-cyanopyrrolidine market is a niche but strategically significant segment within the pharmaceutical fine chemicals industry, characterized by an oligopolistic structure with high entry barriers rooted in technical complexity, regulatory compliance requirements, and specialized infrastructure. Leading players are predominantly Chinese manufacturers who benefit from established expertise in chiral synthesis, cost-efficient production at scale, and deeply integrated API intermediate supply chains. Companies like Capot Chemical Co., Ltd. and Hairui Chemical Co., Ltd. collectively dominate with a substantial combined market share, supplying major pharmaceutical firms across North America, Europe, and Asia-Pacific. Their dominance is underpinned by proven cGMP manufacturing capabilities, established relationships with global API producers, and technical proficiency in handling cyanide-containing intermediates safely and at commercial scale.

However, the competitive landscape is evolving. Emerging players from India and the United States are gaining traction in the wake of supply chain diversification initiatives accelerated by post-COVID procurement strategies. Firms like Divi’s Laboratories and Biosynth Carbosynth represent growth-oriented challengers, targeting both the innovator pharmaceutical segment and the rapidly expanding generic drug manufacturing base. These companies are investing in sustainable manufacturing approaches—including biocatalytic resolution techniques and continuous flow chemistry—to meet escalating ESG expectations from multinational pharmaceutical clients. The overall competitive strategy across the market is focused on enhancing product quality, securing multi-year supply agreements, and developing proprietary synthetic routes that offer cost or purity advantages over existing processes.

List of Key (R)-N-Benzyl-3-cyanopyrrolidine (CAS 157528-56-8) Companies Profiled:

- Capot Chemical Co., Ltd. (China)

- Hairui Chemical Co., Ltd. (China)

- Biosynth Carbosynth (Switzerland)

- Divi’s Laboratories Ltd. (India)

- Finetech Industry Limited (China)

- Matrix Scientific (USA)

- Chem-Impex International Inc. (USA)

- Shanghai Minstar Chemical Co., Ltd. (China)

- MedChemExpress LLC (China)

- Pharmaffiliates Analytics & Synthetics (India)

The competitive strategy across leading participants is overwhelmingly focused on advancing chiral synthesis technology to enhance product quality and reduce per-unit costs, alongside forming long-term strategic supply partnerships with pharmaceutical end-users to co-develop application-specific solutions and secure forward demand visibility. Backward integration into precursor chemistry is also emerging as a key differentiator, providing cost stability and supply security that clients increasingly demand.

Regional Analysis: A Global Footprint with Distinct Leaders

- North America: North America stands as a leading consumption market for (R)-N-Benzyl-3-cyanopyrrolidine, driven by its world-class pharmaceutical R&D ecosystem and robust biotech sector concentrated in hubs like Boston, San Francisco, and San Diego. The region’s advanced contract research organizations and major pharmaceutical companies prioritize high-purity enantiomers to accelerate drug discovery pipelines. Strong intellectual property frameworks and facilitative FDA regulatory pathways encourage innovation and support premium pricing for GMP-grade supply. Despite higher domestic production costs compared to Asian manufacturers, North American demand remains robust because buyers in this region consistently prioritize quality assurance, regulatory traceability, and supply reliability over cost minimization alone.

- Europe: Europe maintains a strong and growing position in the market, leveraging its deep expertise in fine chemicals manufacturing and a well-established contract manufacturing organization ecosystem. Countries including Germany, Switzerland, and the United Kingdom host specialized producers with proven capabilities in large-scale chiral resolution and stereoselective synthesis. Demand originates primarily from pharmaceutical firms developing CNS drugs and metabolic disease therapies, where this compound serves as a versatile and reliable scaffold. EMA regulations promote harmonized quality standards across member states, facilitating cross-border trade and export to global markets. The region’s strong emphasis on green chemistry is also driving adoption of enzymatic resolution approaches that align with European environmental directives.

- Asia-Pacific: Asia-Pacific is simultaneously the dominant manufacturing region and a rapidly growing consumption market for this compound. China and India lead on the production side, with cost-effective synthesis capabilities, abundant precursor availability, and growing cGMP infrastructure enabling competitive pricing that attracts outsourcing from Western pharmaceutical companies. Export volumes from the region have grown significantly, supporting downstream API manufacturers worldwide. On the demand side, expanding domestic pharmaceutical industries in China, India, Japan, and South Korea are incorporating this intermediate into both generic and innovative drug pipelines, creating a self-reinforcing cycle of regional growth. Investments in stereoselective catalysis and analytical capabilities are progressively closing the quality gap with Western manufacturers.

- South America: South America represents a nascent but promising frontier, centered primarily in Brazil and Argentina. Local pharmaceutical industries are increasingly importing this chiral building block for domestic drug formulation, reducing reliance on finished API imports. Emerging regional R&D centers are beginning to explore adaptation of chiral synthesis for local health priorities, while infrastructure investments are improving the handling and logistics of fine chemical intermediates. Regulatory harmonization challenges and skilled workforce gaps remain headwinds, but gradual adoption driven by affordability considerations and growing generic drug production is laying the groundwork for longer-term market development.

- Middle East & Africa: The Middle East & Africa region currently represents the smallest market for (R)-N-Benzyl-3-cyanopyrrolidine, with primary activity concentrated in South Africa and UAE-based pharmaceutical and contract development hubs. Gulf region life sciences initiatives, supported by free zone incentives and government diversification programs, are beginning to promote synthesis capabilities that could eventually incorporate chiral intermediates of this type. Import dependency remains the norm, but strategic alliances with global fine chemical producers and growing investment in pharmaceutical manufacturing infrastructure are establishing the foundations for expanded participation over the coming decade.

Get Full Report Here: https://www.24chemicalresearch.com/reports/307638/nbenzylcyanopyrrolidine-market

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/307638/nbenzylcyanopyrrolidine-market

About 24chemicalresearch

Founded in 2015, 24chemicalresearch has rapidly established itself as a leader in chemical market intelligence, serving clients including over 30 Fortune 500 companies. We provide data-driven insights through rigorous research methodologies, addressing key industry factors such as government policy, emerging technologies, and competitive landscapes.

- Plant-level capacity tracking

- Real-time price monitoring

- Techno-economic feasibility studies

International: +1(332) 2424 294 | Asia: +91 9169162030

Website: https://www.24chemicalresearch.com/